Little Apple

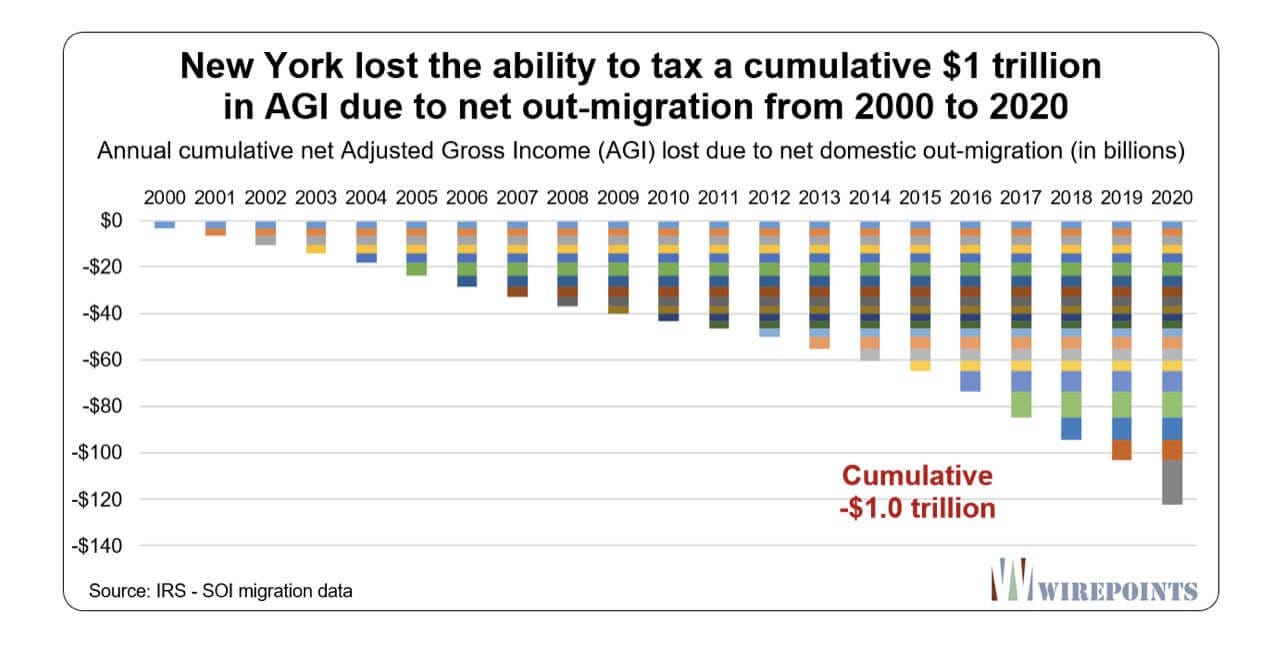

The Big Apple is getting smaller. Once the place we all wanted to go and visit; not any longer. There has been huge net migration out of the state since 2000. One million people have left New York since, for a net loss of 250,000 residents. That ranks the state top in the US for outward migration.

New York is one of the most indebted states in the US. A situation not helped by $1 trillion in potential taxable income being lost through the exodus. It has one of the highest state income tax rates in America at 10.75% (only Hawaii and California tax more – also huge losers in net migration). This is on top of the Federal Income tax rate of 37%.

New York ranks 50th (again) for the total state tax burden which is 14%, bringing the income tax burden to 51%. In European terms it isn’t high, but for America it’s astronomical.

When interviewed, the reasons given for leaving are the same. High taxes and crumbling infrastructure. There is no money to deal with the latter issue and not much room to increase the tax burden. The Detroit-style death spiral begins. It’s almost unthinkable that what happened in Detroit could happen to New York, but the statistics don’t lie.

New York needs to attract new industries and businesses, so it’s surprising to see New York move to ban bitcoin mining.

The legislature voted to ban mining that did not use renewable energy. In New York the miners currently operate at 60% renewable, which is higher than almost anywhere else in the US (and higher than every other industry).

This is the second time New York has legislated against bitcoin. They introduced the onerous BitLicense in 2015 which made running a bitcoin company in New York nearly impossible. Now the most innovative and fastest growing industry in America is being turned away.

