- 43 million customers worldwide

- $456 billion in transaction volume to date

- 1,200 employees (amazingly small)

- Interestingly, no headquarters. They all work from wherever they like

- First 9 months of 2020

- $691 million in revenue

- $141 million of net income

- The most recent batch of 127,000 shares was sold Friday at $373, which works out to a valuation of $100.23 billion

Direct listings are slightly unusual in that you cut out the middle men. Existing shares are sold directly to the public, no new shares created, no dilution for existing shareholders and no new capital for the company.

You can only do this if you have massive confidence and deep pockets, which Coinbase clearly does. The current valuation makes this the biggest listing since Facebook.

From our perspective we want this to fly for a number of reasons. Mostly that the listing legitimises the whole industry, signalling that the USA is finally ok with digital tokens being sold to retail clients. The more distributed the shares become, the less likely politicians do something silly.

It is a big, big moment of validation for this industry, hats off to Coinbase.

It was December 5th 2019. I wrote here about a then little-known Federal Reserve governor, Lael Brainard who gave a speech about using an average inflation rate rather than a hard 2% target.

“Fed Governor Lael Brainard said her idea would see the central bank change its target, after sustained periods when inflation has been below 2%, to a similar level above 2%, and tell the public that inflation would run higher for about the same amount of time.”

Little was made of it at the time, however since then what she described as “my idea” has morphed into formal Federal Reserve policy.

We now know, and are repeatedly reminded, that the average inflation rate will be what matters and that average will be calculated over an unspecified period of time. For example, if CPI were 4% the Fed might do nothing for quite some time.

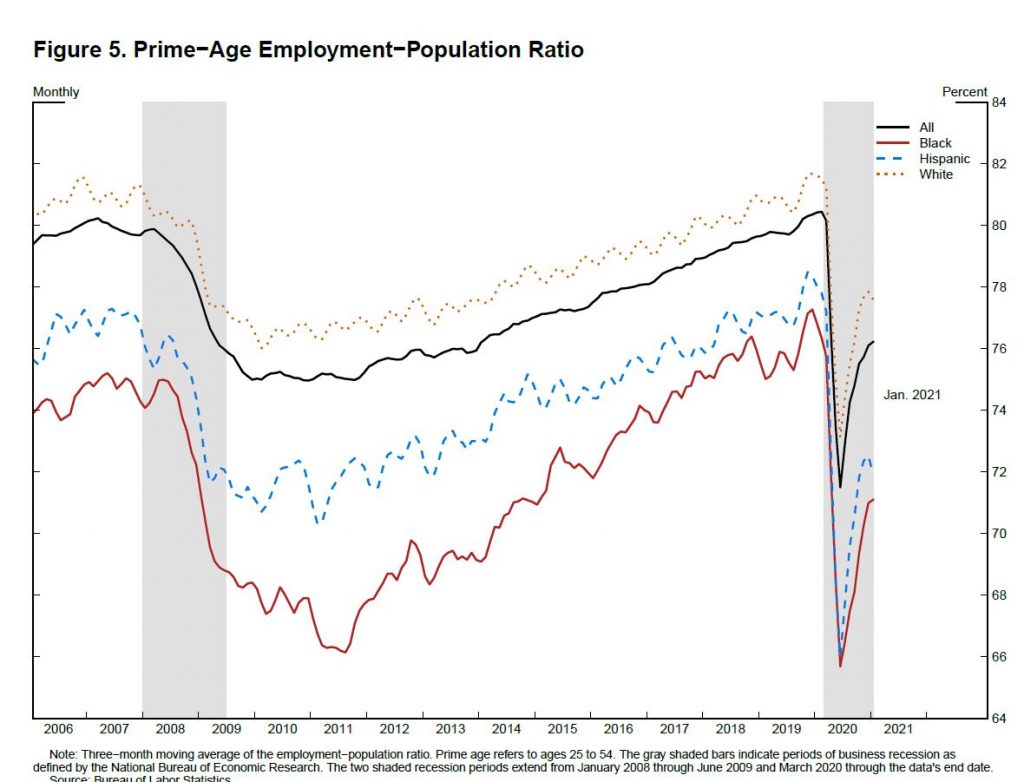

Last week Ms Brainard gave another speech. This time about employment. The main thrust of which was that employment in the US has recovered but not evenly. The less skilled are doing much worse and in particular the Black and Hispanic experience is very much worse.

Here is the crucial policy change:

“The new framework calls for monetary policy to seek to eliminate shortfalls of employment from its maximum level, in contrast to the previous approach that called for policy to minimize deviations when employment is too high as well as too low.”

and further:

“With these changes, our new monetary policy framework recognizes that removing accommodation pre-emptively as headline unemployment reaches low levels in anticipation of inflationary pressures that may not materialize may result in an unwarranted loss of opportunity for many Americans. It may curtail progress for racial and ethnic groups that have faced systemic challenges in the labour force”

What inflation rate will bring the overall participation rate close to the maximum? Assume the maximum is 82% ish as on the chart above. How much inflation is required to get Black and Hispanic employment from 72% to 82%?

