One of the major use cases of decentralised blockchains that has been heavily hyped by institutional investors has been Decentralised Finance — or “DeFi”for short. DeFi is essentially the analog of Traditional financial services for digital assets implemented on top of decentralised networks (thanks to Coinfund’s Jake Brukhman for that definition here). The disruptive potential of DeFi is has long been considered part of the impetus for Crypto — as the old (or new) saying goes “Long Bitcoin, Short the Bankers”.

In practical terms, both Bitcoin and more specialised DeFi systems are a long way away from genuine Schumpeterian disruption, but the recent growth of two platforms in particular give a glimpse into the potential of this area. These two platforms are the MakerDAO protocol and Compound, both DeFi systems (although compound less so) designed to provide basic frameworks for digital asset financial services.

MakerDAO – The first decentralised stable coin

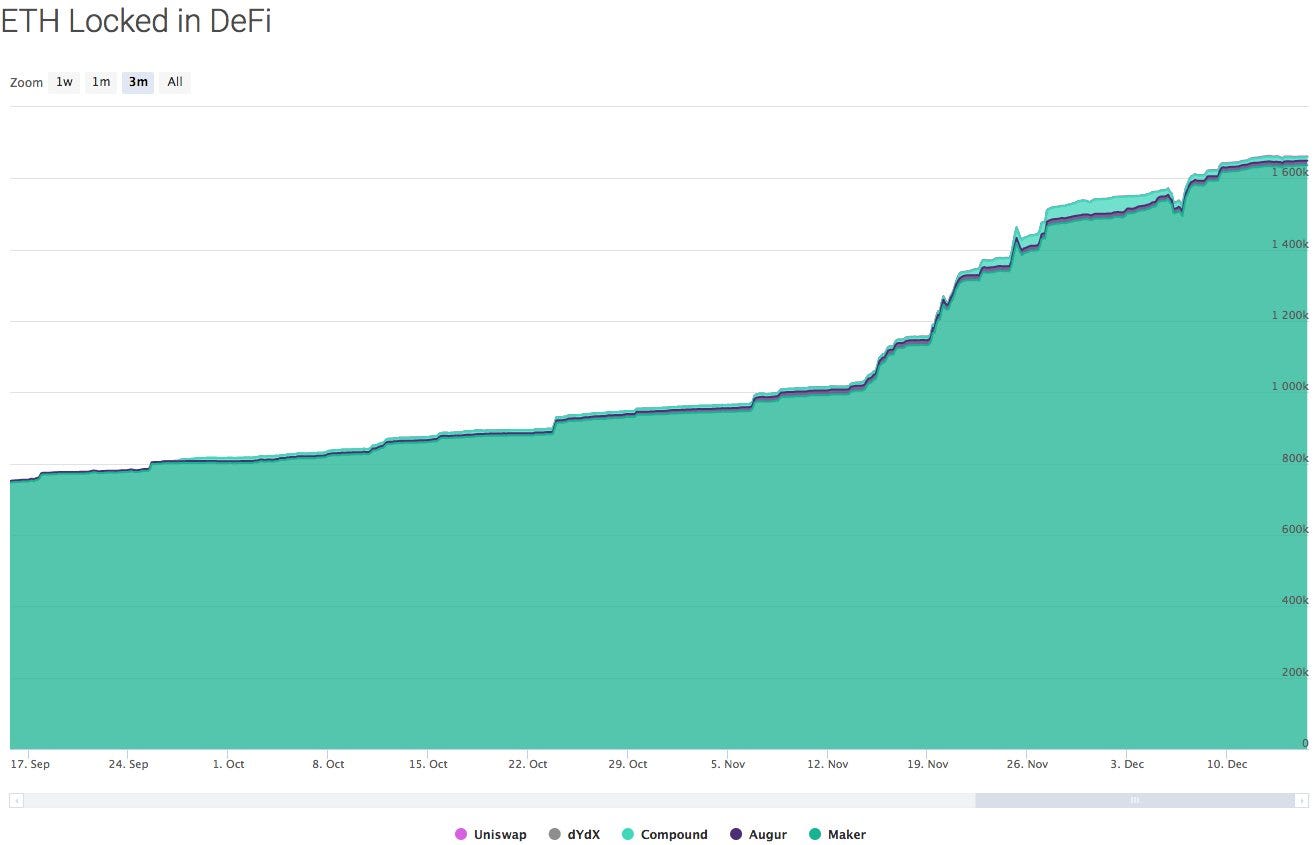

A key story-line out of late 2018 was the rapid growth of the Maker protocol on Ethereum, a decentralised stable coin platform which doubles as a vehicle for collateralised lending. Maker has emerged as the clear market leader in the provision of DeFi so far, as the green area on the graph below shows the relative amounts of Ethereum locked up in different DeFi platforms (the huge dark green section is Maker). Launched at the end of 2017, the Demand for newly minted Maker DAI has reached a level where it almost exceeds new Ethereum on a day to day basis.

To give a basic explanation of the protocol’s function consider the following scenario:

An individual wishes to borrow stable value currency (typically fiat) against the value of their cryptocurrency holdings — they may require fiat for some arbitrary reason, the main thing here is that they do not want to sell their cryptocurrency. They can open a position on the Maker protocol called a Collateralised Debt Position (CDP), where their cryptocurrency becomes collateral for the issuance of DAI, Maker’s stablecoin currency. Individuals currently have to lock up 150% of the value of their stablecoin loan in Ethereum (in USD terms) with the on chain price set by an oracle system implemented by the DAO. A liquidation price in Ethereum/USD terms is struck at the time the position is opened — and the CDP is liquidated if the Ethereum price drops below that amount. The Ether locked in the CDP can also be recovered by paying back the DAI issued, thus closing the position.

