Magic: The Gathering

A game of Magic: The Gathering

We need to discuss Mt Gox because over the next few months it will become intensely relevant.

A brief history. Launched in 2007, based in Tokyo. The name is odd and it stands for ‘Magic: The Gathering Online Exchange’ because its original purpose was for trading game cards in an online game known as Magic: The Gathering.

The game itself is still a big deal, played online with its own large ecosystem of enthusiasts.

The founder of Mt Gox got bored of The Gathering though and when he heard about bitcoin in 2009 on slashdot (which billed itself as a website for nerds) he pivoted again and it became a bitcoin exchange. Then it became, very quickly, the world’s largest bitcoin exchange.

Despite what happened next, this piece of bitcoin history is important. Right from the very start it debunks the idea that “nobody uses it” or “it isn’t useful”. Back then it was worth very little, almost nothing, but it was worth the small amount of compute that would have been used to generate it and interested people could relate that value to the exchange of game cards. In 2009, it was real and useful like it is today. Only a certain group of people grasped that reality because they had the technical skill to execute the exchange of coins (which was not easy then); but it could be done and they did it.

Anyway, the exchange roared ahead and by 2013 they were processing 70% of all bitcoin transactions. At that point the wheels started to come off. They were hacked, indicted by the US for operating a money transfer business, and in the end filed for bankruptcy protection. A bankruptcy process that continues today.

mtgox.com is now operated by the liquidator and full details can be found on the site of the process and where it is up to. The short version is by October this year, the 140,000 bitcoin controlled by the liquidator will be returned to their rightful owners, some of whom were teenage card traders in 2009 and will shortly become multi-millionaires. No doubt the bankruptcy was horribly painful, but I doubt very much they would have held bitcoin for this long unless the liquidator had done it for them.

The market will be noisy when this happens, maybe the price drops as very early bitcoiners rush for the exit and head to the Caribbean. For longer term investors, we need this one cleaned up. In the same way that the Craig Wright debacle hung over the industry, Mt Gox does the same. I’m looking forward to its conclusion. Beware the headlines that talk of bitcoin flooding onto the market when the time comes. It might be the last chance to get some at a reasonable price.

At the time Mt Gox nearly killed bitcoin. It took years to recover but it did recover and we should not forget the enthusiasts who flocked to trade cards with their niche online game. The people who had to tinker around with extremely awkward online wallets – they made bitcoin happen and when they get their bitcoin back I for one will be happy for them. Could they have imagined at the time that the likely buyer of their coins would be one of the largest investment firms on Wall Street? I doubt it.

Coinbase quarterly

They shot the lights out. $1.6 billion in overall revenue, up 72% from the previous quarter. Net income at $1.18 billion. EBITDA at $1 billion. Generated earnings of $4.04 per share against estimates of $1.15.

The chart presents the 2020 and 2021 quarters. Notably in those periods retail was delivering on average $130 billion in trading volume each quarter. In the quarter just gone, retail delivered about $56 billion.

So the results tell us two things:

Firstly, retail remains mostly on the sidelines at the moment and perhaps that will continue in a constrained interest rate environment. Secondly, Wall Street still does not really have a clue about the industry at all. I expect their estimates to improve over time but it is a very difficult industry to predict mostly because the assets have deeply unfamiliar characteristics.

For as long as it is misunderstood, I believe the sector will be a better investment than those areas which are better comprehended and perhaps more accurately priced as a result.

Too much cash

The problem of too much cash is a very real one for some companies. Apple, Amazon and Google all hold over $100 billion in cash. It sounds wonderful and perhaps a sensible solution is to just return it to shareholders. After all, inflation probably burns through ~$10 billion a year for each of them. Apple recently announced the largest share buy-back ever to deal with their problem. At $110 billion, it is larger than the GDP of Bulgaria.

There are of course more radical solutions, notably from Block Inc, which has committed to buying bitcoin with 10% of the cash generated from its bitcoin business. It’s quite elegant in a way because they are risking only the money they make from bitcoin rather than betting the house (as MicroStrategy did).

