One of major hurdles to online commerce today is the difficultly in empowering individuals to control their own online information, including proving their identity. The potential for smart contracts and their associated platforms to provide a secure and efficient way to manage digital identity is a major source of investment and research in the blockchain community.

Digital identity is widely defined as the information on an entity or individual that is available online. Currently, the fragmentation of an individuals information across a wide variety of platforms causes major problems for both individuals and companies. The key factor here is in how companies manage the data they are legally required to use in order to comply with KYC (Know your customer) requirements. In simple terms, customers are often required to send personal data/information to companies who use that to verify their identity online. Individuals must trust that companies have the infrastructure to handle and secure their personal data, whilst companies must minimise costs and verify information securely and efficiently.

Companies increasingly do not seem to have the infrastructure to consistently handle personal information, as the value of black-market identity information drives hostile actors to attack vulnerable handling processes. Even with increasingly publicised data breaches, we still see mishandling of information to the extent that significant personal information is being exposed to hackers. An example of this can be seen in Fitness giant Under Armour’s MyFitnessPal having its data compromised in March of 2018, with personal information of users being stolen by hackers. For most companies it is simply too costly to build secure systems for managing and verifying user identities securely. With legal protections coming to users in the form of the GDPR and other user-centric regulations, that cost is only increasing, making a blockchain based third-party solution more attractive.

The key for any blockchain project wanting to succeed in this area is to provide a proof of identity solution that works with data on chain. Being able to have a personal profile of data stored on the blockchain provides a layer of security not available to a typical database system. Profiles are linked to individual public keys, meaning only a person who can prove their ownership of that public key (i.e. have the private key) can prove they own the corresponding digital identity. A number of projects have already begun development along similar ideas:

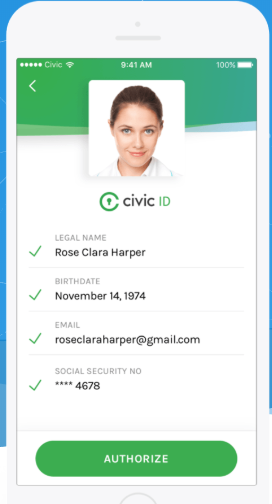

One project providing a way to securely store user data using a decentralised application is CIVIC, a reusable digital identity profile for customers. Raising US $33 million in funding via its ICO, Civic provides a method for users to send their documents and personal data to a digital identify profile on the blockchain using those verified documents. This profile is usable across any company that wishes to use Civic, meaning users only have to expose their data at a single company, whilst still fulfilling legal/compliance obligations. Companies save significantly on managing and securing user data, and users have a safer and easier way of handling their own digital identity. Civic’s major issue at the moment is adoption, as the project does not address major pain points unless it becomes widely used by companies to manage KYC, and thus more convenient for users to maintain.

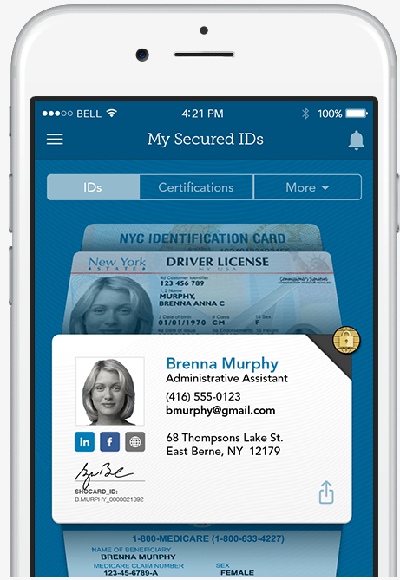

ShoCard implements a similar approach, using a blockchain based digital identity verification and authentication process. Again leveraging the security of blockchain based storage, ShoCard extends a typical KYC processes to provide enterprise services utilising on chain security protocols. An example of this is in ShoCard’s banking service, providing banks with the ability to digitally sign credit certificates in order to provide blockchain verified individual credit reports. The ability for enterprises to provide secure proof of identity is a critical development for secure online transactions and information management. ShoCard similarly suffers from a lack of adoption in the same way Civic does, although its enterprise applications provide an interesting use case for companies looking to integrate blockchain into their processes.

Beyond these platforms, smart contracts can also provide the means by which individuals can ensure they are doing transactions only with verified parties. Whist implementations of projects like those above provide a means by which to link people to accounts, smart contracts provide the means to utilise those accounts in productive contexts — meaning these identities can quickly become integrated into IoT applications, making them vastly more powerful.

A ubiquitous blockchain identity platform would have widespread growth implications for blockchain, as the issues of digital identity are not just limited to those discussed here.

Check back next week for more.