Given the stablecoin is decentralised, the mechanism which maintains the DAI’s 1:1 peg with the USD also is relatively sophisticated. The system is designed such that there always an arbitrage incentive to trade the DAI at 1$ — if the price falls below 1$, individuals with open CDP’s can buy DAI and free up their collateral for a profit. If the price is above 1$, individuals have the incentive to open CDP’s and sell their newly issue DAI for a profit.

Interestingly enough, the major point of interest for many investors and CDP users is not necessarily the utility of a decentralised stablecoin, but instead the ability for the protocol to provide leverage. Because CDP’s issue DAI, individuals can simply sell their DAI on an exchange, convert it into Ether and open a new CDP with that currency. Repeatedly doing this can generate significant leverage for the investor, increasing their returns on Ethereum on positive Ethereum price action and potential losses on corresponding negative action.

Leverage certainly isn’t a new thing in crypto or traditional finance, and it is fairly common for people to enter leveraged investment positions. The problem is the rate at which leveraged positions in CDP’s and Ethereum are growing, and the potential risks that poses to the network’s long term health. Concerns about the influence of large CDP positions on Ether prices are common — as the tweet thread here shows an almost exact correlation between the closure of large CDP positions and significant declines in ETH/USD pricing. With an asset as volatile as Ethereum, the potential implications of a sharp decline in Ethereum price are both real and likely to occur — if many of these positions reach their liquidation prices, its plausible we see a huge decline in Ethereum prices in the short term. For anyone following Ethereum price action in the short term, I would recommend following the Maker DAI twitter bot. It provides live updates on large scale positions being closed, opened and liquidated, all of which seemingly have a disproportionate influence on Ether prices as of right now.

That said, the protocol itself has significant safeguards on its stablecoin’s peg in the event of a large scaled liquidation event like this — and the expansion of Maker beyond just Ethereum will see its own success diversified from simply the success of the network. As part of the greater push for DeFi applications, Maker is probably just a precursor to a suite of more sophisticated tools, as its simplicity and reliance on collateral are well suited for the current stage of the digital asset ecosystem.

