Buffets

The talk is that self serving buffets are now a thing of the past, simply they don’t work in this new world order. I was prompted to find out why, here’s a possible explanation.

Not only that, Buffett has managed to underperform the S&P 500 for the quite some time. Still, this is not to criticise an amazing investor but simply to make an observation. The world is changing, Buffet was late to technology, he rejected Microsoft, he was very late to add Amazon and he has had this to say about bitcoin:

“Bitcoin is an asset that creates nothing”

“Probably rat poison squared” (amusing given he owns Coca Cola)

“Has no unique value at all”

It’s extremely hard to outperform the market, almost no investment manager can do it, including Warren Buffett these days. Ultimately, you have to do something different, be somewhere that other people are not willing to go because you have a different perspective on the risk versus reward and you believe you understand something that they do not.We have the strong feeling that our funds add something to portfolios that they do not currently have. Holding bitcoin gives you early access to an asset that most other people do not wish to touch at this stage. Very few people actually understand how it works, why it is resilient, why it is meaningful. Indeed our job as a fund manager is to do that for you.

The man who sells the real rat poison isn’t outperforming hard assets any longer. Times are changing, the era of the Buffet(t) is coming to an end.

“Holding bitcoin is like owning the fastest horse in the impending inflationary race, if I am forced to forecast, my bet is it will be bitcoin.”

He went on to explain. Governments around the world insist on 2% inflation as a minimum, as we know that means any cash you hold erodes by that amount every year, compounding. That situation is likely to get much worse thanks to the amount of stimulus and money printing we now see.

“The depth and magnitude of the economic drop-off took modern monetary theory or the direct monetization of massive fiscal spending from the theoretical to practice without any debate. It has happened globally with such speed that even a market veteran like myself was left speechless. Just since February, a global total of $3.9 trillion (6.6% of global GDP) has been magically created through quantitative easing. We are witnessing the Great Monetary Inflation (GMI) an unprecedented expansion of every form of money unlike anything the developed world has ever seen.

The thesis is simple. Buy something scarce. The bitcoin invention is “provable digital scarcity”. It really is no more difficult that that.

JobKeeper

In Australia, the JobKeeper allowance pays $3,000 per month to employers for each member of staff they keep in employment, subject to a number of conditions. It is hugely expensive for Australia, roughly $150 billion for its scheduled 6 month duration. That is somewhere close to 10% of GDP before any other costs of coronavirus are factored in.

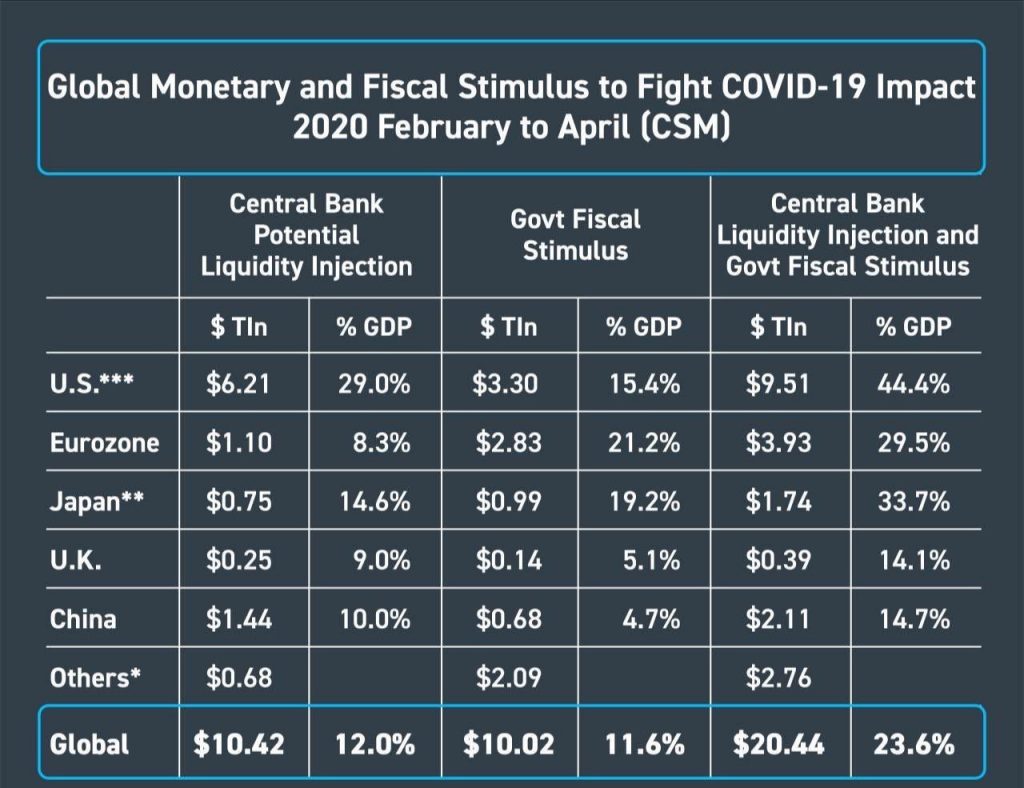

It seems relevant since in the table above, this huge sum does not register. It sits in the column “Others”. A note of caution on the table, the US Liquidity Injection includes $3 trillion that hasn’t yet happened but has been promised (by the time you read this though, it will likely be more).

