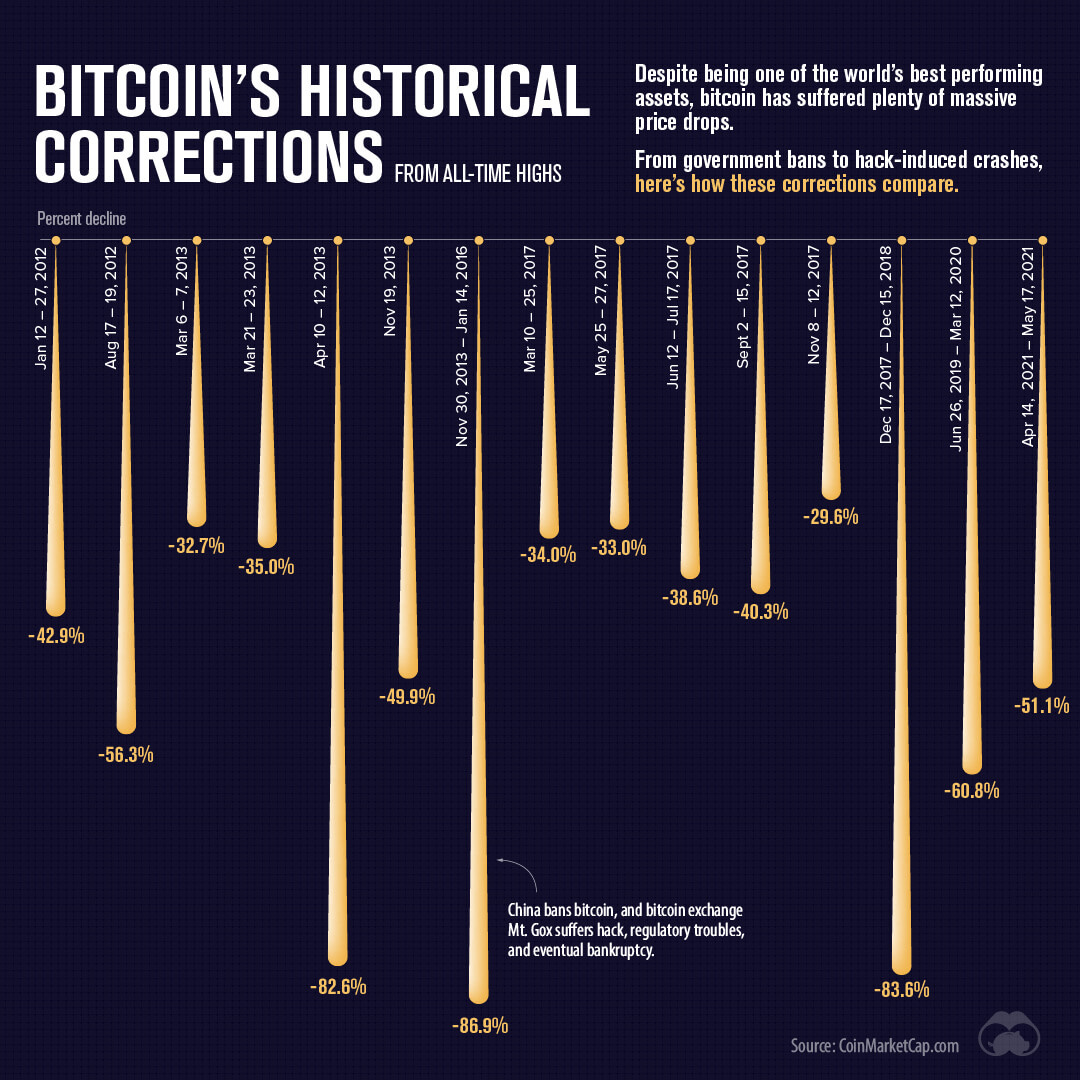

A quiet week

I confess it has been rather quiet on the inbound money side this week. It’s no surprise given the brutal plunge with perhaps more volatility to come. All this is nothing new for bitcoin or indeed for us as a fund. This is our fourth meaningful drawdown.

Our fundamental thesis remains unchanged and indeed is likely to be enhanced later this year when the bond market pain gets even louder. The economic backdrop means governments must choose between financial probity and certain electoral defeat, or more spending. They will choose the latter option.

It was not a good week for this sector, but being in the scarcest asset for the longest time is even more compelling now than it was in January.