It makes no difference at all to the network, which has been avoiding the state for years, but it is an odd way to run an economy.

It seems hard to believe that New York has somehow become the least American city in America. Freedom to choose what you do with your money or your computing power is higher in every other state.

The most powerful vote of all is voting with your feet, which is what New Yorkers are doing.

Interest rate decision

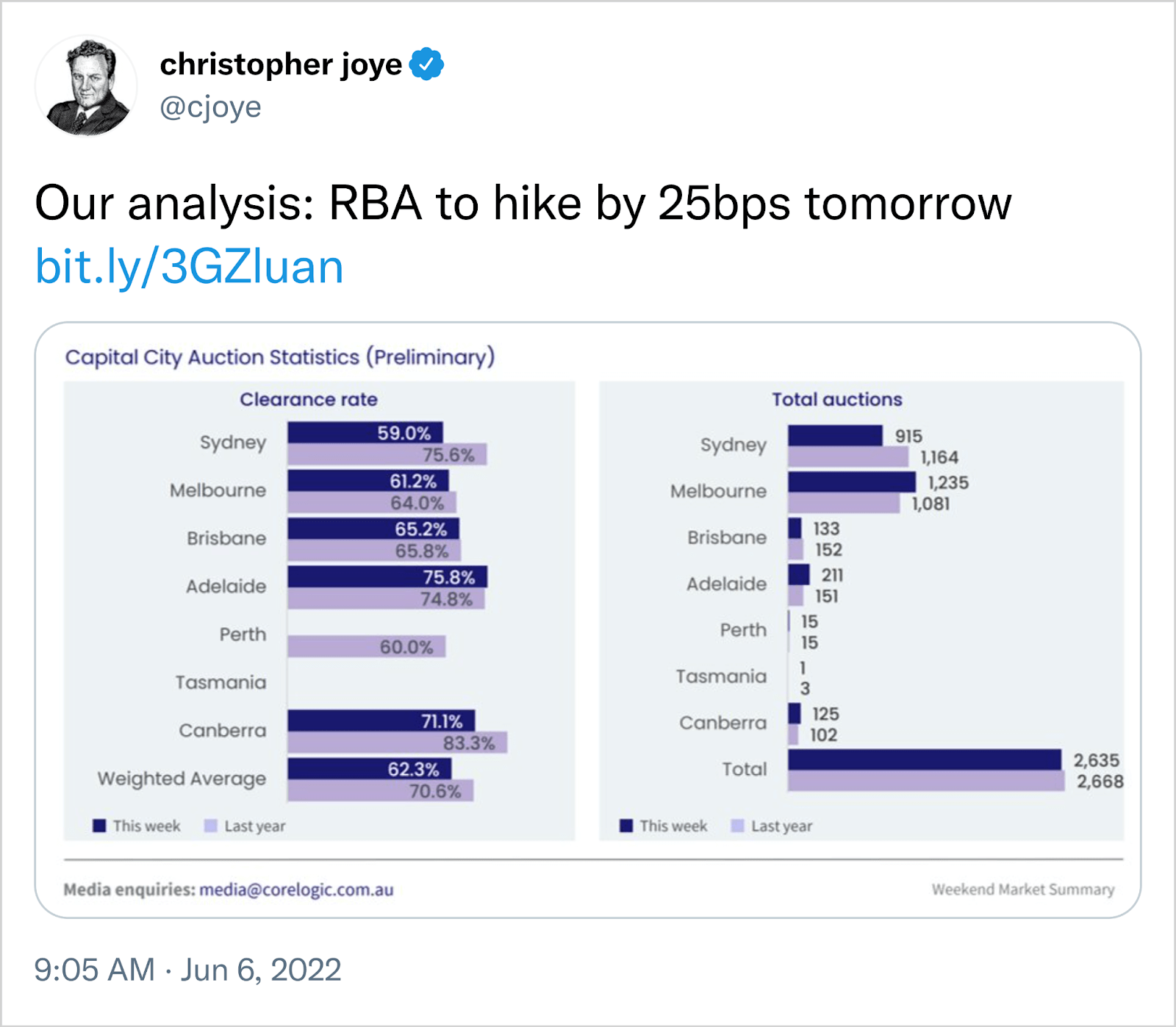

Our favourite bitcoin critic waded into the interest rate debate on Monday with his views on the RBA’s latest move:

The detailed (and 100% wrong) analysis waxed lyrical about the inside line to ‘Martin Place’ and how the 25bps move was entirely sensible and should be supported in full. Oddly, there have been no further interest rate analysis updates since the RBA hiked by 50bps.