Compound – The first cryptocurrency lending platform

Currently a distant second in the DeFi stakes, Compound is a product of significant venture funding from Bain Capital, Polychain Capital and Andreessen Horowitz (a16z). Its offering is a digital form of the money market, providing a facility for individuals to both lend and borrow cryptocurrency for the purposes of short time horizon loans. Strangely enough, Compound is considered a DeFi product by many in Crypto despite being a centrally controlled organisation, mainly because of its financial offerings being based around decentralised digital currencies. Regardless of its labels, Compound — or rather, the type of product Compound offers — looks to be an important part of the future of the ecosystem.

The basic mechanism by which Compound functions is in the lending and borrowing of digital assets at a floating interest rate. The Compound business model operates by taking a small residual of all transactions passing through their protocol, and they provide the same security services as reputable exchanges. For users, lenders and borrowers interact in the open market to set interest rates for assets, allowing the floating interest rate to be entirely market set.

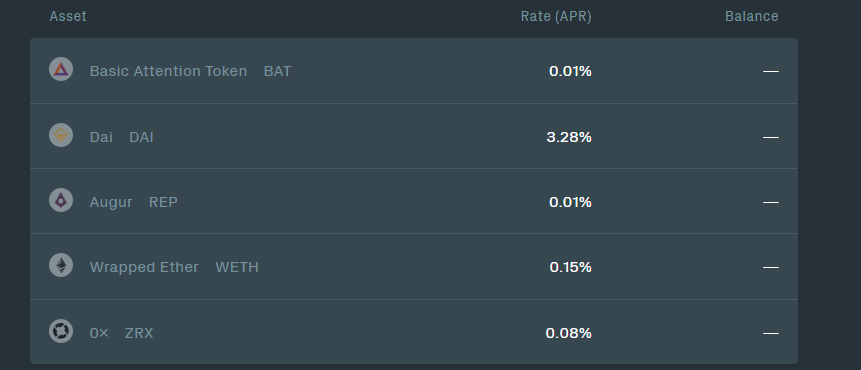

Given only the above assets are available on the platform, it is reasonably surprising to see the volumes that Compound handles — as the assets on its platform are not particularly widely used other than the DAI. BAT, REP and ZRX are all utility tokens for which there are an abundance of without genuine uses for (all 3 networks have relatively low usage), and WETH is a privately pegged form of Ether.

An application commonly explored for compound is in the maintenance of utility token based networks, where the use of tokens is critical for a protocol’s health or function. In a world where utility token based dApp’s are successful, Compound most certainly would serve as a short term money market for individuals looking to get involved in these networks — consider the example of BAT, an advertising based utility token. The Brave Network plans to launch an advertising model whereby ads are paid for in BATs. An Advertising agency could then take out a short term loan on compound in BAT to pay for the advertising, with the loan acting as a hedge in volatility of the price of the currency, as all compound loans are struck at the value of the currency at the time of the loan. Given many of these applications will require significant adoption from individuals who aren’t looking for huge cryptocurrency risk exposure, services like this are important for bridging the gap between them and cryptonative products.

The major issue with Compound is its centralisation. It hasn’t solidified its position as the key lending protocol of Cryptocurrency other than Maker and its position in the market will be challenged heavily by decentralised alternatives such as Dharma (and even Maker to a lesser extent). Its success in the short term has been based almost entirely on its UX advantage on the rest of the market (venture support will help with that), but the lack of concrete success in utility token applications have left liquidity and usage of the protocol lacking. Its fairly likely that Compound loses both its UX and liquidity advantages by the time we see significant dApp adoption, putting its long term success in serious jeopardy.

Regardless of whether either of these protocol’s succeed in their long term goals, their short term success is promising given the surrounding market conditions. The possibility of more complex and improved products coming in the future makes DeFi one of the more exciting areas in Crypto, especially from an institutional investor point of view. We expect this to be a big growth area in both the near and long term, as these offerings are introduced into the space.