Web 3.0

A crisis?

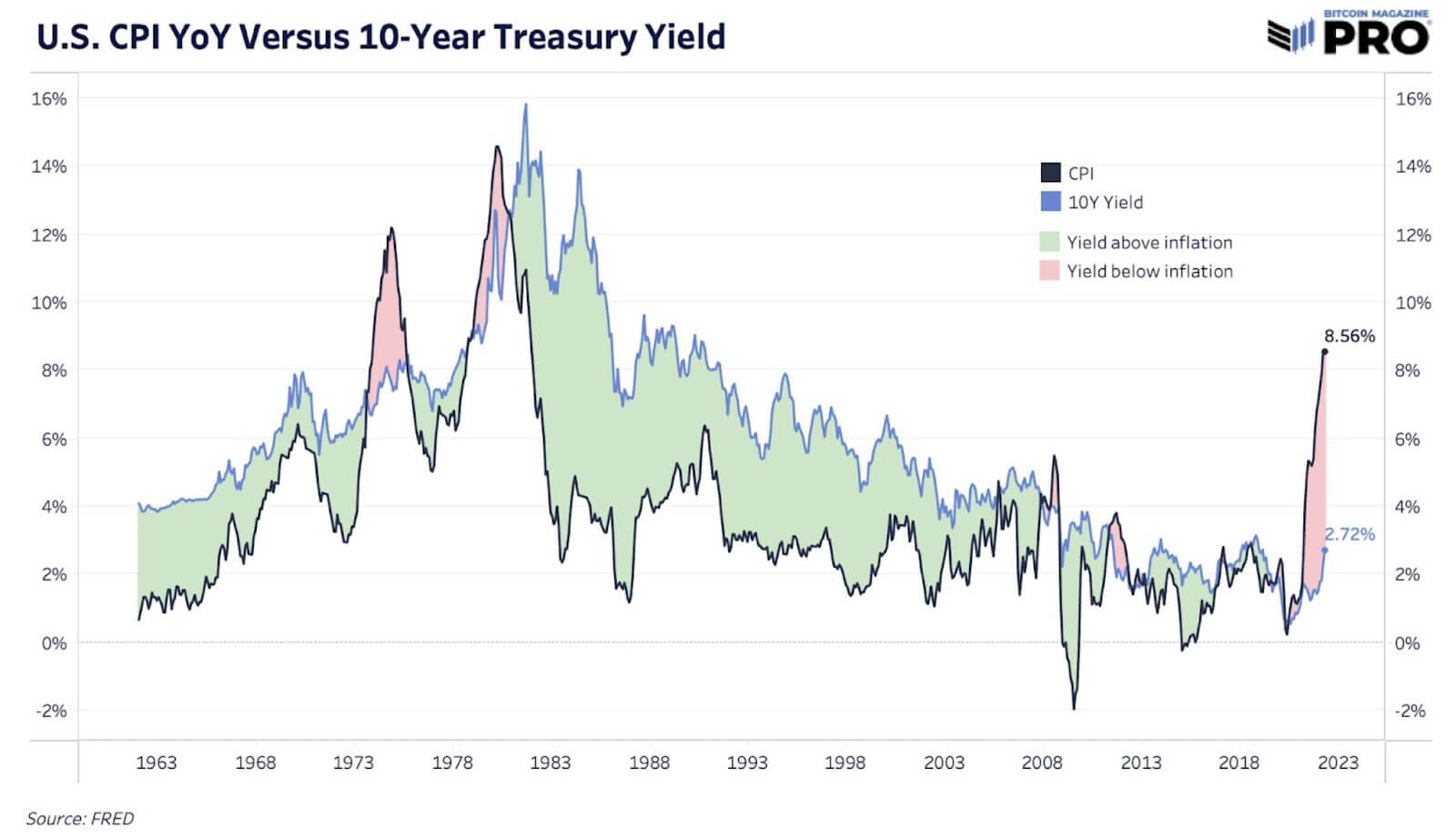

At no point in the last 60 years have bonds yielded such a negative real return. Perhaps more critical now is the fact that government borrowing has never been at such consistently high levels. So while bonds are an awful investment, never have there been more of them on sale.

It’s a situation that cannot continue forever and I recommend this excellent podcast featuring financial historian Russell Napier in which he predicts what will happen. In essence, the government has lots of bonds to sell, and people will be forced to buy them under a system he terms ‘financial repression’. Regulations are introduced which force pension funds, mutual funds and other tightly regulated asset pools to allocate to bonds. It will be done in the name of risk and it will be at the expense of other asset classes. One way he recommends to avoid this happening is to own assets outside of the regulatory domain, the less financialised the better.