The scale of the global stimulus is simply enormous, the United States will have unleashed over 40% of its GDP in liquidity before the end of June. The numbers have become so large that barely anyone notices, would it matter if the US lobbed in another $5 trillion in liquidity? Probably not.

As you sit back and watch this happen in the US, Europe, Japan and Asia you start to think that this is crazy. I have to say though, international policy makers are playing an absolute blinder here. They were in an enormously tight spot, escalating debt, falling tax base, how on earth do you get out of that? The answer is the same as it has always been, you simply print money. You monetise the debt and if you can find a distraction to hide behind, like a war or a virus, even better. Throughout history that has always been the answer.

If we go back 2000 years, we can find a very good example of how to do it. Back then, the Emperor Nero was on the chair in Rome. He debased the currency in AD60 by reducing the silver content of the coin, meaning more coins, which briefly made everyone happy (it ended badly). However he used an admirable distraction. At the commencement of his reign he had minted coins with his mothers face on the reverse side along with his own. One year before debasement began, he murdered her, although by then her face had been removed from the coins as well. So much more panache in Roman times. No need to wait for the Federal Reserve minutes, simply observe which face on a coin has been murdered as your precursor to debasement. Dull Australian politics would benefit greatly from this kind of uplift, “Treasurer Frydenburg announces JobKeeper to stay having murdered his own mother earlier in the day”

Nero and his mum in happier times

Right before your very eyes this debasement is happening. As sure as eggs are eggs, the crowd cheers from the stand. Wait until later in the year when the supplementary payments run out, there will be clarion calls for them to stay, the government will resist, they will make noise and then, they will relent. More money will be printed.

The great thing about this current situation is that we know with some confidence how the biggest economic actors in the world will now behave. Their goal will be for solid inflation, somewhere from 0-8%, that would be sufficient to get nominal salaries rising and debt burdens falling.

The signs have been there for a while. Countries have been issuing longer and longer term debt, Austrian 100 year bonds, US 20 year bonds. There is a tidal wave of issuance at low rates. It is actually incredibly sensible for the issuers and incredibly bad for us. They know what is coming.

Who is dumb then? Who is crazy? Is it the institution that issues huge amounts of money and debt at record low rates for record long maturities, or is it the person that takes the money?

Look at that chart. The joke is on us.

Risk

Many traditional investment analysts believe that current stock valuations, while high by historic standards are supported by the low interest rates. Fundamentally, in valuing a stock, one simply discounts the future cash flows of the business. The lower that discount rate the higher the stock value. Consequently then, with rates as low as they are is it a surprise that equity prices are where they are?

On the face of it, that analysis is absolutely true. But:

1. The interest rate is surely artificially low. We know this is true because in all major economies around the world we have central banks telling us that they are buying bonds to keep interest rates low. High bond price, low yield, low interest rate.

If the interest rate is artificial. Isn’t the stock price also artificial?

2. There is now a very real chance that interest rates go negative. Any interest rate at or below zero implies a stock price of infinity. So, if the analysts are correct they should be buying an unlimited amount of stocks, but they are not.

It is becoming really difficult to discern where value actually sits because the measurement metric, the dollar, is now so distorted.

I cannot emphasise enough the importance of a stable unit of measurement. Value in terms of something that does not move or that moves in a predictable way. We might well find that stock prices double in the next five years but even then, stock holders may end up poorer in relative terms.

The question is starting to become, “will this assets/stock/commodity be relatively more or less desirable in five years”. Nominal dollar values are not as instructive as they once were. Will it go up, is no longer the question. The question is, will it go up enough?

Will $1000 of bitcoin be worth more than $1000 in five years?

Bitcoin is risky. I need compensation, fine. Let us say 25% per year. That implies, the $1000 will be worth $3,051 in five years. 3x. That implies a price of US$30,000 and a market cap of $600 billion.

Will Apple shares be $900 in 2025? Market cap would be $4 trillion

How about Google it would be $6,865 per share? Market cap would be $2.8 trillion.

To me, the chances of bitcoin being $600 billion + in 2025 are much higher than Apple at $4 trillion. It’s just an example of course, but the risk reward profile of bitcoin looks appetising at the moment.

Bitcoin Mining

In a post-halving world. Bitcoin mining is a lot less profitable that it was. Miner income has effectively dropped by half since last Tuesday. In better news for miners though, fees have more than trebled on average. Ultimately when the block rewards run out, bitcoin’s mining model will be funded by fees.

For the next 4 years, we might expect bitcoin fees to be somewhere from 10-20% of the block reward and that should increase with each halving until fees make up the majority of miner income.

Opinions differ on fees, I reside in the camp that fees need to be viable and high. 50 cents for a transaction that will reside on hundreds of thousands of computers around the world, always allowing you to prove it is yours, seems like a good deal to me. We need a sustainable fee model and it’s happening.