Narrative shift

If you wanted a looking glass into future White House press conferences, this was one.

That was released late last week ahead of GDP numbers. Sure enough, last night, the US printed its second quarter of negative GDP. For as long as anyone can remember, that has been the definition of recession. It was useful too because there is no room for weaseling.

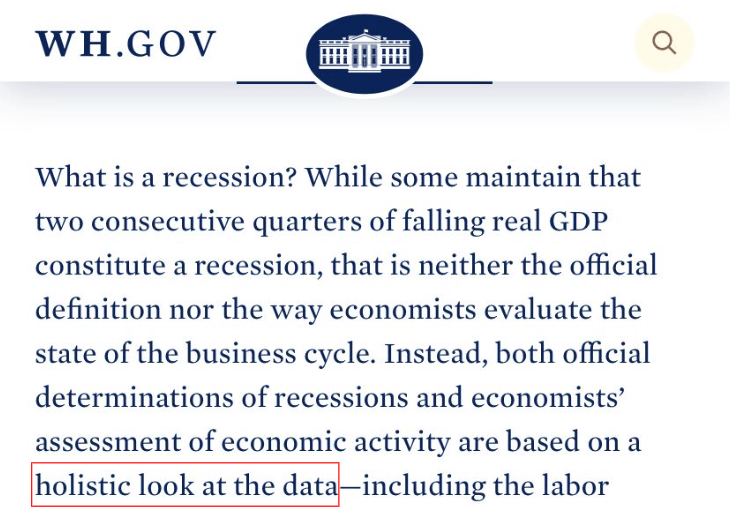

Not anymore. Now the definition is “holistic”.

Would you believe it? Based on the holistic data, there is no recession in the US. This theme was taken up by Madame Transitory herself, Secretary Janet Yellen. Appearing on NBC news she came out to bat like the champion she is. Watch the video here for maximum pain.

TODD: “If the technical definition is two quarters of contraction, you’re saying that’s not a recession?”

YELLEN: “That’s not the technical definition. There is an organization called the National Bureau of Economic Research that looks at a broad range of data in deciding whether or not there is a recession. And most of the data that they look at right now continues to be strong. I would be amazed if they would declare this period to be a recession, even if it happens to have two quarters of negative growth.

Are we clear on that? Even if it meets the definition of recession. It’s not. Now get back to work.

RBA review

Today I announce the first wide‑ranging review of the Reserve Bank of Australia since the current monetary policy arrangements were instituted in the 1990s.

Yikes. This one took me by surprise because the RBA, despite some recent disasters, really isn’t that bad. Let’s face it, if you are an economic steward and blessed with 30 years of growth, perhaps you’re getting more things right than wrong.

Even if all the good things that happened were nothing to do with the RBA, at least they didn’t stand in the way through needless intervention. They will be blamed for house prices (up or down) and they did preside over humiliation with their yield curve control last year, but overall 8/10. It’s all academic now though and the review has been announced.

The government’s terms of reference point to a political objective including:

1.2 The interaction of monetary policy with fiscal and macroprudential policy, including during crises and when monetary policy is limited.

If I was being cynical I would suggest that the report might return that the government should be able to override the central bank in times of crisis. You can imagine scenarios where the government wants to massively increase spending and get the reserve bank to facilitate that.

2.3 Its culture, management and recruitment processes.

The dreaded “culture”. Should be a fun read when the report comes out in 2023. We as mere citizens can be satisfied that when we need the RBA to be concentrating on a slightly dodgy economy, they will be spending their time answering questions about whether John in the accounts department is nice to Mary in IT.

After 30 years of independence are we witnessing the re-politicisation of central banking?

More bailouts

It’s not quite banking bailout time yet (it will come) but it is bailout time for energy producers.

In Germany, the state has taken a 30% stake in Uniper, a huge power company which operates numerous (mainly gas powered) stations across Europe. Uniper has been unable to pass price increases on to consumers for a variety of reasons, including fixed price contracts and political pressure.

