Did Amazon grow?

An honest question, if Amazon revenue growth was +7% in the last quarter and inflation in the US was 8%; did Amazon grow at all? In real terms, surely no.

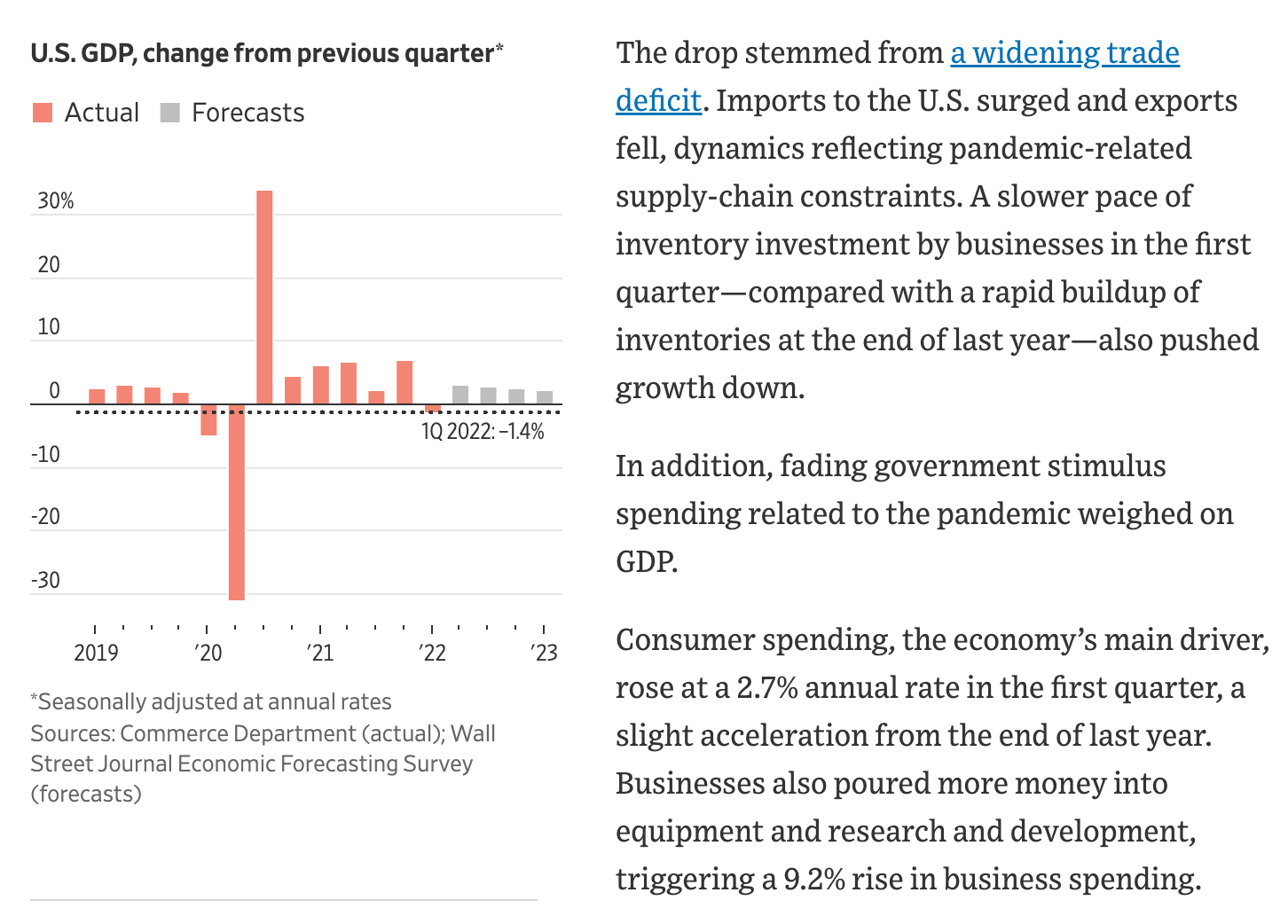

Consider then that the US economy actually shrank by 1% in Q1 this year. It is rather odd that this was not covered in more detail by most of the financial press, dismissed as a statistical anomaly because of something to do with the trade balance. Maybe, but maybe the world’s largest economy contracted in real terms by something over 5% in a quarter when the taps are on and everyone is at pre-covid levels of activity.

The detailed report was buried on page 900 of the Wall Street journal and since then there has been very little discussion about it. Talk about burying bad news.

