One of the major characteristics driving innovation in blockchain is the prevalence of open source projects. Making protocol code accessible to community developers has seen massive acceleration in the technological development of networks. Whilst this system may be good for the development and evolution of protocol technology, it hasn’t been able to facilitate the creation of successful blockchain based applications (so far).

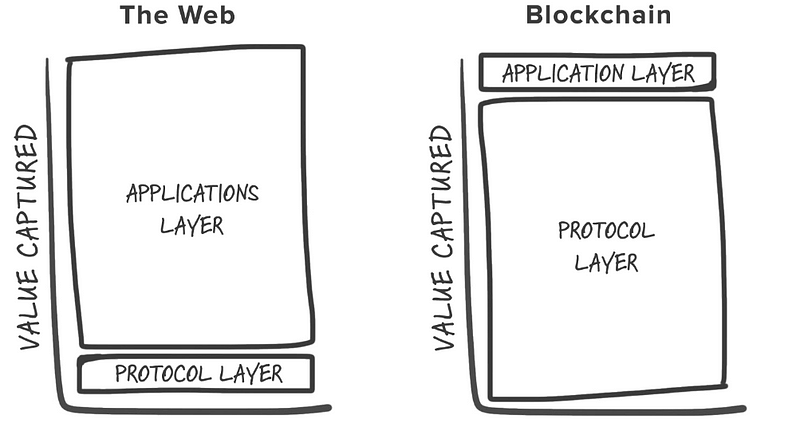

Application developers have seldom (if at all) been able to genuinely monetise open source decentralised projects, typically because of the problems caused by having code publicly available. The constant threat of having code taken and utilised by a competitor invalidates some of the incentives that would exist for first movers in a traditional non open source context. Margins on the provision of services become very small, such that traditional avenues for monetisation are not effective. These issues have led investors to come up with the Fat Protocol Thesis. The Fat Protocol thesis states that value capture in blockchain is concentrated at the protocol level (hence ‘fat’ protocols), rather than at the application level.

This theory has certainly held true so far, given the comparative market size of protocols versus the equivalent market for blockchain applications. However, it is difficult to suggest this will continue into the future with any certainty, given the immaturity of the protocols that these applications are built upon. For a realistic gauge on what a successful blockchain application looks like, there first must be a protocol layer ready to facilitate the applications success.

One key development that presents a possible opposition to the Fat Protocol thesis is the Utility Token. Utility tokens constitute application level cryptocurrency that can be used in exchange for some degree of value from that application. Think of the popular prediction project Augur, and its utility token REP that can be used as a currency to wager with. Token sales are a lucrative exercise for applications, permitting them to both raise funds for future project development, and also to monetise their future growth.

Utility Tokens are a key piece of application design, as the ability to create the most efficient tokenomics for a particular project is key in ensuring its long term viability. In an open source decentralised context it becomes critical that an application’s token model incentivises token holders be engaged as participants. Using tokenomics effectively should lead to the application’s tokens generating network effects, whereby users are rewarded for using the platform and token holders are rewarded for increased application adoption.

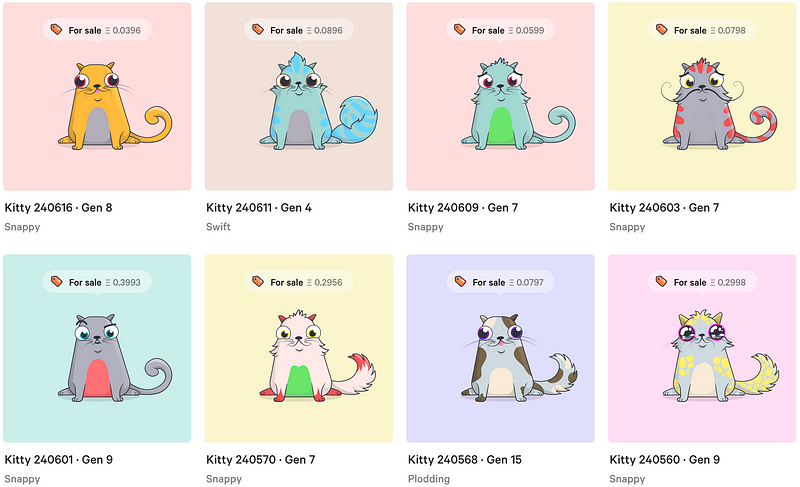

Example #1: CryptoKitties

The CryptoKitties application is a great example of a project successfully developing tokenomics to match their product. CryptoKitties constitute a utility token because they provide an implementation of the projects service — the provision of collectable digital cats. Each digital ‘kitty’ represents a non-fungible token (defined by the ‘awesome collectables’ standard, found here) which can be traded to other users on the ethereum network. Token holders are rewarded the privilege to breed and create new Kitties using their existing ones. As the application becomes more popular, individual Kitties appreciate in value, thus generating the network effects required for long term adoption. The major limiting factor for CryptoKitties was/is the protocol, as its reliance on the Ethereum network created bottleneck issues for not only itself, but the Ethereum network as a whole. Even with those issues one of these CryptoKitties sold for US $170,000, demonstrating the value of tokenised collectables.

Example #2: Steemit

Steem is a content creation platform based around blogging and social networking. Its token STEEM provides the basis for rewarding network participants for both content creation and curation. The community decides the distribution of token rewards based on the votes of users who hold ‘Steem Power’. Curators and creators are both rewarded on the basis of the quality of their contributions to the network. As users are continuously rewarded for participation in the network, and the value of those rewards scales with the number of uses, Steem’s token model effectively encourages the generation of network effects.

Example #3: Augur

Decentralised prediction platform Augur is designed to provide a basis for markets on predicting the outcome of events. Its utility token REP serves as the basis for its settlement mechanism, as markets are settled by participants of the network voting on the outcomes of each market. Participants are rewarded on the basis of the ‘truthfulness’ (relative to consensus) of their votes, meaning there is a clear incentive to participate honestly in market settlement. Because the valuation of REP scales with the amount turned over within Augur markets, as the Augur network becomes more popular — the value of REP increases. Thus, the Augur token model generates the network effects required for long term value growth in the REP token.

One of the key issues for these open-source projects to tackle is the legal classification of their token issuances. Regulators currently have very few guidelines for the classification of digital assets, and the penalties for issuing a token that later is designated as a security are severe. Project creators thus have to tow the line between rewarding participants for application use and the potential legal repercussions of having their token classed as a security. In the longer term, regulators will develop a better understanding of these digital assets — presumably leading to a more efficient approach to defining and regulating what a token constitutes.

Utility tokens represent an important step forward for blockchain, as their ability to generate value for investors and funding for projects provides a strong incentive for open-source application investment. In situations where investors would otherwise not be able to monetise their investments, they can now capitalise on the success of these applications.

The question is whether utility tokens can survive without the traditional income earning characteristics of equity or debt. They need to avoid securities law and yet still generate value for investors, it is hard to do and it remains to be seen how many projects can successfully achieve this goal.