In addition, they produced a helpful paper on exactly how they plan to execute. They also highlight in that paper the new accounting treatment for bitcoin, which allows gains and losses to be taken through the Profit and Loss account, as is the case with other liquid investments. That change makes life much easier for corporate treasuries around the world to treat bitcoin as they would a government bond or money market fund investment.

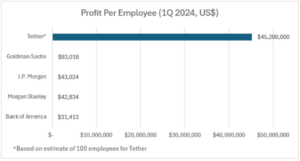

Block is actually small fry though. Tether has been adding bitcoin to its balance sheet each quarter for several years now. They too reported their quarterly profits last week; $4.5 billion for the quarter. A lot of that profit came from the unrealised gains on its bitcoin holdings, but they generated $1 billion on US treasuries alone.

At the risk of repeating a point made a few weeks ago, profit per employee at Tether is absolutely off the charts. They will make billion dollar losses in bear markets, when their bitcoin holdings are marked down, but from a cash perspective it is absolutely pouring through the door at a phenomenal rate.

They continue to invest part of their profits in bitcoin too. They bought 8,888 bitcoin on 31 March taking their total holdings to 75,354 BTC. They have committed to invest 15% of profits in bitcoin each quarter.

So, two listed US companies (Block and MicroStrategy) are adding to corporate treasuries, and the largest stablecoin provider in the world is doing it too. I don’t expect Apple and Amazon to follow suit, at least until they have no other option. Much in the same way as I believe superannuation funds will be forced by their clients to get bitcoin exposure, the major corporations will too.

The surprise to me is not that Block and Tether are buying, it’s that so many of the other corporations are not. Indeed it is true to say and we can say it out loud “the overwhelming majority of people and businesses and governments are not yet buying or holding bitcoin”. I suppose a large part of our thesis is that one day they will.

We’ll revisit this in a few years to see if the Apple buy-back outperformed the bitcoin purchases. Apple stands at $183 per share and 28x earnings today. Let’s see.

Zeitgeist

Long time readers will be familiar with this chart which we first posted in 2019. Some four years on, with the onset of AI (which we did not predict), it feels even more relevant.

Former PayPal President David Marcus picked up the theme this week, opining that bitcoin is going to be the native currency of AI. Why? Simply because the Americans will never accept European money, and the Chinese won’t accept non-Chinese money and the only apolitical money in existence is bitcoin.

I’m not so certain it will be quite that straightforward but what does seem true is that integrating native digital assets into your technical stack is much easier to do when those currencies do not belong to a national government. Open source money is likely to prevail, not just because it is better but because it is orders of magnitude easier to work with.

![]()

Even his terminology is interesting. “The language of value”; I think that’s right. Money is simply an expression of relative values and on the internet, increasingly, the value proposition of bitcoin is well understood, requires little explanation and crucially, does not require permission.

Euro-Trash

I’d like to join the ECB in heartily congratulating Alain on his appointment. Yet another French representative joins the ECB in a senior position! What are the odds?

I wanted to assure myself that Monsieur Busac had been appointed on the basis of his IT skill and experience and not solely on his Frenchness. As the press release reveals, he in fact has a master degree in Statistics and Economics from the Centre d’Études Statistiques and from the Université Louis Pasteur in Strasbourg. He must have tinkered with computers on the side or perhaps he’s a whizz with an abacus.

I suspect his appointment is important because he will be one of the key architects of the ECB’s digital currency. His background at the Banque de France and education in the political schools of France will pretty much ensure that the Digital Euro is absolutely the surveillance coin we all think it will be.

As part of the press release, the ECB updated its manager list too. 19 dense pages of division directors, heads of section, deputy heads of division. I must credit them for their openness in publishing the list but I want to draw a contrast between simplicity and complexity. Bitcoin has no staff and I can download the entire history of every transaction ever and interrogate and verify it in a matter of hours.

Consider too that Alain will be competing with another Frenchman when he takes up his role. One of the most famous developers in Bitcoin, Nicolas Dorier who built btcpayserver, an open source payment solution for merchants. A documentary about the story of btcpayserver was released a few weeks ago, it’s great stuff.

I can tell you without further due diligence that there is no comparison in technical skill, ability and commitment between the two. Dorier works for free, Busac works for Euros +25% towards his final salary pension (a privilege almost nobody else in Europe enjoys).

There will only be one winner.