Now US interest rates have risen 50bps too, so consumers will have something else eating their purchasing power to accompany 8% inflation.

Perhaps a more reasonable assessment is that every single vector is moving against American workers and the marginal dollar for spending just isn’t there. No surprise that Amazon and US GDP are moving in sync here. The US consumer might just be out of bullets.

Halfway there

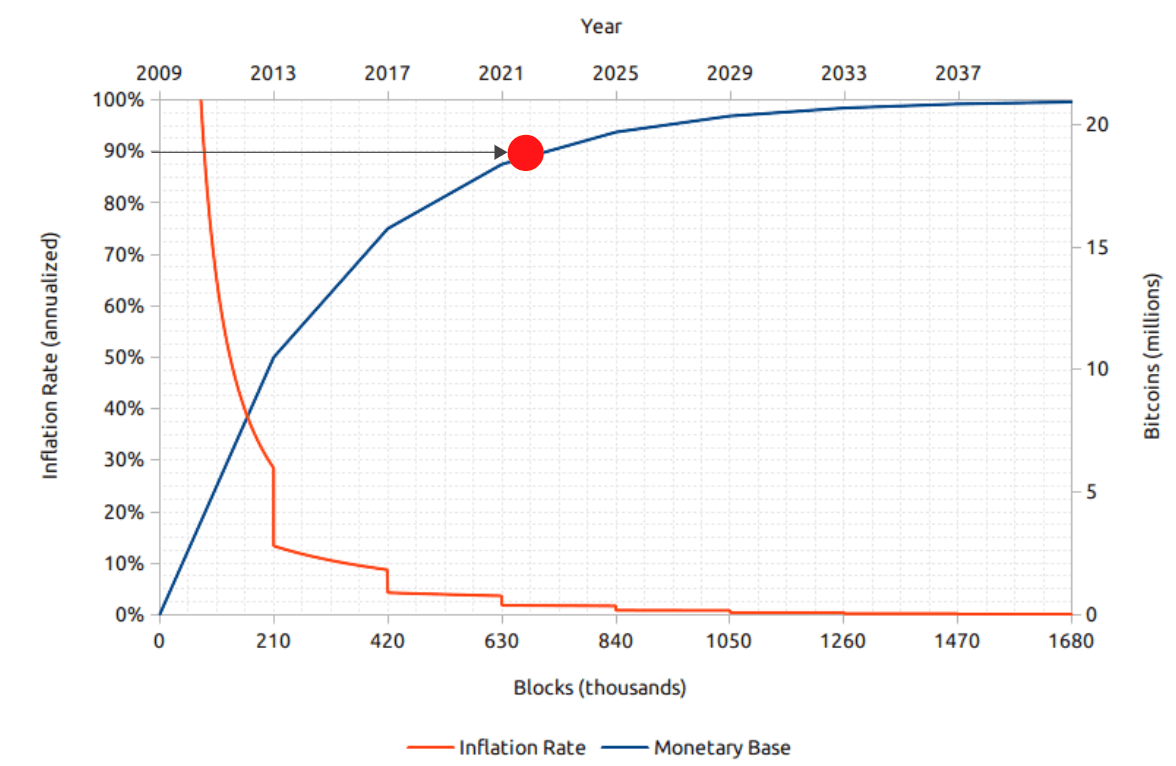

We are now officially halfway to the next bitcoin halving. In two years, issuance will drop again to 450 bitcoins per day from 900 currently. That takes the annual inflation rate of bitcoin to 0.8%.

I drew attention to this supply curve effect in our webinar this week for investors.

19 million of the 21 million bitcoins are now on issue and the rate of issuance is falling fast.

When you consider we don’t have an ETF yet in most countries and almost no superannuation/401k money is invested in the sector, that leaves an awful lot of money on the sidelines that will compete in a very tight supply space.

Bitcoin’s supply cannot react to demand, only price can. True of almost nothing else in the world. The two year count starts now, on the last few occasions we started to see major movements 18 months out.

Goldman Loans

Goldman offered their first bitcoin backed loan recently. I suspect this will become a very vanilla product quite shortly because of the excellent collateral digital assets represent. Every other asset has some sort of risk of double pledging, it is very hard for a lender to be absolutely sure that a given asset is not already mortgaged. Not so with a digital asset, because ownership verification is simple and absolute. If I pledge bitcoin to a bank as collateral I can only do that once, cryptography makes sure of that. It is the same for all digital assets.