LUNAtic

The near collapse of the stablecoin UST this week has not helped matters. It is a great reminder of why as a fund we have been deeply sceptical about some of these DeFi projects. The promise of 20% interest etc. is compelling but where does the interest come from? What happens when things go wrong? This week we found out.

The idea of UST (not to be confused with Tether) was something along the lines of the stablecoin would be backed by Luna, another cryptocurrency, and one would always be redeemable for a floating quantity of Luna worth $1. This would occur through the algorithmic issuance and redemption of Luna. It only works of course if there is faith that Luna is worth something. Luna itself had raised several billion dollars to support this mechanism and with it they bought a lot of bitcoin.

Initially things were going well though and the founder of Terra was adding to their reserves to defend the peg should it become necessary.

Guess what? Bitcoin’s price fell a lot. Faith in the peg between UST and Luna failed and UST started trading at 60 cents. Indeed it was failing so fast that even though it was true that you could redeem the stablecoin for Luna, by the time you received it, it would be worth less. Indeed Luna has lost 98% of its value this month so far.

At this point it is not clear who is holding the baby on the losses. There would be some professional market-making firms somewhere that are nursing biblical damage and undoubtedly their margin calls and liquidations have forced the rest of the sector downward.

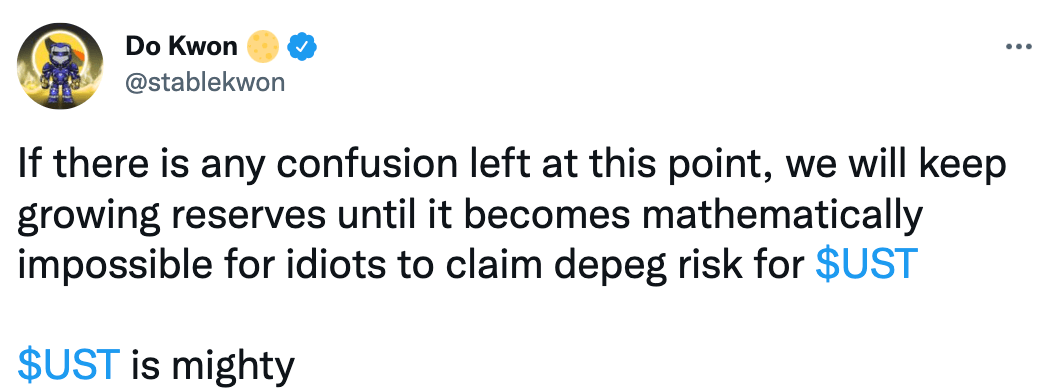

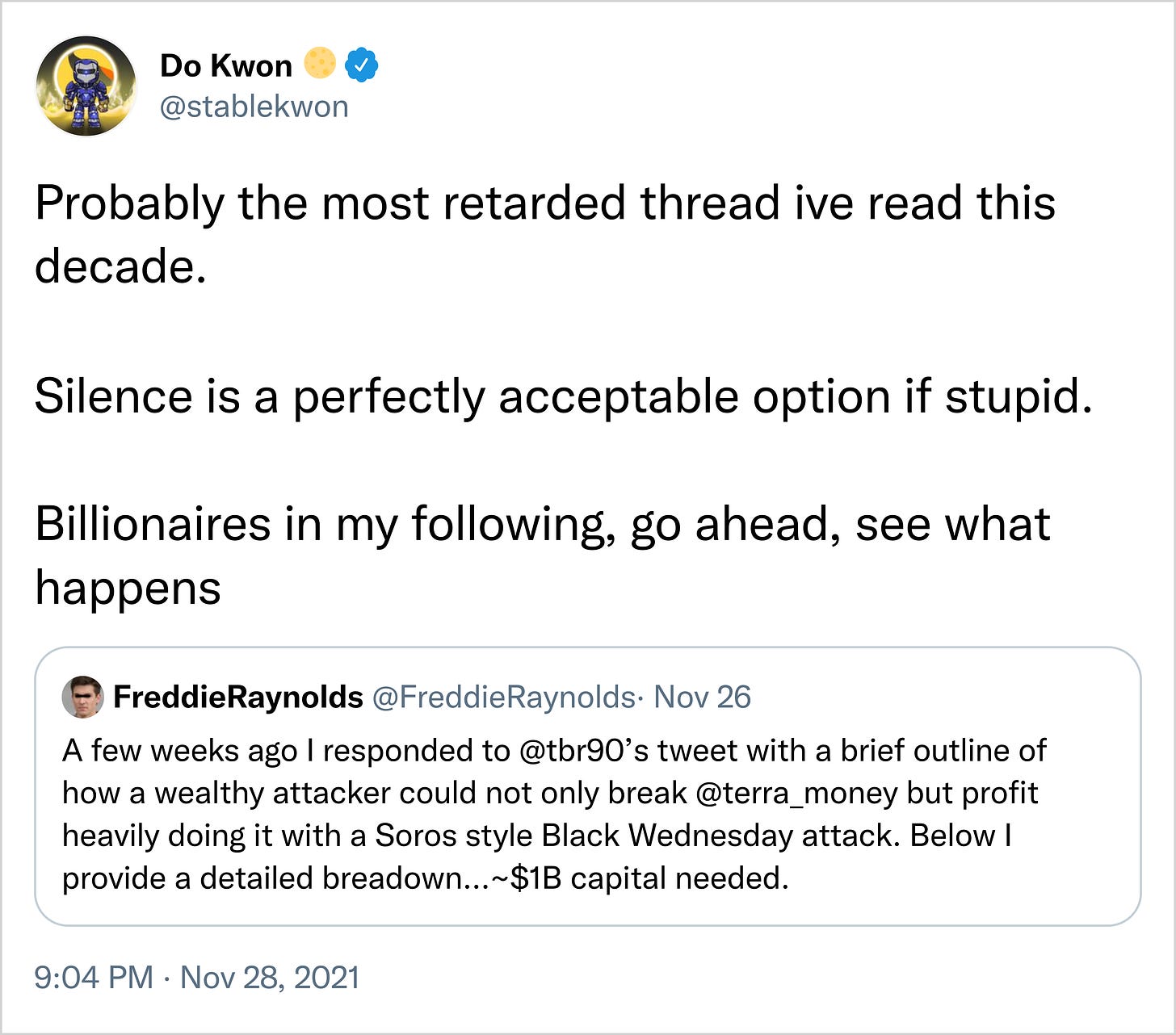

Back in November someone by the name of Freddie Raynolds laid out in a thread exactly how Terra could be unravelled. His entire thread is here. He set out that with $1 billion dollars of capital, it would be possible to destroy the peg. Here’s how Do Kwon responded:

Then this week, exactly as Cassandra Raynolds predicted, it all happened. Retarded indeed. Some billionaire did read the thread and they are now a multi-billionaire.

It’s not quite Soros breaking the Bank of England, but not far off because it was a very obvious play for somebody brave enough. The gains from this would be enormous and I salute whoever it was for their success. That’s capitalism, no bailouts.

