Consensus

Is it time to jump on the “Bitcoin bandwagon” asked the AFR. Their full article here is not unreasonable; urging caution and small allocations.

“Most advisers, and their licensees, will give them a wide berth at least until there’s a solid performance track record, and an ‘investment grade’ asset consultant rating,”

Even now, with an SEC approved ETF and a track record like no other asset out there, apparently advisors will still be giving bitcoin ETFs a wide berth. There was no shortage of advisers lining up to be quoted either, pointing out volatility, and that it can take a long time to recover from crashes. Small allocations, not get rich quick, etc. I agree with their comments and yet it all missed the point.

The world is going digital. In the physical world you need intermediaries and regulators to secure your assets for you. You need hundreds of years of common law precedents so you can broadly rely on the system to do what you expect it to do.

In the digital world, we are watching cryptography and mathematics replace that whole infrastructure. Trustless (crucially) peer-to-peer exchange is now real. Bitcoin, like gold, is not the liability of another entity (like equity or cash) and you can own and operate it entirely independently of everyone and everything else. That concept is new and brilliant because digital property rights now exist and they are personally enforceable.

This point seems little understood and I have never seen it discussed in a serious article from a mainstream financial newspaper.

The idea that one might wait until an ‘investment grade asset consultant rating’ has been issued to bitcoin ETFs conflates the old world with the new. It’s like getting an aircraft signed off by a vet, because they know about traditional transport methods like horses.

My elevator pitch would have been: Unencumbered waterfront digital property is for sale; enforcement of property rights by mathematics. I would have followed up with a series of book recommendations, namely The Bitcoin Standard and The Sovereign Individual, and at least given readers a chance to understand the fundamentals of what is happening before suggesting they allocate anything at all. I think the deeper an investor’s understanding of the fundamental shift in the enforcement of property rights the more able they are to steer through volatility.

Let’s be honest though, if the AFR did things like that, what would be the point of reading this?

Vanguard

When the ETFs were lining up a few weeks ago, I pointed out that Vanguard was the largest asset manager who had not submitted an application.

That was fair enough. However when things launched last week Vanguard took things further and blocked their clients from having access to any Bitcoin ETF products. This I am less keen on. A brokerage platform is there to facilitate client trades, not make the trading decision for clients.

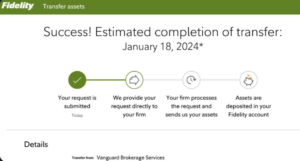

The uproar from Vanguard users has been immediate and #BoycottVanguard began trending on social media with clients posting their transfers online. Fidelity appears to be the winner, collecting a lot of new business as a result.

No issue at all with them not wanting their brand attached to a specific product, but to block everyone else’s when clients want to buy them feels wrong. I expect this decision will get reversed soon enough.

Even Jamie Dimon, who loathes bitcoin, has said “I’m not here to tell clients what to do, I’m here to help them do what they want even if I don’t like it”. Perhaps that’s why he has been CEO for 20 years.

Davos

This year’s edition of snow, private jets and cocaine is all about ‘rebuilding trust’. For some reason, trust in centralised institutions like banks and governments has fallen in recent years and our friend for Klauss is setting about to fix all that.

I get the sense that politicians in particular are wary about attending these days though because of the very obvious criticisms that will follow. Like, why do we take our lead from unelected bodies like this? What are you doing swanning around in Switzerland talking about solar panels?

To save you time, I perused the finest sessions and watched them online. The absolute low point was this one from Euro-Empress, Useless von der Lazy.

Special Address by Ursula von der Leyen, President of the European Commission.

It was awful. For the purposes of our amusement, I asked ChatGPT to summarise the transcript in tabular form “as though it were given by a dictator”. I must say I was so impressed, it’s very funny.

Great stuff. “Outlines her battle plan against nature” a particular highlight.

$100 billion

Speaking of building trust … Tether, the USD stablecoin of choice is approaching $100 billion in total issuance. During the dark days of 2022 they were put under serious pressure with huge withdrawals; they never blinked and met every single one.

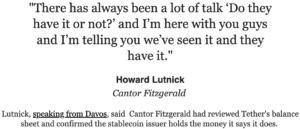

The doubters remain though. Does Tether actually have the money? Their audit reports can be found here and they lay out in detail the nature of the reserves; 75% of which sit in US Treasuries. As it turns out, those treasuries are managed for Tether by Cantor Fitzgerald whose boss happened to be in Davos this week.

Could it be more emphatic?

Doubters remain. In my book Tether has 100% reserves. American banks have a reserve requirement of 0%.

Take your pick but my guess is another US bank will fail before Tether does. Note they have 0.4% held in cash, so almost zero exposure to the banking industry. It’s a strange world where holding Tether is becoming a hedge.

Euro-Trash

With glorious timing the European Central Bank had one of its AMA Sessions last week (Ask Me Anything). The nominated victim was Board Director Isabel Schabel. Naturally, and to the evident frustration of the ECB, bitcoin questions dominated.

This one from BitcoinPleb, suggested that perhaps bitcoin might be superior to the incoming digital Euro. Isabel swiftly killed the notion of such a thing.

The bitcoiners would not relent though ‘Pummelpaffpaff’ enquiring, very sensibly, whether adding just a little bit of bitcoin might be sensible as a long term risk management strategy.

No because “liquidity, security and returns”. Interesting response, there are few assets now as liquid, none are more secure and the returns speak for themselves. The reality of course is the ECB only buys the toxic waste assets of banks across Europe, which have zero liquidity and they buy them for precisely that reason.

It was lots of fun though, because Bitcoin keeps coming up every time a Central Banker rears their head. It must be so annoying.

The story the ECB pedals about the Euro is just palpably false. Here Robin Brooks of the Institute of International Finance points out that the de-industrialisation of Germany is now gathering pace. Nothing else matters in Europe except Germany.