Goldman are rather late to the party though, DeFi startup Arcade has been lending against NFT’s for a while now with over $25m of NFT collateral backing loans. The LTV’s are predictably low because of price volatility but the highly prized NFTs like the Bored Apes are holding up well as collateral.

The lending market in Bitcoin is much more developed. Billions of dollars are pledged into DeFi as collateral and at low LTV ratios. One can now borrow for as little as 1% per annum. That makes sense too because the collateral is so good that making a risk assessment (and hedging it) is easy for the lender. It doesn’t matter what other liabilities the borrower has; those additional claims cannot access the bitcoin once the private keys are shared with the lender.

Expect this market to develop very quickly. The penny is finally beginning to drop about the purity of collateral that bitcoin provides. It is better than almost anything else and over the next decade, it will prove it.

Japan

Remember Yield Curve Control? Australia was one of the few countries to actually try it during Covid. In the end, the Reserve Bank got taught a lesson by the bond market when they realised they would end up owning an entire series of a particular bond. Sensibly, with egg on their faces, they relented.

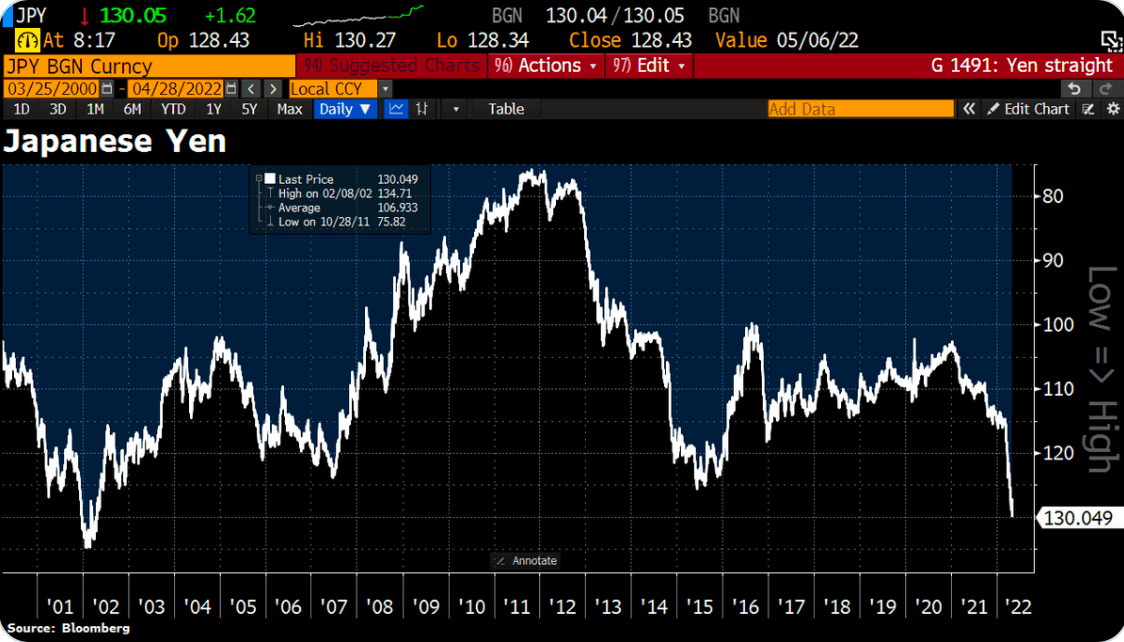

In Japan, they have no such qualms. BOJ governor, Haruhiko Kuroda, recently said he was more than happy to buy every single bond in an attempt to make YCC work. Unabashedly describing it as ‘unlimited bond-buying’.

In that case it absolutely will “work” but the market will likely punish you in another way, and it did. The Yen dropped to its lowest level in over 20 years against the dollar. In some ways, Japan has no other choice, a shrinking population means they do not have new buyers for their government securities. The only choice is to monetise the currency and it’s been downhill for the Yen against the USD ever since.

YCC is coming to Europe too. America’s demographic crisis is not quite as severe but the competitive currency devaluations are likely to continue across the world. The one thing sustaining the US dollar right now is the weakness of almost everything else.

When I hear pronouncements like the one from Mr Kuroda this week, I think only one thing: Buy bitcoin.

