Super Mario

Windfall Tax

“Report finds”. Always a worry that. Who wrote the report? Do they have an agenda and do they have any understanding of economics?

In this case the report was written by the ‘Australia Institute’, who according to their website, are ‘a progressive think tank’. It’s hard to think there is another kind but it would be nice if regressive think tanks existed. Perhaps advocating for witchcraft and bloodletting, just for balance, obviously.

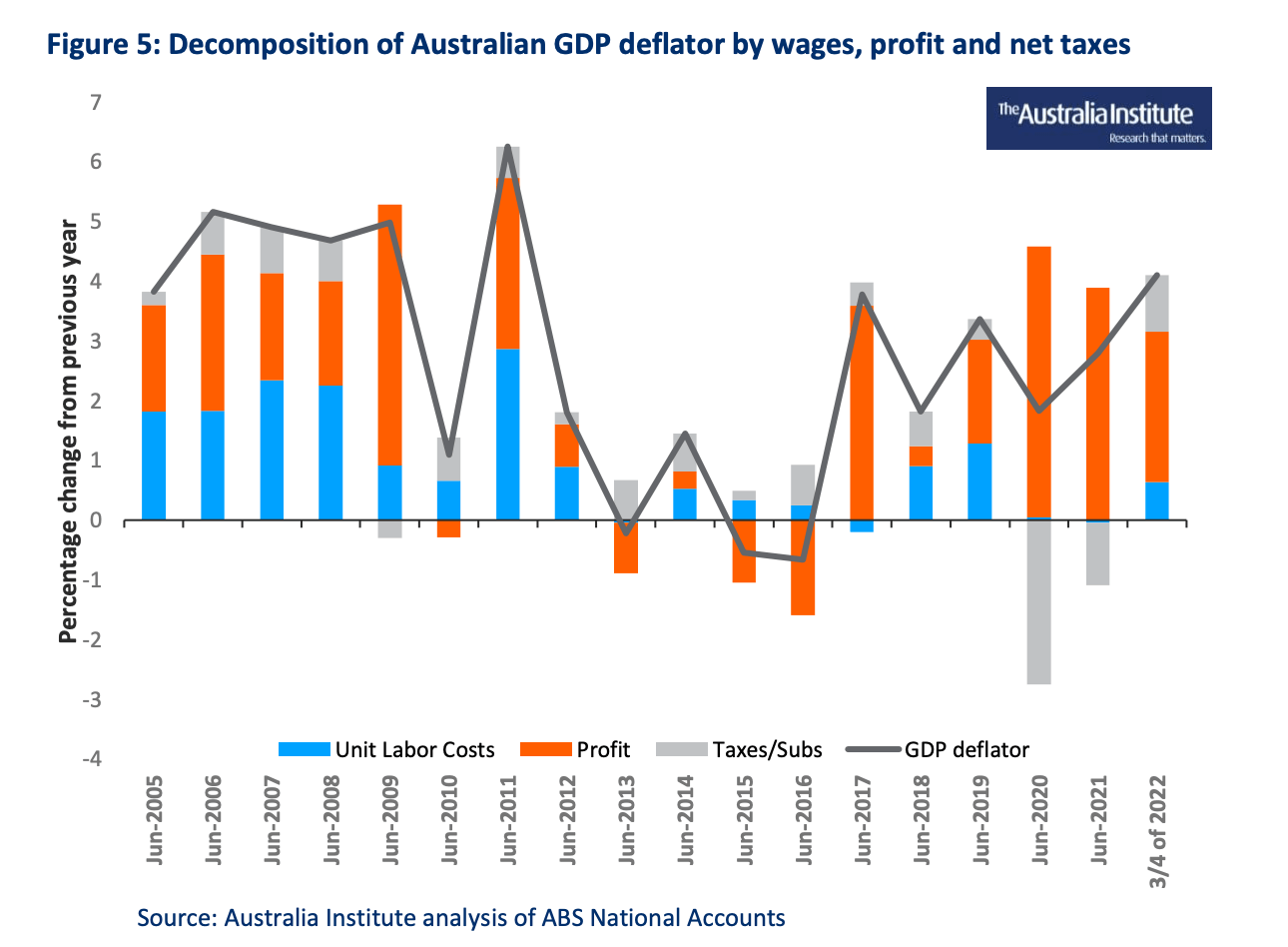

Anyway, profits are to blame for inflation, the report declares, because they are higher than they were and inflation is higher than it was. Here’s the “killer chart”.

Australian GDP broken down by wage growth and profit growth. One is bigger than the other so profit is to blame.

Even the European Central Bank tries harder than this. Correlation is not causation but in this case there isn’t even correlation. Profits are the result of everything else. They don’t cause anything. If anything, it is profit that brings prices down.

Case in point, avocados. Two years ago you couldn’t buy one for less than $4, leading to huge profits for growers. So more people grew avocados and now you can buy 2 for $1.

The whole setup blaming profits is gaining ground though. We have seen it with Biden bashing oil producers and even more dramatically with the UK imposing windfall taxes on energy producers.

It seems the narrative is being shifted. The setup is very much along the lines that times are getting harder and anyone making lots of money might be subject to a windfall tax. This week Nobel Idiot Joseph Stilitz was in Australia, he was advocating for exactly this:

Joseph Stiglitz, has said introducing a windfall profits tax should be a “no-brainer” for Australia, with the respected US economist pushing for the change during a meeting with Treasurer Jim Chalmers.

Speaking to reporters during his visit to Australia, Mr Stiglitz pointed out that a lot of companies made huge profits throughout the Covid-19 pandemic, along with electricity and gas companies profiting off the energy price rises as a result of the Ukraine invasion.

