You are not alone

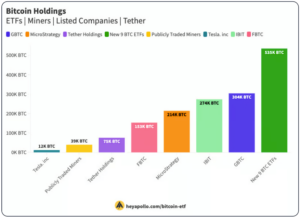

This is the first quarter since the launch of the ETFs where we get to see which hedge funds are holding bitcoin. It was a pretty special quarter quite honestly. For example, BlackRock sailed straight past MicroStrategy in holdings to 274,000 BTC. Across the chart, 8% of the bitcoin supply is represented.

Among the surprises were the Canadian banks. After the whole Trucker protest-with-bitcoin imbroglio of the Covid era, I was surprised to see them diving in. Franklin Templeton with $20m, Canadian Imperial Bank of Commerce has $7.2m. It’s tiny beans for them, but I think perhaps that is irrelevant since anything greater than zero means it’s approved for purchase.

At the other end of the scale, trading group Susquehanna has ploughed $1.3 billion into ETFs.

In Hong Kong, the Yong Rong investment group has IBIT (the BlackRock ETF) as its third largest holding after Nvidia and Tesla. Closer to home, Phil King’s Regal Partners tiptoed in with $4.3m of IBIT.

Most significantly, the state of Wisconsin revealed they hold $100m of IBIT in their pension scheme.

I think plenty of other pension funds will now follow and if they don’t, over time their members will surely be asking, why not?

Least worst

“Just” six months now until polling day in the US. The question arises who is the better candidate for our sector?

The answer on this became a bit clearer through the week as some Democrats (Elizabeth Warren in particular) continued their attacks and draconian legislative proposals.

Trump’s campaign has seized what they see as a political opportunity and decided to position themselves as “not against it”. It’s pure politics of course. Trump doesn’t care one iota for bitcoin, he just wants to win and see this as a possible way of shoring up some marginal votes. He is a self-confessed “dollar guy” and he won’t be doing anything as President that threatens or weakens the dollar but if it is a choice between openly hostile and not, then the latter would be a preferred option.

In the betting markets, Trump continues to shorten, now under even money to Biden’s $2.50. You would have to think given the age of the candidates and their specific political weaknesses then the market pricing any other runner at a 12% chance is quite generous.

Still, if it goes to the wire, purely from a sector perspective, Trump is preferred.

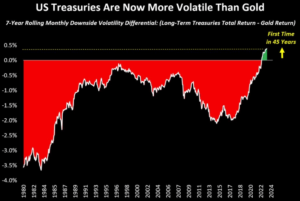

Gold got boring

Credit: Otavio (Tavi) Costa, Macro Strategist at Crescat Capital

Credit: Otavio (Tavi) Costa, Macro Strategist at Crescat Capital

For the first time in 45 years. Gold is more boring than US Treasury bonds.

Bonds have had an absolutely wild time this year as the level of issuance in the US spiked to record levels, but Treasury auctions have still been robust. We’ve been asking for years “who will buy the bonds?” and frankly we have been wrong because they keep rolling off the presses and the market laps them up, albeit at 5% not 1%.

The pressure is beginning to tell though. The US has begun rolling back its quantitative tightening; down from $60 billion every month to $25 billion. That adjustment barely warranted a mention but it is the equivalent of $100 every month for every American. Given the inflation pressures and the reluctance to crack the nut with interest rates, why reduce QT then?

There are some clues. Treasury Secretary Yellen for example has been busy, visiting China twice in April (which is unprecedented) presumably to ask them not to sell their bonds in response to their own liquidity difficulties. China, despite being a net seller for a while, still holds a lot of US Treasuries and could blow up the market if they sold. Then we have Japan, another massive holder. The Yen continues to weaken and the Japanese continue to do all they can to defend it. Again, they must be under intense pressure not to sell US Treasuries but they don’t have many options because they need dollars.

Solution? Swap lines. This article has some great charts about swap lines and their growth in recent years.

Imagine being Japan for a moment. They need Dollars to buy Yen and maintain the value of their currency. They could sell their US Treasuries for instant dollars but this would put tremendous pressure on rates and make it hard for the US to manage their budget. Instead then, use the swap line. Give us Yen, we give you dollars and you can buy as much Yen as you want.