Euro-trash

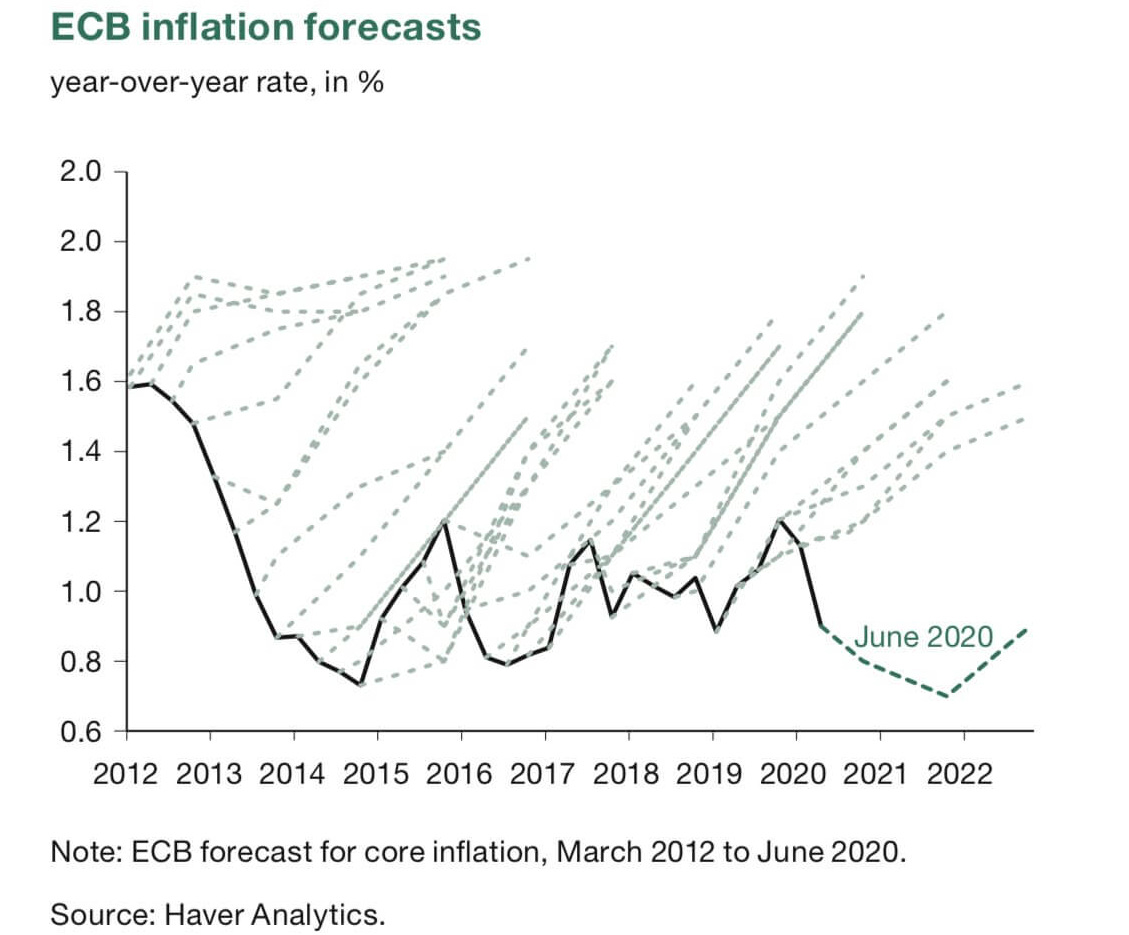

It’s ok to be wrong. However, when one is consistently wrong on the same theme only to make a 180 degree turn at exactly the wrong moment resulting in you carrying on being wrong, then people might doubt your judgement. Please welcome the European Central Bank.

For 10 straight years and 40 individual predictions, the ECB has been right just once, in 2014 and they were right for about 6 months, a 97.5% error rate. More importantly though, they were totally wrong on trend for a whole decade. They never predicted inflation would go down, until 2020 when they had the money taps on like never before, at that point their forecast was inflation to fall below 1% until 2023. Inflation immediately went to 8%, which is completely off the chart.

When you are wrong, you apologise and move on. When you are this profoundly wrong and you have armies of PhD Economists at your disposal spending other people’s money, what do you do? Unbelievably, you produce a report explaining your wrongness. The report is a work of art; it can be enjoyed in full here.

Part of the explanation can be found on page 86:

The real explanation is that the price mechanism is infinitely complex, incorporating the relative wants and desires of billions of people around the world which change all the time and interact with each other. You can’t model it because each input has a complexity level of about 7 billion to the power of 7 billion and changes every second of the day. Even worse is to try and interfere or manage that price mechanism but that is what the ECB do all day long; with approximately zero success.