Once again then, a major policy change has first been announced by Lael Brainard. She seems to be the one with the ideas and she takes some personal risk in being willing to announce them, and indeed claim them personally. Full marks to her for that.

This is the biggest policy change since the introduction of QE. It implies a participation rate increase of 10% in specific ethnic groups (which is huge and normally takes a decade) would need to occur before the Federal Reserve moved meaningfully to raise interest rates.

Banker: “Can you explain why you said on the form you spend $500 per month on electricity when in fact you spent $502?”

Borrower: “I provided an estimate”

Banker: “I am required to provide explanations in our computer program for variations from estimates, what should I say for this one?”

Borrower: “I used more?”

Banker: “We will need more than that, is this a trend, this using more, or a one off?”

Borrower: “Last Friday I stayed up late, I was reading a book, the lights were on longer than usual, it is not a trend”

Banker: “Thank you. I notice your gas bill ………”

….and so it goes on. They want everything really and the experience can be rather unpleasant.

Contrast that with the government experience. When they borrow there is queue to lend. You might think they too would face awkward questions:

Bond investor: “You seem to have overspent on your nuclear submarines by roughly $300 billion, can you explain?”

Treasury: “we left the lights on while reading the submarine manual on Friday night, it is not a trend”

None of that happens though and for decades US bonds have been mopped up like the oil of the global economy, which in some ways they are. Every bond auction is oversubscribed many times and they run rather smoothly. No documents or explanations about overspends required, in fact they are barely even required to pay interest at all.

On Thursday last week the US Treasury was selling $62 billion of 7 year treasury notes and guess what? The market wasn’t so keen to lend for seven years at almost zero.

“A big move came in the early afternoon when an auction for $62 billion of 7-year notes by the U.S. Treasury showed poor demand, with a bid-to-cover ratio of 2.04, the lowest on record according to a note from DRW Trading market strategist Lou Brien who called the result ‘terrible’.”

The bid to cover ratio is the dollar value of bids divided by the value of the auction. A strong auction can have a bid to cover above 10 (generally only for the shortest term bonds) but anything close to 2 is bad.

Either this is temporary because of last weeks bond market wobbles or the US Treasury has a serious problem. They will be nervous. The next big tests are Wednesday 10th March and Thursday 11th with 10 and 30 year securities being auctioned.

Since Monday we have had some big statements from Central Banks about the bond market wobble. The ECB with its extraordinary “we will not tolerate higher rates”, the Australian Reserve Bank did rather better buy actually buying a lot of bonds and suppressing the rate rather than just talking them down, and the Fed mumbled about accommodative policy. It will work for a while longer yet, but it cannot work forever.

Possibly the last decent newspaper in the Western World has a rather compelling angle. They hate bitcoin. I think that is appropriate, after all the bankers of London don’t want some “funny money” ruining the racket. For hundreds of years now the Bank of England has looked after things fabulously and they’ve all been at lunch by noon, which is absolutely the way it should stay. The FT is a business after all so they have to keep the audience happy.

They have ramped up their efforts this week after those dreadful Americans at Citibank wrote a rather glowing report on bitcoin, which to be fair was a bit over the top.

We should welcome the relentless the bitcoin bashing. The system needs to be sufficiently robust to survive. If you need journalists to say nice things about you, something is probably wrong.

Contrast the experience with the bond market which at the slightest whiff of trouble has every power player in the world doing everything they can to help it.

The FT’s main beefs were that Citi overstated merchant adoption of bitcoin (true, they did) and that USDT is some sort of criminal enterprise which prints “lookalike dollars” because the New York Attorney General investigated them. Well, Tether just paid $18.5m to the NYAG, admitted no wrong doing and will now prove they have full reserve backing each quarter, they basically won their case and the NYAG backed down. You can’t ask for much more.

Our FT journalist has been against bitcoin for a very long time too.

Oh how they laughed in 2014. The bitcoin price was $550 at that point and it had risen 20 fold in 12 months, everyone was in Dutch Tulip mode. “We should put it in our pension funds hahaha”.

Haha indeed.

As to the offending report from Citibank, its here. It’s interesting even with the adoption rate typos.

Euro-Trash

In bad news for Christine, Super Mario is back. He becomes Italy’s twentieth Prime Minister of the last forty years. By contrast, Germany has had only three Chancellors in that period. Kohl, Schröder and Merkel.

Draghi knows the inner workings of the ECB very well. Indeed he no doubt commands lot of loyalty still inside that institution. What will happen when Italian borrowing rises above agreed limits? Will Italy be sanctioned by the EU? will bond yields diverge? I doubt it.

For the ECB this is the worst case scenario, the man who knows the playbook is now running the country that poses the greatest risk to the Euro. He absolutely knows that they will do everything to make sure Italy stays in, especially with him at the helm. So he can spend and do whatever he likes using the European balance sheet rather than just the Italian one.

Hats off to the Italians. Just like in soccer, they work with the rules not against them. Appointing Draghi is like getting a penalty in the 90th minute after a fabulous dive by one of your favourite strikers.

As for Christine, I feel bad, but when you are a sleazy overpaid political player, there’s always a bigger oil slick to take you down. He’ll play her like a banjo, can’t wait.

Former members of the band “QE Infinity” announce their comeback tour