It’s crazy in a way because essentially as the swap provider (the US) you get left with the depreciating currency, but it stops them selling your bonds. All you have to do is give them a load of dollars which you can print at will. It’s elegant, and for that reason expect these swap lines to get very large indeed; they are in fact a back door mechanism for ensuring the US can continue to pump the system with Treasuries without interest rates getting too high.

It’s also opaque. There isn’t much news about swap lines. Nobody understands them really and we aren’t going to be walking down the aisles of Coles anytime soon hearing people lament that “swap lines are effectively causing inflation through shared international currency debasement, now where is the Millel cheese?”

There’s no end to the financial innovations that can be invoked to continually devalue currencies.

Australia’s Budget

A rather embarrassing divergence of opinion this week after Treasurer Jim Chalmers set out his inflation forecast in direct contrast to the central bank.

Australian Treasury Sees Inflation Hitting RBA Target in ‘24

RBA has forecast inflation will stay above 3% until late 2025. Australia’s GDP growth is forecast to slow in upcoming budget

It’s not a small difference of opinion either. You might say “good, I hope he’s right” or you might equally consider that he has had a massive glass of hopeium and just wants to set things up for re-election.

Does it matter either? What is the point of having an Independent Central Bank if you never have a difference of opinion between them and the Treasury. When budget day finally came Jim poured fuel on the fire by giving every household $300 to address cost of living issues, which will leave Australia with substantial fiscal deficits for the next 2 years. $28.3 billion (1% of GDP) and then $42.8 billion (1.5% of GDP).

I must say though, most politicians appear to be chancers. They don’t actually have to live in any meaningful way with the consequences of their decisions, I think that makes them easy to read. They will try to get re-elected at the cost of longer term economic stability by avoiding the harder short term decisions.

Again, it just seems incredibly obvious right across the world that as government spending approaches 50% in the developed world (the US is 36%, Australia 38%, Japan 44%, Germany 49%, and France 57%!!) they will simply just print the money. There is absolutely no impediment to them doing that. $42.8 billion in 2026 is money just made from the magic in the sky.

There is also the distinct possibility that by disagreeing with the RBA, Chalmers turns out to be right. The RBA’s general level of forecasting success is appalling so taking the alternative view might pay off. If he’s right, then he’s right and if he’s wrong, well you got $300 which is great.

Euro-Trash

We got an update on the “Digital Euro” last week from the ECB Board. I find the whole thing very odd because the overwhelming majority of transactions in Euro’s are already digital.

The slides themselves do not actually consider the Euro itself as a comparator, rather the ‘Digital Euro’ has its capabilities compared to credit cards and cash as you can see below.

If we just focus on the comparison to cash. Person-to-person payments are already instant in Europe via the SEPA mechanism. This is even laid out on the ECB website, so the Digital Euro adds nothing there. Point of sale payments are also instant, so I’m not sure on the suggestion why “national schemes” don’t work. If you have a Euro bank account and debit card it works everywhere. The Digital Euro adds nothing again.

Finally, e-commerce payments. True, these cannot be made in cash but everyone in their right mind uses a credit card in case of fraud. I’m not sure why using an irreversible payment method like a Digital Euro is a good idea to buy goods that might never arrive.

It really is not obvious to me what the intention of the Digital Euro is in terms of ‘usefulness’ other than to phase out cash. The ECB has been emphatic in its insistence that cash will stay and I’m sure that’s true for now and will certainly not be true 10 years from now.

Another interesting notion “holding limits will be calibrated”. So, you will only be allowed so much Digital Euro otherwise it will put the retail banks out of business. I don’t find that terribly compelling either, surely I can convert all my Euros to Digital Euros and if not, why not? After all there is nothing stopping me converting it all to gold, or eggs, so why is there a limit?

The whole thing seems like a solution to a problem that doesn’t exist. There isn’t really a clamour from the general public for digital currencies either. Most likely, like me, they just do not understand it. Why? What will it enable that is currently not already enabled? It does not make sense. I expect it therefore to proceed at full pace.