Taper complete

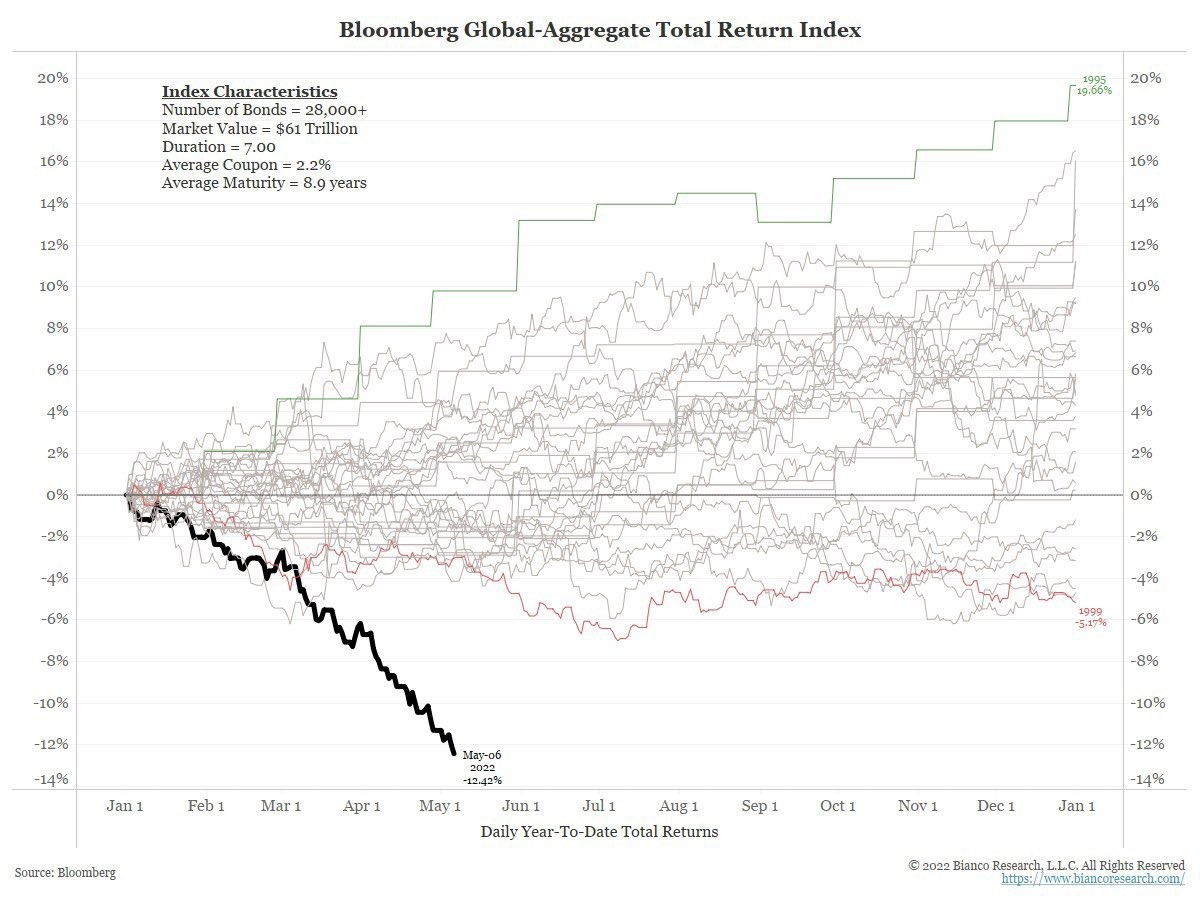

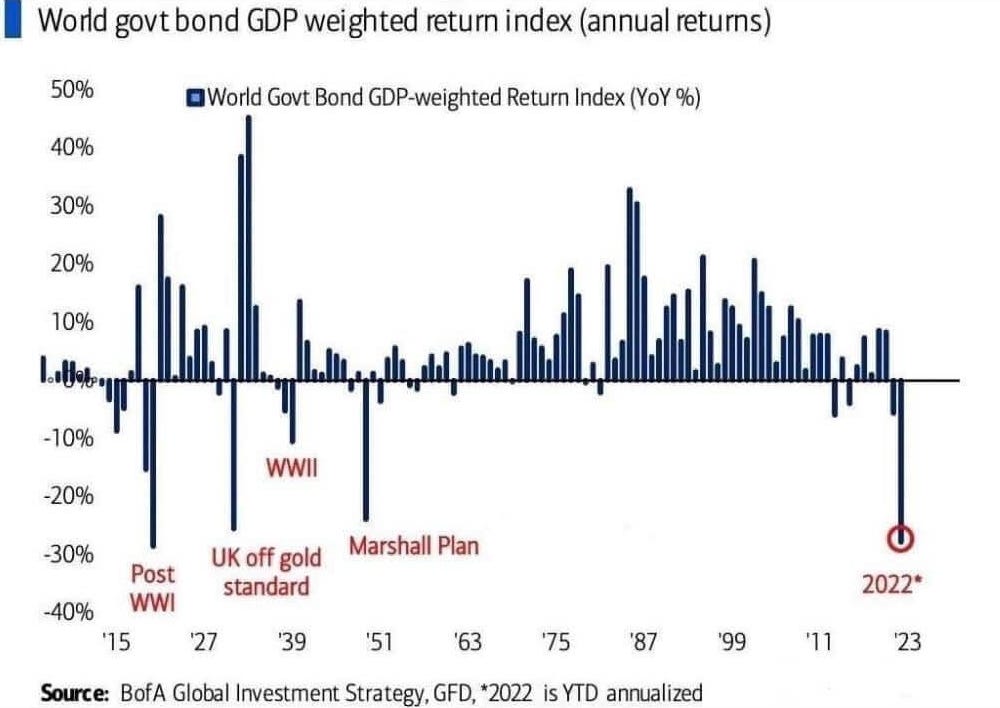

Elsewhere, this is now the worst start to a year for bonds in living memory. That would be fine except that bonds are meant to be a safe haven investment when things go wrong elsewhere. It is very unusual to find them moving in lock step with equities.