“It makes a great deal of sense at this current juncture – it’s not as if the energy companies did anything to deserve it,”

It’s all curiously timed isn’t it? The report blaming profits drops on the same day as Stiglitz lands advocating for the same thing.

Scary stuff. Even the claim “they didn’t do anything to deserve it”. What? They took risk; they allocated capital; they spent years on extraction and engineering; they worked on distribution. Would he be advocating for subsidies to them if prices went down?

The problem with all this is who decides what a windfall is? Is any consideration at all given the preceding periods where they might have been in difficulty and scratching by?

The fact is the state is now so large it is devouring everything in its path; there just isn’t enough money to fund all their projects and these tax grabs are likely to get more and more prominent. The dreaded words “report finds” is simply agenda setting by politicians.

All of this was predicted in a 1999 book, The Sovereign Individual, which surmised that the state would get so large it would resort to outright theft, either through inflation or seizure to fund itself. We see both prongs of attack now with money supply increases and windfall taxes (which are just seizure).

The book went on to predict (long before bitcoin) that the solution would be cryptographically protected assets. The seizures then stop because guns don’t work against cryptography.

Those days are now here. In the words of Satoshi Nakamoto “it might make sense to get some, just in case it takes off”.

Merge Time

…and did we need some good news. Of all parties to deliver it, the Ethereum foundation announced that their long planned ‘merge’ might happen in September. ETH is up 35% in the last 10 days on the news.

The merge makes some serious changes to the network moving from Proof-of Work to Proof-of-Stake. Aside from the arguments around the wisdom of doing this it has never been done before so if the merge is successful this will be quite a technical feat.

The changes should also permit a significant increase in the throughput of transactions on the Ethereum network. From 30 transactions per second to closer to 24,000. It’s unlikely this will be immediate given the technical challenges that lie ahead.

There are some second order consequences to all the changes too. The mechanics of mining on the Ethereum network will change a lot and we’ll see a lot of mining capacity leave Ethereum.

Any sign of success in this change will bring tremendous pressure from regulators and ESG advocates for bitcoin to make a similar change. That will never happen because the two networks are doing completely different things and in bitcoin’s case the proof-of-work is the value. The debate will likely be front and centre for a while, likely led by people with an agenda who otherwise have no idea what they are talking about.

The ETH price could run strongly here into the change, but the change is fraught with risk both short and long term.

Overall it’s positive. We will have the two biggest assets in the class with opposing consensus mechanisms and over time can compare. One will be favoured by regulators and governments. The other one will win but it will be fun to watch all the same.

Money has a cost

Apart from the fact the numbers are wrong, this is the first casual reference in the financial press to a ‘cost of production’ for bitcoin. It’s delivered in such a way that it assumes everyone knows there is indeed such a cost.

In fact, most pundits and financial wizards do not yet comprehend this profound fact. It goes to the very heart of the entire value proposition. You cannot fake bitcoins, nor can you cannot summon more of them at will. Money should have exactly this characteristic which is why for so long people used gold or its derivatives as money. They knew it was costly to produce and from such cost it derived its value.

The amazing thing is that the entire world goes to work every day for currencies that can be printed by somebody else. We all work in return for something that has a zero cost of production. Why we accept this is unclear and over the next few years more people will likely start to question it as the value of their dollars continues to fall.

The numbers themselves are nonsense though. The bitcoin hash rate has dropped by about 5% through June, so the cost of production has dropped by a similar amount. For most miners that is somewhere from $17,000 – $30,000. Those at the higher end of the scale will likely scale back production in the short term bringing things back to equilibrium.

In any event, the difference is profound. Bitcoin as an asset has a cost of production greater than zero. Every fiat currency doesn’t. If you wanted the value proposition in a nutshell; that’s it.

Euro-Trash

So, it’s the end of an era in Europe as Super Mario resigned as Italian Prime Minister. Losing an Italian PM is not normally news, but in this case it matters quite a lot.

Draghi was to some extent a compromise candidate when he arrived on the scene just over a year ago. His former colleagues at the ECB were delighted that there was someone in Italy they could work with to defend the Euro and do ‘whatever it takes’ as he so famously said.

Earlier in the week as the crisis in Italy unfolded the usual suspects in Europe piled in behind their man. The Financial Times trumpeted in its opinion piece over the weekend showing just how much Italy still needs him. It was all for nought, by Wednesday he was gone.

The dynamics behind this are not good. Italy has a huge national debt (140% of GDP), far in excess of the agreed limits of the Euro members. It has zero chance of reducing that burden too because its population dynamics are appalling. 1.27 births per woman is way below replacement rate and one of the lowest in the world.

There are similar dynamics in Greece and Spain but Italy is different because its economy and debt are so large. Germany can swallow all the Greek debt and suffer only mild discomfort. It cannot do the same for Italy.

Nobody understands the debt dynamics of Europe and the consequences for the Euro better than Drahgi and having him in Italy’s driving seat was a massive boon to the ECB.

The Euro broke parity with the USD last week standing at a 20 year low. It’s hard to see that weakness turn around long-term. Currencies ultimately are driven by trade and productivity. You must have things to sell and to have things to sell you need people to make them and sell them. Europe doesn’t have the people and its largest economy currently doesn’t even have enough power.

To make matters worse, overnight the ECB broke with its own guidance and raised interest rates by 50 basis points. The Euro ‘soared’ to $1.02. Better yet, the ECB, panicking about Italian bond yields which are racing upwards, unveiled yet another new tool called the Transmission Protection Instrument.

“Through no fault of their own”. Goodness me.

Quite the week for Christine and the gang. Perhaps the best connected politician in Europe is down the road (he really was smooth). The ECB has been forced to break its own guidance because its collapsing currency is driving inflation upward and quantitative easing has a new name.

As Master Yoda said, ”and now, matters are worse”.