To stave off the collapse, the German government has injected €8 billion of equity into the company and a German state bank has organised €9 billion in credit lines. The quid pro quo is the government will now decide the price increases for German consumers. Presumably none which will beget some more bailout money.

When banks are too big to fail people lose money. When it happens with energy companies, people freeze to death, so we can have some sympathy with the action taken here.

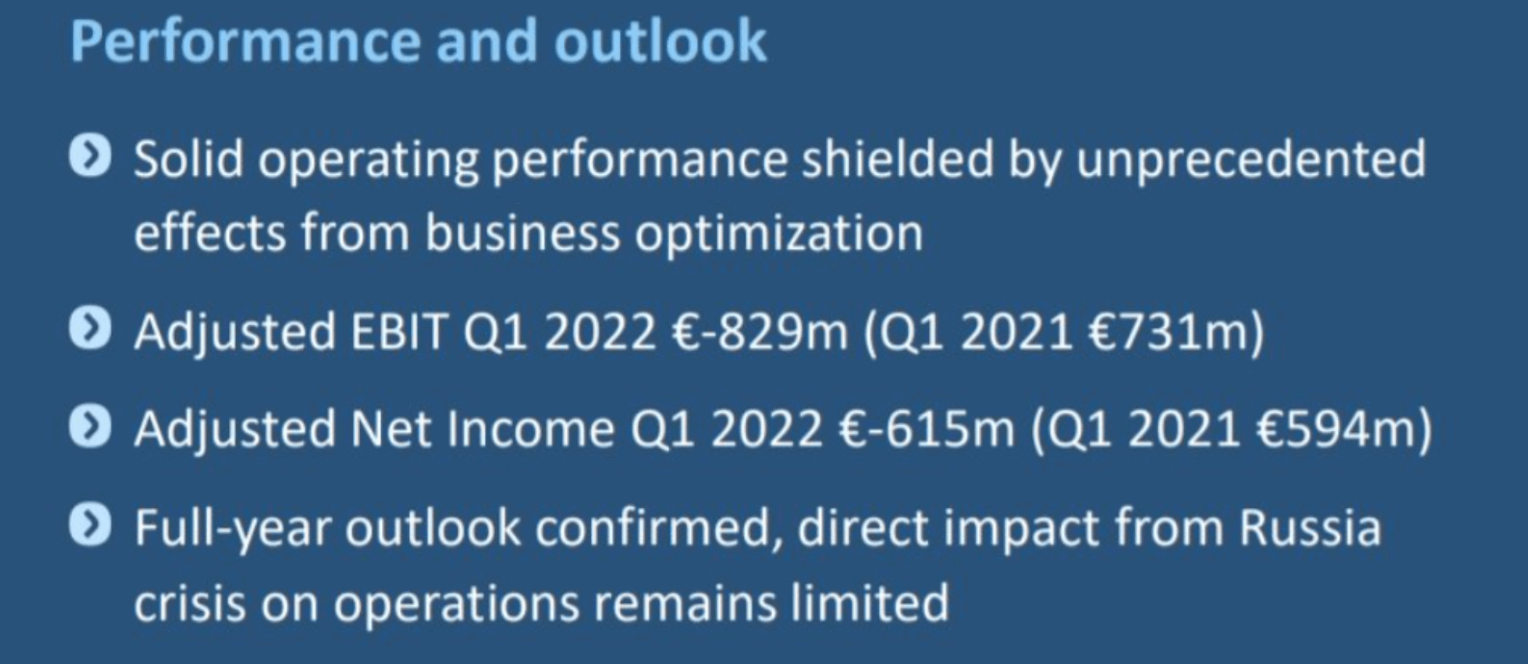

You might be a smidge nervous if you were on their board too because in May they confirmed the full year outlook was tickety-boo and the impact from the Russian crisis was ‘limited’. The shares have now lost 90% this year.

It’s not just Germany. In Belgium the partial nationalisation of their providers is underway. This is being done to secure funding to extend the life of their nuclear reactors, which they had planned to completely decommission in 2025.

