As a new fund manager (not yet four years old), it is a learning curve. Perhaps the most surprising thing we have encountered across the industry is the amount of time that goes into number crunching and comparison to benchmarks and “consensus views”.

Consensus seems to be an important thing that people look for and take comfort in. I still do not know why. What is the point being a fund manager and looking for consensus?

I take pride in our rather different approach. We do not have a complicated strategy and we do not seek consensus. I can tell you our strategy in one sentence.

As to consensus views, surely if you wait for consensus then the boat has left the harbour. It is not possible to win via consensus, simply by definition.

To be first, you have to go first (and risk being last) and in doing so there will be no consensus.

Your memory is bad

As a fund, we were delighted:

There is now great excitement at this potential taper. I think it would be fair to say that our memories are extremely poor though. Recall in 2008 at the launch of quantitative easing that the policy was ‘temporary’. Over a decade later, we are now ruminating on whether there will be reduced buying.

To be clear, he isn’t even suggesting that QE will stop, there just might be less of it. The idea that it will ever be removed seems like a distant fantasy and it surely must be, because who on earth would buy US debt unless they knew they could easily flog it to the Federal Reserve if things got sticky?

You will recognise some of the language below in an extract taken from a Fed QE announcement in 2010. “Temporary”; “transitory in nature”. Back then they were talking about their bond purchases; now that same language is used about inflation.

The most important thing about this year’s Jackson Hole is that QE is never going away. In the language of the Federal Reserve, it is “temporary and transitory in nature” i.e. permanent.

IMF

“privately issued cryptoassets like bitcoin……”

Bitcoin is not privately issued. That is a reference to the seigniorage rights that every national currency enjoys. National governments can (and do) print more money whenever they wish. That cannot happen with Bitcoin. Indeed, there is nothing more public than its code, its issuance schedule, or its ledger. There is no private person deciding what happens, no CEO, no team or any people at all. The network decides, users and their bitcoin nodes enforce the rules combined with game theory and cryptography. Together that protects the integrity of the currency.

The IMF simply cannot get their head around the fact that some computer code released into the wild has gained a massive network effect which grows every day. It has a security model that is totally unassailable. No government could ever create equivalent code because they would seek to control it from day one, immediately destroying any network effect it might hope to create.

The IMF would love to operate a pan-national currency. It even has its own currency, known as Special Drawing Rights, launched in 1969. SDR’s are made up as follows:

Originally SDRs were defined as 0.888671 grams of fine gold but they scrapped that in 1973 after the United States defaulted on the gold standard. One SDR would be worth about $50 in today’s money as originally conceived, instead it is worth about $1.40. Roughly a 97% loss of value since 1973.

The IMF had their chance to design an international currency that protected wealth. They had all the best economists in the world, they had the largest budget too and they came up with SDRs. They failed, totally.

One cryptographer with a budget of zero and an ego of zero came up with something vastly superior.

No wonder they hate it.

Crypto-Voices

The team at crypto-voices produced their quarterly report this week. They focus on comparing the core metrics of various fiat currencies around the world.

The most eye-catching chart was the one below. It shows the gross value of base currency globally (so the M1 definition in most countries; notes and coins + bank accounts). Dark purple is notes and coins, light purple is money in bank accounts.

Since 2008, there has been a four-fold increase in the amount of money sloshing around. Most tellingly, the bulk of it is the computer printed version of money in bank accounts, not physical notes and coins. Some of that is the move to digital payments and a lot of it is simply government the impact of monetary policy interventions.

It really boils down to this. Take 2008 as a starter; say your home has increased by 3x since then and the money supply has increased by 4x. Are you richer? Arguably, only if you borrowed the money. The debt you used has been monetised away to the point you don’t really think about it anymore.

It is perfectly possible that the property insanity we see in Australia is a simple function of people wanting to short the currency in this way. The only way they can do it is by overpaying for a property, but that overpayment might be more than compensated for by the short position.

You might think that people don’t think that way and certainly most people don’t think that a mortgage is a short position on their national currency. People do understand when they are being swindled though; they inherently know what is valuable and what is not over the long term and generally they act accordingly.

The tidal wave of retail debt looks insane, but is it? The collective mind has a way of knowing what an individual mind cannot. If everyone borrows lots of money together, will the government bankrupt them? No. You cannot win elections that way.

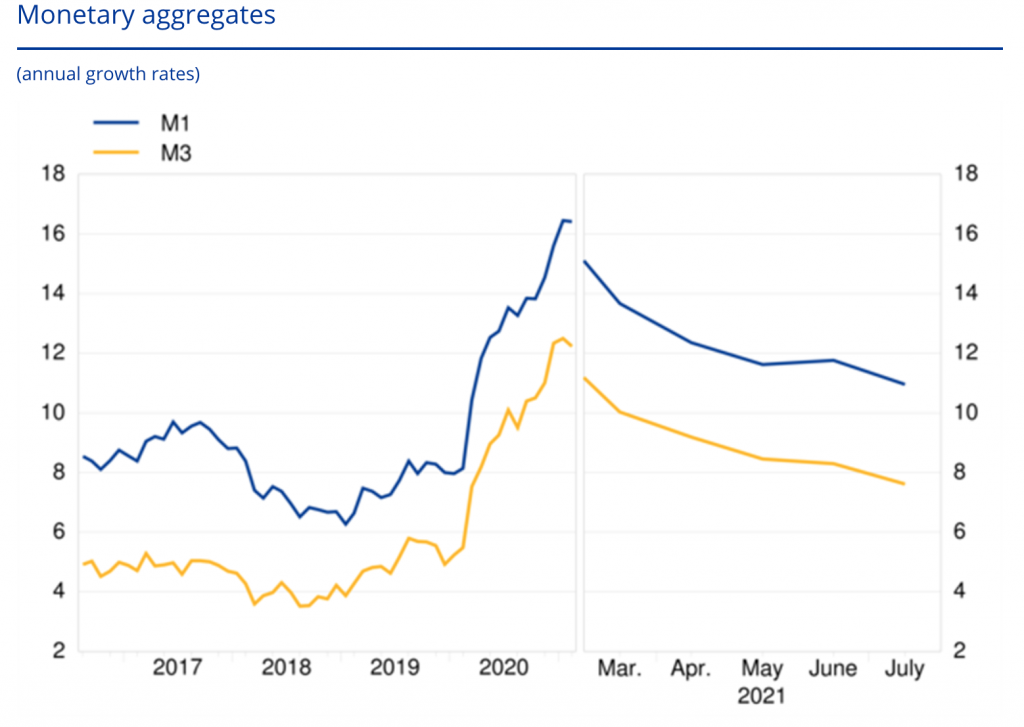

Euro-Trash

Great news from our friends at the ECB this week reporting that the amount of money in circulation is now increasing at only 11% per annum down from 16% last year.

It’s exciting because now it will take seven years instead of five for the Euro to lose half its value. Don’t forget, you also get to deduct about 0.5% annually because interest rates are negative, so it might happen more quickly. Don’t blink.

They were so pleased, they even provided a chart laying out the reduced pace of their total value destruction.