In the bond market you are not supposed to lose 15% of your portfolio before the halfway point of the year. It’s rather worse in the World Government Bond Index which is down 30%, helped by some defaults along the way.

Looking historically, these sorts of falls correspond to major events like world wars or massive changes to monetary standards (like the Gold Standard etc.) I believe 2022 could well be one of those years. Something will have to give, I would think the United States will be buying its own bonds again before the end of the year.

It just seems highly unlikely that we could have the government selling bonds to finance itself, while its central bank is also selling bonds to unwind QE (and apparently the plan is to sell them in a market where half the stocks in the Nasdaq are down 50% from their 52-week highs, a quarter are down 75%, and more than 5% are down 90%).

Book

While we are on the US bond drama, I think it is worth recommending this book from 2016. Set in 2029-2047, it tells the story of US hyper-inflation. Now six years old some of the predictions are already coming true. Scary stuff, and amusing too.

Euro-trash

It’s my favourite time of the year. ECB Annual Report time. First of all, the Annual Report does not follow International Financial Reporting Standards, mostly because such trivial things are for the likes of you and me, not the supreme overlords of the Euro. As a result we do not get all the information we otherwise might, like how much they spent on wine in the canteen and that sort of thing. What we get is nonsense, in 22 languages.

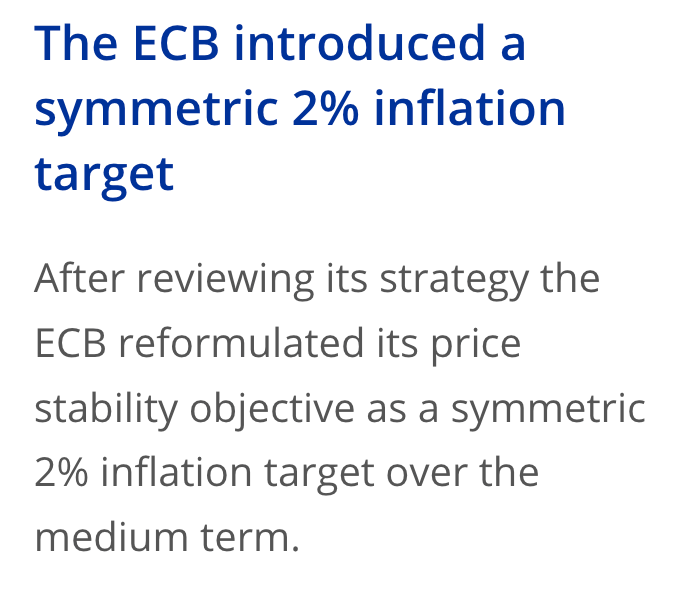

Trumpeted in the report as a major success the ECB introduced a “symmetric target” of 2% inflation. Nobody knows what that means other than for a decade they have got nowhere near it.

Inflation now sits at 3.5x the “symmetric target”. The only symmetry so far is that when they miss on either side, they miss big.