In France it’s even more radical. A full $9.8 billion nationalisation offer on the table for their number one provider EDF.

None of this is that big a deal except that none of the governments involved have the money, so the magic printer in the sky will deliver again.

Et voilà, Monsieur Macron, la plus grande entreprise énergétique d’Europe. De rien.

3AC

More developments this week in the bankruptcy proceedings of 3 Arrows Capital. Allegations have now surfaced that the parent of Grayscale Capital Management (the world’s largest digital asset fund manager) was using another subsidiary to trade what was known as the Grayscale premium (now a discount).

The full analysis can be found here. It’s amateur sleuth stuff and all the better for it. In essence, the allegation (and that is all it is at present) is that Grayscale deliberately engineered a premium over their NAV, or at least did nothing to remove it, and then loaned money to 3AC via its related entity Genesis to trade away the premium for a massive profit. That massive profit should really have belonged to Grayscale unitholders.

It all worked beautifully until the tables turned and Grayscale started trading at a discount. Then the whole thing began to unravel and 3AC couldn’t pay Genesis back leaving them with a $1.2 billion loss. Nobody would ever have found out except for all the detail that turned up in 3AC’s bankruptcy revelations. Grayscale trades and 3AC trades are curiously coincidental.

The SEC will be doing backflips of joy here. If this is true they will hammer Grayscale in the upcoming lawsuit about ETF approvals.

I hope it’s wrong and though it pains me to say it, the SEC may have been right all along.

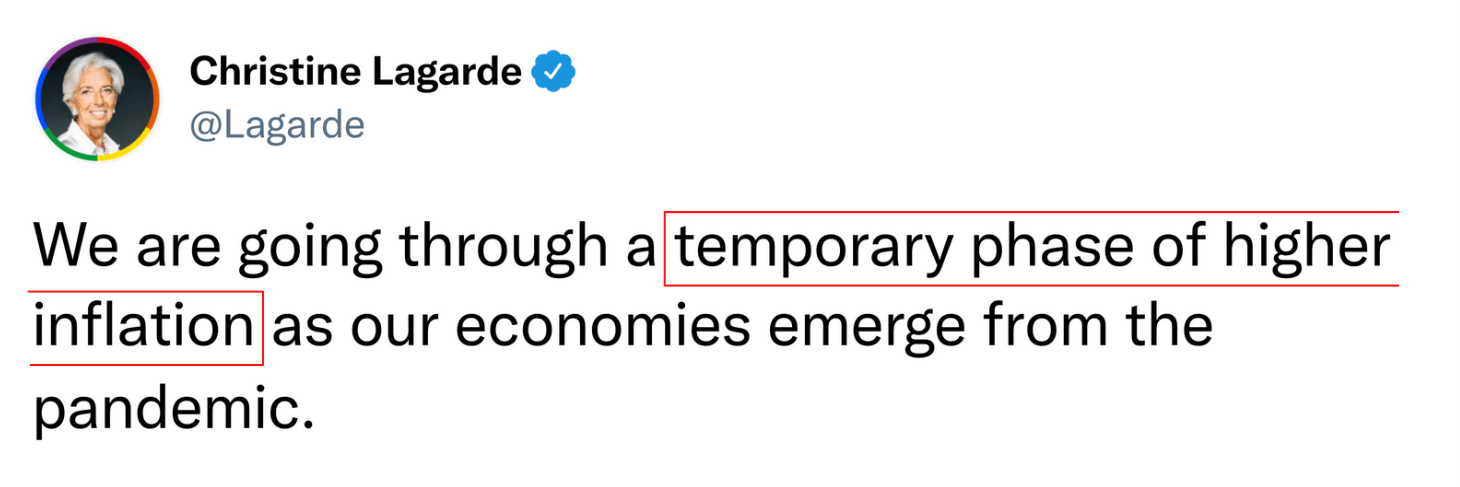

Euro-Trash

This week we dedicate Euro-Trash to the idea that it is simply impossible to get sacked as President of the European Central Bank.

July 2021:

September 2021:

October 2021:

July 2022: