Denied

“the proposal did not meet standards designed to prevent fraudulent practices and protect investors”.

Once again, the SEC has denied Grayscale’s application to convert their bitcoin fund to an ETF. There were over 11,000 letters from investors and academics in support of the application this time, which is far more than anything seen before but it made no difference. 86 pages of SEC legalese said no. The length and complexity of the response suggests it was not a straightforward decision. There are 268 footnotes in the document and we can take some real comfort from the tremendous pain that must have been endured by the SEC legal team. With more to come, as we will see.

The main issue is how on earth can you have a futures ETF which, whatever the circumstances, will underperform a spot ETF, and not approve the spot product? It does not make sense, which is why within an hour of the decision Grayscale launched legal action to sue the SEC.

Suing the SEC is not normally considered sensible in the corporate world. Grayscale now has nothing to lose and has signed up some of the best lawyers in America to make their case, including the former Solicitor General.

Recall that the first bitcoin ETF application in the US was in 2013, with the bitcoin price about $13 at the start of that year. It went to $250 and then fell 50%, sound familiar?

Still, volatility is not the reason the product is denied by the SEC, it would actually be a better explanation to say we cannot approve an ETF for an asset as volatile as this. Unfortunately, that boat sailed when the futures ETF was approved.

The CEO of Grayscale estimated this morning that the lawsuit would be decided within a year. Is it possible the SEC hopes they lose the case? The decision to approve the product is then effectively made by the court and taken out of their hands somewhat.

Perhaps Grayscale made a strategic error by pre-announcing they would litigate if the product was denied. If you are a government entity the easiest thing in the world to do is let someone else decide.

Strikes

Oh dear. Is he a former economist because they sacked him? Here’s his rationale:

Adding in the annual rise in the superannuation guarantee, bonuses and promotions, people’s pay is rising faster than indicated by the 2.4 per cent wage price index.

The super guarantee is an extra 0.5% per year. Bonuses do fluctuate but on average they don’t grow more than wages. So let’s be generous and include the extra super (which nobody can spend) and say wages are growing at 2.9%. That’s still a long way behind the 5.1% inflation.

Teachers, rail workers and nurses are all on strike because they are calling fraud on these government numbers and the nonsense spewed by paid shills.

For most people, prices are rising at something like 10% per year, because most money is spent on housing and food. People feel poorer not because of some temporary wobble but because they are indeed poorer.

The reality is inflation is a tax, generally a well managed one, which people don’t notice until something goes wrong. It is also a hugely regressive tax since the increases in food, power and housing prices are felt most by people with least money.

Appliance of science

The general perception appears to be that the cure for high inflation is higher interest rates. This strategy works by causing people to spend more on debt repayments than they can in the general economy. It is a policy of ‘demand destruction’.

In the short term it works. Longer term, the interest rate is only a mechanism through which capital is allocated – it bears no relation to inflation.

The real cure for inflation is simple: do more with less through the application of technology. Either less labour, or less capital but get the same output.

There are many examples but a good one which we are all familiar with is the smartphone. Whatever its inherent evils, it was a massive step forward in efficiency. You could likely administer 90% of your economic interactions now through your smartphone. It was a massive inflation crusher. Fewer staff and supporting infrastructure are required in almost every economic function.

A more oblique example from history was the invention of air conditioning. It didn’t improve efficiency directly but conditions in factories were so much better in air conditioned locations, workers were actually prepared to either work longer hours or take a pay cut to work in the cooler location. It was a massive upgrade to output. Again, somebody made things better and it generally lowered input costs and inflation.

There are examples of course of things that are getting worse. Dishwashers for example are not as good as they were five years ago. Newer machines attempt to clean dishes using a teaspoonful of water and a solar panel. The American Institute of Economic Research published an article on exactly this issue.

Although nobody talks about it, the way to fight inflation (and the only way) is to get better at doing things. There is no magical cure in interest rates, only needless pain distributed by people that believe they can micromanage an infinitely complex thing like an economy.

Most improvements in technology will use more energy if they are allowed to. Air conditioning was a huge step forward for human comfort and factory production but uses a tremendous amount of power. Similarly, smartphones and their supporting infrastructure are right up there in the power consumption stakes.

Getting better at things is the answer. Generally, those improvements will require more power. Improving a person’s life generally means less power output from them and more power output from the technology they are using.

Either we command the infinite energy in the universe to our will, or we don’t. There isn’t really an inbetween.

Better but worse

For the first time since 2013, Western Australia had its state bonds upgraded to AAA. It is an impressive feat. Consider that sovereign bonds in the UK are rated only AA and California, an economy 10 times the size of Western Australian, holds AA-.

There is an interesting dynamic here. WA has been upgraded thanks to a huge increase in commodity price inflation. The raw metrics of the investment look less than compelling though.

WA bonds yield 3.9%. Inflation in Australia is 5.1%.

So thanks to inflation these bonds are now an excellent investment guaranteeing you a loss of only 1.2% of your purchasing power every year.

AAA? If you say so.

Euro-Trash

Are we too hard on Lagarde? We can lay out some compelling factors that suggest we are not.

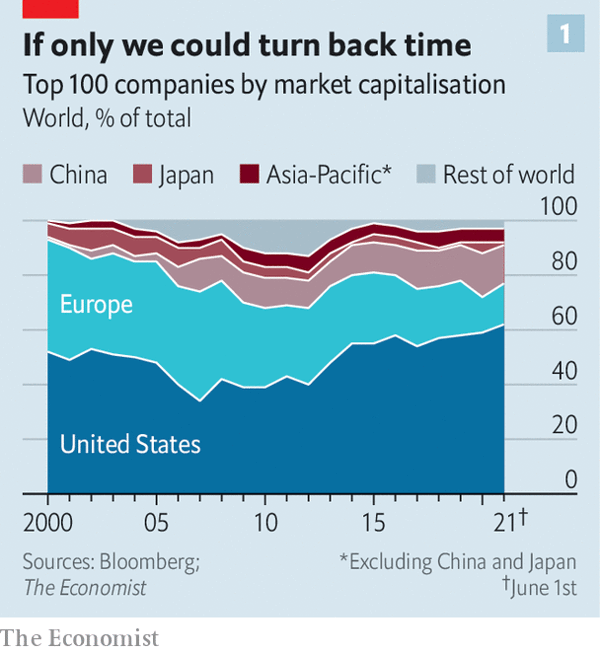

In terms of the market capitalisation of their largest companies, Europe has gone from a serious global player at the time the Euro launched to an also-ran. Dominated by the USA and overtaken by China. There is almost zero innovation in Europe these days.

Of 150 companies globally that are worth more than $100 billion, 43 of those companies were set up from scratch in the last 50 years. Only one is from Europe.

Why? Well Europe is mired in politics and political projects. Small groups of unelected persons make decisions that impact everyone, and despite being well-meaning, they are generally poor ones. The pursuit of the Euro as a mechanism to bind European countries together is prioritised at all costs. Those costs are enormous in terms of potential value destroyed. The chart above proves it. Europe’s declining population proves it.

The European Parliament has been aware of the issue for a long time. They laid it out in gory detail in 2008 here. Then they did nothing about it .

Nobody ever says “I have a great idea and I’m going to Europe to start the company”. Globally, entrepreneurs head for America first and Asia next.

As summer approaches in Europe it is likely their latest crisis will ease. While they scramble around for gas and prepare to start burning coal again they will be missing the bigger existential issue they face.