The world is short bitcoin and long fiat. For 11 years that has been a horrible trade. Given the way that governments around the world treat our money it is likely to remain a horrible trade.

There is no limit to the number of times fiat currency can lose 99%. I accept that bitcoin is subject to that risk too. I think the risk unlikely but I accept it.

Do you accept that the Australian dollar or US dollar will almost certainly be worth 50% – 90% less in 20 years? That’s by the central banks’ own current projections of 2-3% inflation. It’s not me making it up, they are outright telling you if you are listening.

Adoption

We recently went through 3 million bitcoin addresses that hold something around US$1000+ in bitcoin. Any one person can have more than 1 address with bitcoin in it (and likely does). So it probably means somewhere around 1 – 2 million people have more than US$1,000 in bitcoin.

By any measure, that is almost nobody for a global commodity.

That is why bitcoin is cheap, but it won’t be cheap forever.

Money velocity

The economists among you will recall the equation. MV=PT

It states that the money supply (M) x Velocity of circulation (V) = Average price level of transactions (P) x the number of transactions (T). This theory was the basis for inflation concerns along the lines that if the government increases the money supply a lot, the number of transactions won’t change that much, and the price level will increase.

This is the basis of QE, we must have inflation of 2%+ so we increase the money supply.

Unfortunately, the least talked about factor, velocity, is not playing ball. As you can see in the chart the yellow line is collapsing and monetary policy is not as effective as a result. But why?

The answer is that the money being created since 2008 is trapped inside a financial ponzi. The Fed buys Treasury bills from some hedge fund or other, they then reinvest the cash in some other financial instrument that they deem safer or more suitable. Similarly in Europe, all the QE first goes to banks, who use it to bolster their own failing balance sheets, it never actually makes it to anyone who might spend it via loans. It’s very obvious that this is true because interest rates for Wall Street participants have fallen to 0.25% and less while credit card holders still pay 15% plus. Those with the weakest credit status have hardly benefited at all and velocity is in free-fall as a result.

Then Covid came. Governments gave money directly to households. In Australia, despite horrible economic statistics, household income actually rose in the quarter to June by 2.2.%. The JobKeeper/JobSeeker payments were really QE that bypassed banks and it worked.

It is pretty easy to see what happens next. The mechanism of direct subsidy to people who might actually spend the money is well and truly underway, that is Universal Basic Income. It’s here, we know from 10 years of QE and the Japanese experience that QE does not stimulate the economy. Far better to simply give money to the bottom 20% of earners in the country and you have a guarantee that they will spend it.

I suspect we are about to embark on yet another economic experiment where a lot of money is given away at both ends of the economic spectrum. Wall Street will have its QE and free money, the bottom 10/20% will have their free money too. Everyone in the middle will be in an almighty tight squeeze and asked to pay what will be an enormous bill. I can write the script for you:

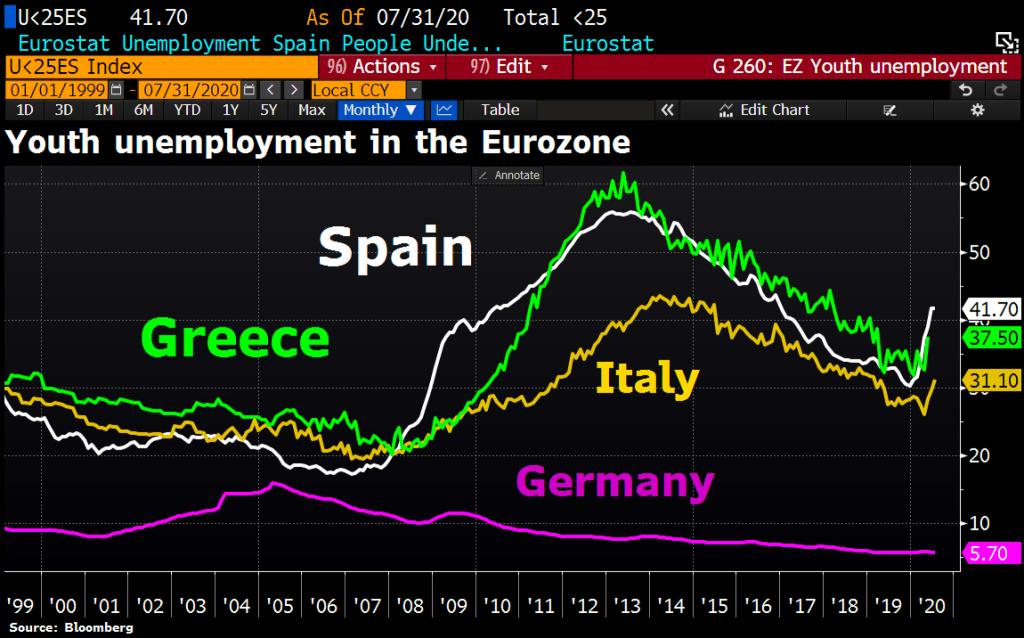

Youth unemployment in Europe’s south was always a problem. Even at the Euro’s launch it was 30%, then post 2008 it spiked all the way to 60% in Greece and Spain which both now hover around 40%.

The older generation in Europe are retiring, and many, many young people have never worked and never will. The people who pick up the tab for this are the Germans. Through their subsidisation of the currency and through EU transfers. It is true they benefit since they are the manufacturing powerhouse of Europe, and the purple line proves it. The young of Germany have relatively little problem finding work as a result, and good luck to them.

If you run economic experiments and they don’t work, the best thing you can do is admit it and move on. Not doing so is a huge price to pay to assuage political egos. It’s tragic and has consequences way beyond not having a job. Very low birth rates in Italy (2nd lowest globally), Spain (7th) and Greece (12th) are a direct consequence.

Topping the pile is Japan whose economic experiments went wrong long, long ago and still they do not reverse course. They have gone beyond falling birth rates with a now falling population.