For the avoidance of doubt, he does not mention digital assets at all, simply that you might consider those assets which you can own and control outright beyond the reach of the government. For example, in Australia, self managed super funds would appear safer from this kind of forced allocation than professionally managed regulated funds.

Aside from anything else though, when the largest asset market in the world is returning -6% (if you believe the published CPI), it is not a good sign. As long as people are willing to sign up and lose money though, everything is fine. Many superannuation funds around the world do not have a choice, they must simply gobble this garbage up but at some point an American bond auction is going to fail. Then the Federal Reserve will step up again and all hell will break loose.

Bitcoin ETF (nearly)

Australia’s first listed bitcoin product looks set to go live next week. Unfortunately, it will once again not offer pure bitcoin exposure and will invest via the Canadian Purpose Bitcoin ETF. Essentially, a fund of funds with multi-layered fees. Still, there are expectations that the fund could reach $1 billion in AUM quickly.

The better news is that the pure-play ETF is very close. Allowing an ETF in Australia via a Canadian product and then denying a pure Australian-based ETF would seem very strange indeed, so we may in fact only be weeks away from the pure product.

The road to legitimisation has been long but listed ETF products are the pinnacle of regulatory difficulty. That bitcoin has scaled these heights is quite something.

As you can see, since it launched in 2009 it has been top of the pile. Other digital assets started to try and take the crown from around 2013 but they have come and gone and will likely continue to. I expect bitcoin to be on top for a very long time, not just of digital assets, but commodities in general.

Liquidity

Our number one criteria for investment as a fund is liquidity. Specifically, is there any?