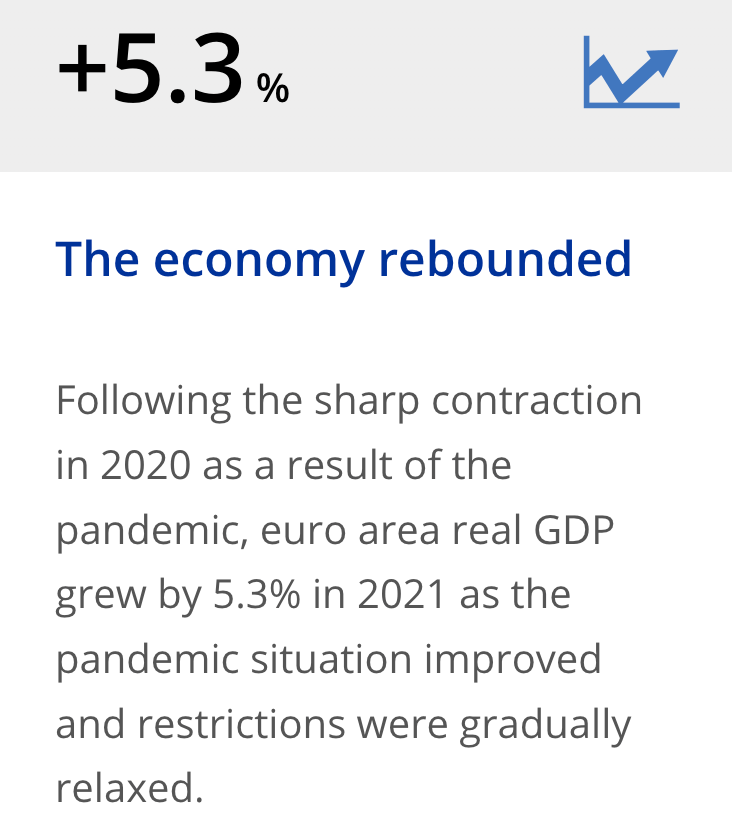

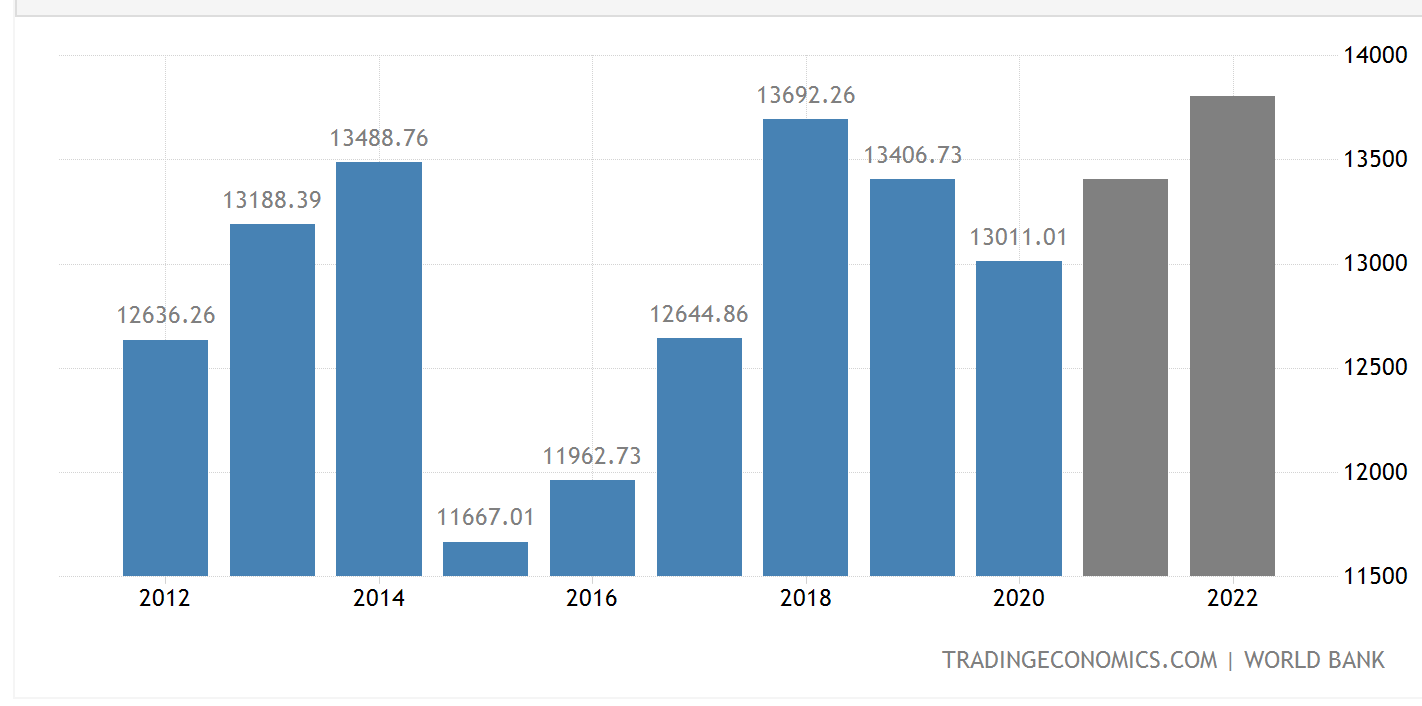

While we weren’t looking, the economy rebounded. The slightly more accurate truth is that in 2021 the economy was still smaller than it was in 2014. That seems scarcely believable but the independent facts from Trading Economics are rather revealing.

Finally, deep in the bowels of the report our favourite section. The pension note. Recall the contributions to staff pensions at the ECB are around 23% of salary. For the Board members, (and as a reminder there have only ever been 25 since the ECB was founded) the pension charge was €5 million. €833,333 per active Board member per year or €200,000 per year for all the Board members there have ever been.

It’s Marie Antoinette stuff. The ECB is extremely fortunate that nobody gets as far as the pension note.