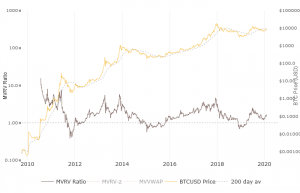

Realised market cap at all time high

In bitcoin, the concept of realised market capitalisation reflects the value of each specific sub-unit of bitcoin based on when it last moved on the blockchain. This is as opposed to the traditional measure which is simply the total number of coins multiplied by current market price. It is arguably a far more robust measure because it reflects real transactions. This week realised cap reached a new all time high of $103 billion versus the actual market cap of $167 billion.

The metric is particularly useful as a ratio, market capitalisation divided by realised capitalisation. At the market peak in 2017, this ratio was 4.7, reflecting a steep rise in price with few coins moving. When things dipped sharply in early 2019 it was 0.7. The ratio is complex because it contains not just the vector of price but also that of distribution, as coins become more and more distributed, realised cap will converge on traditional market cap so it should be interpreted with caution. That said, when the ratio drops below one it has historically been an excellent time to buy. Also, the $103 billion reflects actual dollars that have been exchanged for bitcoin and gives you a sense of the amount of “traditional money” in the game.

We can also conclude from the new all time high, that the vast majority of current holders of bitcoin have made a profit from their investment.

Realised market cap = # of Coins * Price when they last moved

Bitcoin under uncertainty

A common theme this week is “what will happen to bitcoin under uncertainty”. As an example, let us assume that Coronavirus is indeed very serious, for many multi-national companies it’s bad news. Supply chains and earnings will take a hit.

Many of the anticipated impacts on business are irrelevant to bitcoin though. Bitcoin has no staff, so they cannot get sick, it has no earnings, so it cannot fall short on that score. There is no supply chain impact from the closure of major trading partners, it simply makes no difference at all. Computer codes are familiar with viruses, but bitcoin can’t catch this particular one. The features that so often attract criticism “there’s nothing there, its just some computer code” will show themselves as major strengths as this all plays out.

Not much matters to bitcoin actually, particularly around what you might call macro risks. It’s just a piece of code right? And it rumbles on regardless. 11 years now and counting.

Credit risk

Most people would claim they don’t understand credit risk, sounds a bit “banky”. It isn’t true though, people understand it very well, inherently almost. If I were to select two of your good friends, you would be able to tell me instantly who would pay you back first if you lent them money. You wouldn’t need a spreadsheet, you wouldn’t pay Moody’s for their opinion and you would answer quickly, because inherently you are able to make that judgement and people do it all the time.

In Asia, credit often works in that way, through word of mouth. Individuals will vouch for another person, the person vouching for you will also be assessed (mentally) by the lender, if they know you, there is a good chance they will lend. It is a vastly more efficient system than the one in the Western world.

When it comes to financial markets it gets more complicated. You are not able to compute the credit risk of your bank, you just say “I don’t know what credit risk is” even though we have suggested you know exactly what it is, and you are good at assessing it.

Banks themselves won’t lend to each other without an expensive report from a credit rating agency who will have crunched the numbers and produced a sequence of letters determining the quality of credit. As an example, Bank A and Bank B wish to transact with each other. Bank A says please send me $100 million and I will send you €90 million. The issue in banking is someone has to go first and send their money hoping in the meantime the other bank doesn’t go bust before sending their piece. Entire departments in banks exist with people assessing and obsessing about this risk and they assign a cost to it. The cost is simple, what is the percentage chance of Bank B going bust while we wait for our side of the transaction, multiplied by the transaction size. So, lets say it is one in a million, for this transaction alone the cost of the credit risk is $100, not a lot but not trivial. When you consider the total value of such transactions in a year it is enormous, daily foreign exchange markets transact around US$5 trillion per day, then our one in a million chance of default (if that’s what it is) costs about $1.8 billion per year.

Actually, the risk of bank default is probably much higher than one in a million, since that fraction would imply banks last 2,700 years before they go bust, I think we know it’s rather less and thus the value of the credit risk market is orders of magnitude higher than $1.8 billion. (As an aside, I wrote some weeks ago about the recent bail out of Banca Monte dei Paschi di Siena, it happens to be the oldest bank in the world at slightly over 500 years, it has a credit rating of B1, the junkiest of junk bond ratings).

This problem of transaction credit risk has now been solved. In cryptocurrency, the technology now exists to simultaneously confirm that a counterparty has the balance of money they say they have and to execute the transaction. In our example, Bank A and Bank B are able to check that each party has the $100m or €90m and swap them instantly. It’s called an atomic swap and essentially involves the exchange of private keys on a blockchain, in effect you swap the access code to the counterparty asset without ever revealing your own access code.

Transaction credit risk in transactions like these not only costs many billions of dollars a year but supports tens of thousands of staff who do what cryptography can now do for them. Atomic swaps are currently operating at a level similar to bitcoin in 2009, for geeks and enthusiasts only. Almost nobody has heard of them or understood the impact they will have on credit risk. Atomic swaps will revolutionise finance because they solve a very real and very expensive problem that is encountered by millions of people, millions of times a day. It will be worth a lot.

Is Australia copper bottomed?

Copper has its longest losing streak since 1971

So, it was with considerable interest I looked at the Reserve Bank announcement about interest rates on Tuesday. The market expected that they would remain on hold at 0.75% and that’s exactly what happened, however:

- The Central scenario is for the Australian economy to grow by around 2.75% this year and 3% next year which is an increase on the last 2 years

- Consumption growth is expected to pick up gradually

A letter

The letter is 140 pages long, so I will spare you the detail other than to say that bitcoin and cryptocurrency featured in that report. Specifically calling out to the high net wealth recipients that as far as bitcoin and crypto are concerned.