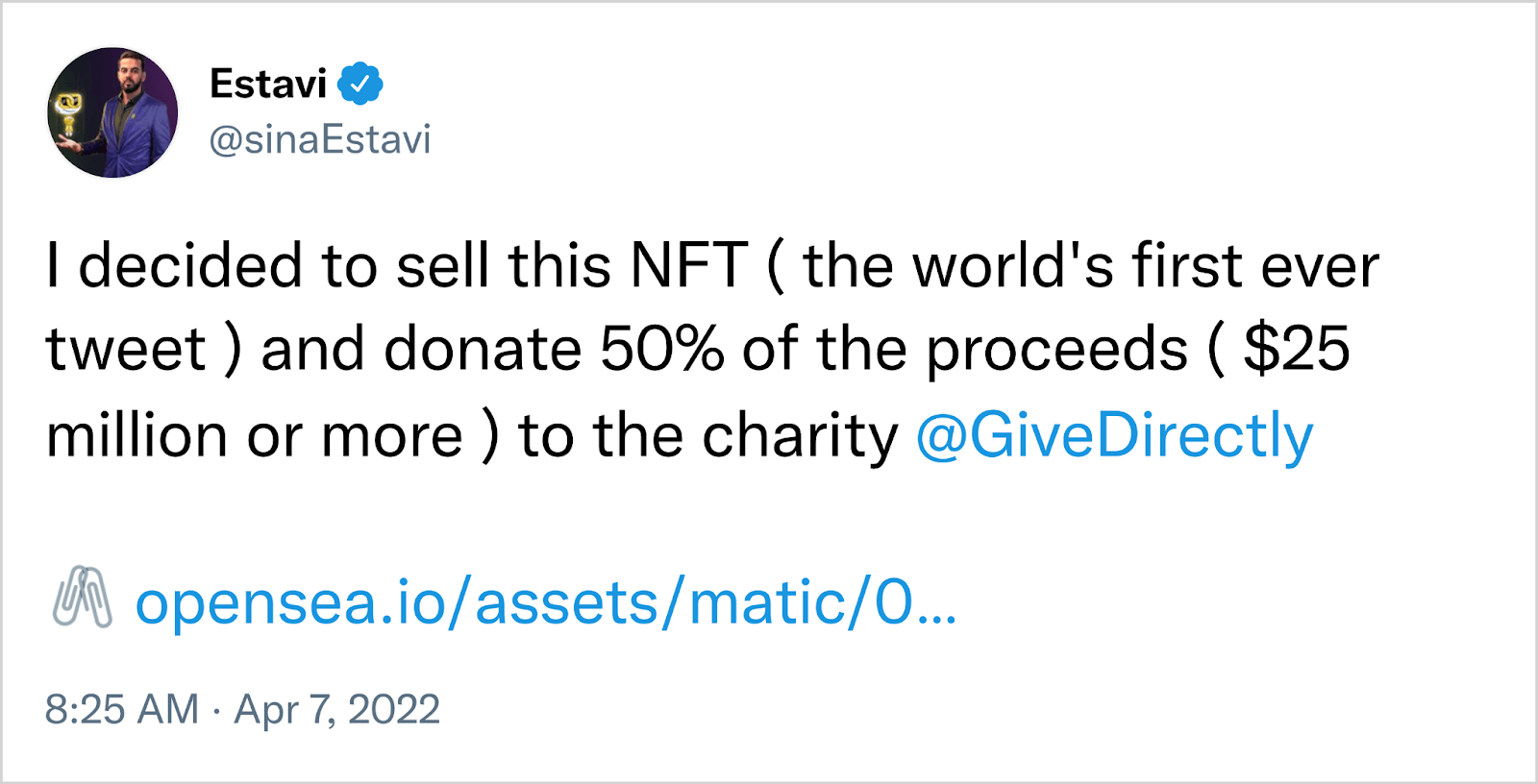

A terrific example was provided this week by the owner of the infamous Jack Dorsey NFT tweet. Sina Estavi bought the NFT last year for $2.4m and promised to donate half the proceeds of his forecast $25 million sale to charity.

Unfortunately for Mr Estavi, there were very few bidders. The top bid at the expiry time was $270, although later someone offered $14,000 which would have secured a 99%+ loss in either case.

In the end, he didn’t sell. I suspect the exercise has made him and his company more famous and he will forever be the man who bought the Dorsey tweet. One could make quite a solid argument that this whole experience has been worth well in excess of the $2.4m he paid in marketing exposure alone. Ultimately, he may very well get his money but the point is there has to be liquidity. NFTs are unique, like art. You have to find someone as interested as you are and that is often difficult, particularly in a time of falling NFT prices.

None of this makes NFTs worthless, it simply illustrates a point about assets and liquidity. Some assets are hugely liquid in this sector. Bitcoin for example. Other assets have essentially zero liquidity; which is the very source of their value in the first place and so pricing them is difficult. Last week the tweet was worth $2.4m, this week, $270. Now Mr Estavi has decided he is never selling it, so is it worth infinity?

Euro-trash

The journey into Euro-Oblivion continues. Agent Lagarde released a video this week in which she explains, with real clarity, the plan.

“We are on a journey. And clearly, as I said, we started the monetary policy normalisation back in December, reconfirmed in February, clearly indicated in March and we are restating this determination on the occasion of this monetary policy meeting. We have, as I said, added a few particular attributes to the decision that will be made in June when we have the next projection round, which is when we can take stock and actually assess exactly the timing of the conclusion of our net asset purchases, which will then trigger sometime after the end of net asset purchases, interest rate hikes. So, the journey has begun, it is moving along as predicted. We want to have flexibility, and move gradually and keep all the options open.”

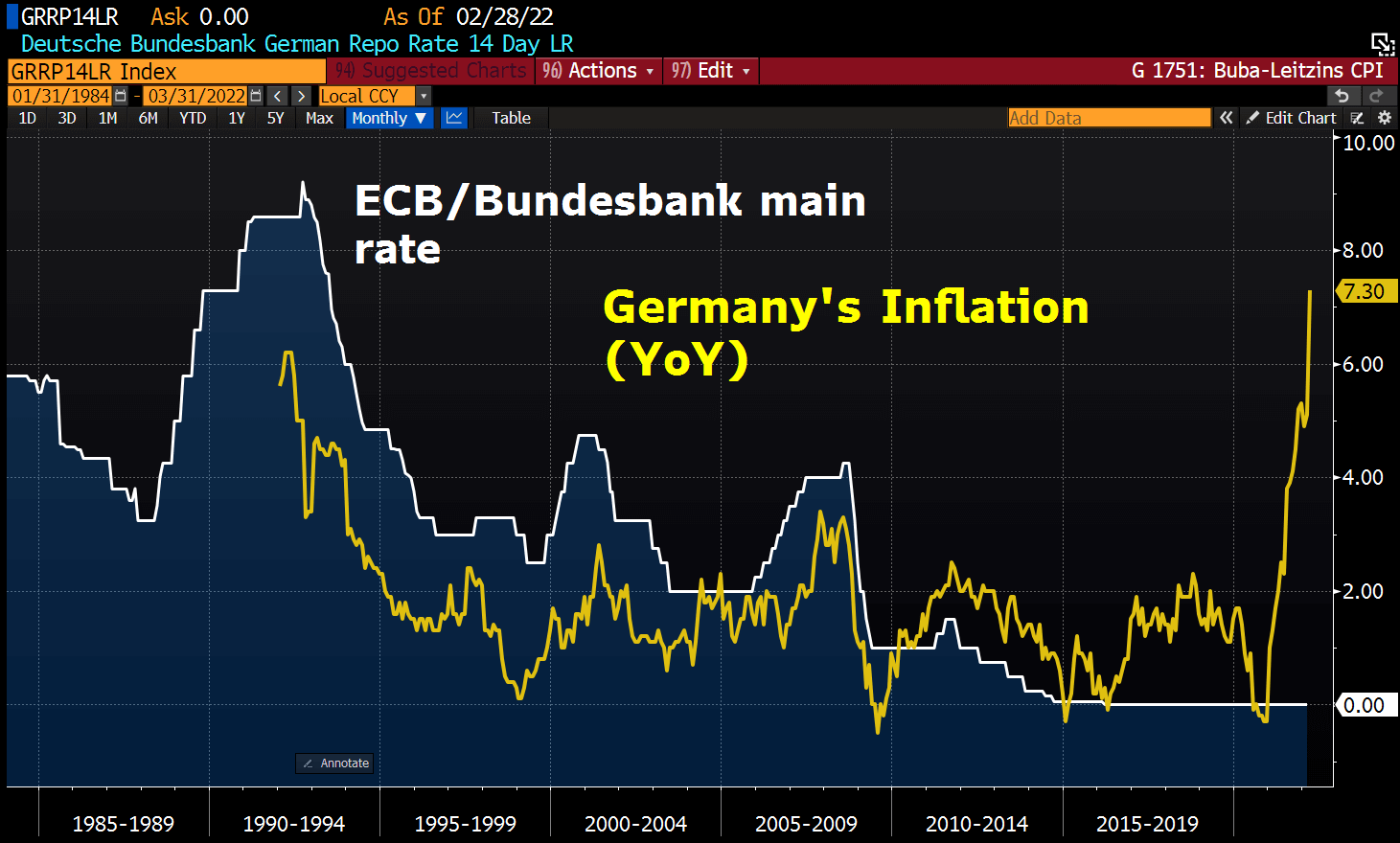

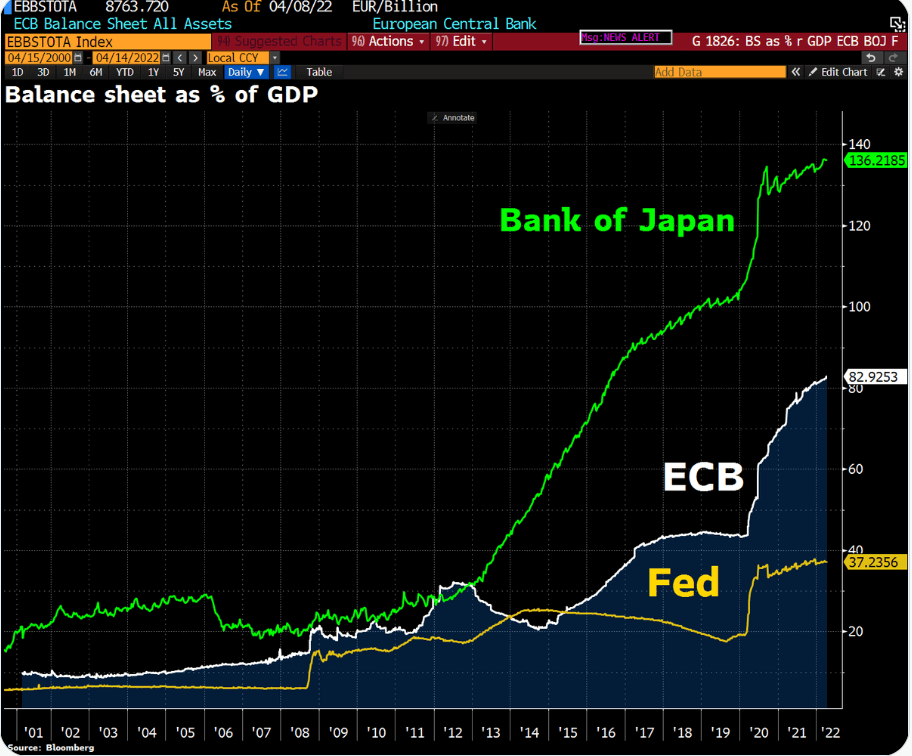

To paraphrase, Lagarde is saying “we have made a decision to make a decision although we do not know when or what the decision will be”. There is always nuance and signal in the language selected by central bankers but this takes things to a new level of ridiculousness. All the while asset purchases continue, no normalisation occurs, the ECB balance sheet is now 83% the size of the Euro-zone GDP and the real interest rate is still profoundly negative.

German inflation is responding and as a result the first country to leave the Euro-zone and re-adopt its own national currency, will not be Greece or Italy. It will be Germany. There’s lots of fun to come yet in Europe, it hasn’t even begun.