In any event, the intricate debate about 25 bps or 40 bps is ridiculous because the real inflation rate in Australia is surely 8% or more. Australia has some of the highest housing debt in the world. It is a great innovator in new ways to lend and borrow money – see Afterpay.

People are not as stupid as most commentators suggest though. Borrowing money at anything less than 8% is like getting paid for doing nothing. The money is better deployed on income earning assets than frivolity, but the nuanced debate in the press about which micro movement in interest rates will come next seems to miss the point.

The average mortgage in Australia is about $600,000. At 8% inflation, that debt is being eroded at about $48,000 per year tax free. That is more than the after-tax salary of an average person. For many people the biggest single contributor to their net wealth is actually their debt.

If the interest rate is 0.85%, 1.85% or 2.85% while inflation is 8% then borrowing money for a productive purpose is a very good deal. Tell me I’m wrong, but surely the obsession with small movements misses the bigger point.

A plan

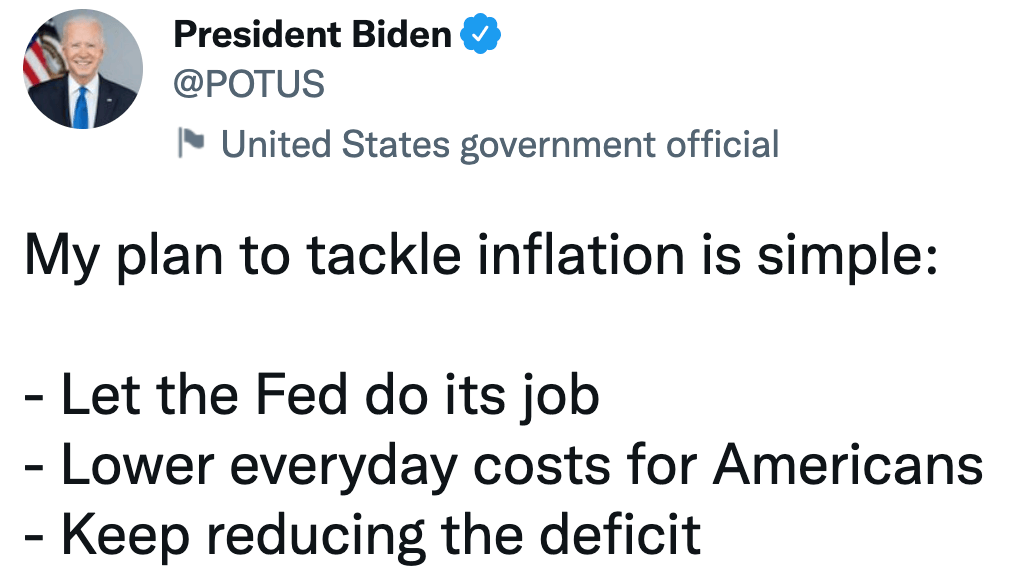

Joe has a plan.

He was handed the plan on the auto-cue:

- He will let the Fed be a knob

- Lower costs for everyday Iraqis

- Keep reducing the speed limit.

Joe’s deficit promise is convincing. 2022 is performing much better than its comparative years and has been helped a lot by huge tax receipts. Inflation is doing its work, tax bracket creep is working and sales taxes are reaching record highs.

To be fair to the American leadership, this is exactly why they want and need inflation. Their tax revenues will rise $900 billion this year. That’s the equivalent of the entire defence budget. It is the steepest rise in tax receipts in 40 years.

We are told it’s because the economy is booming, and nominally, I suppose it is.

A leaky ship

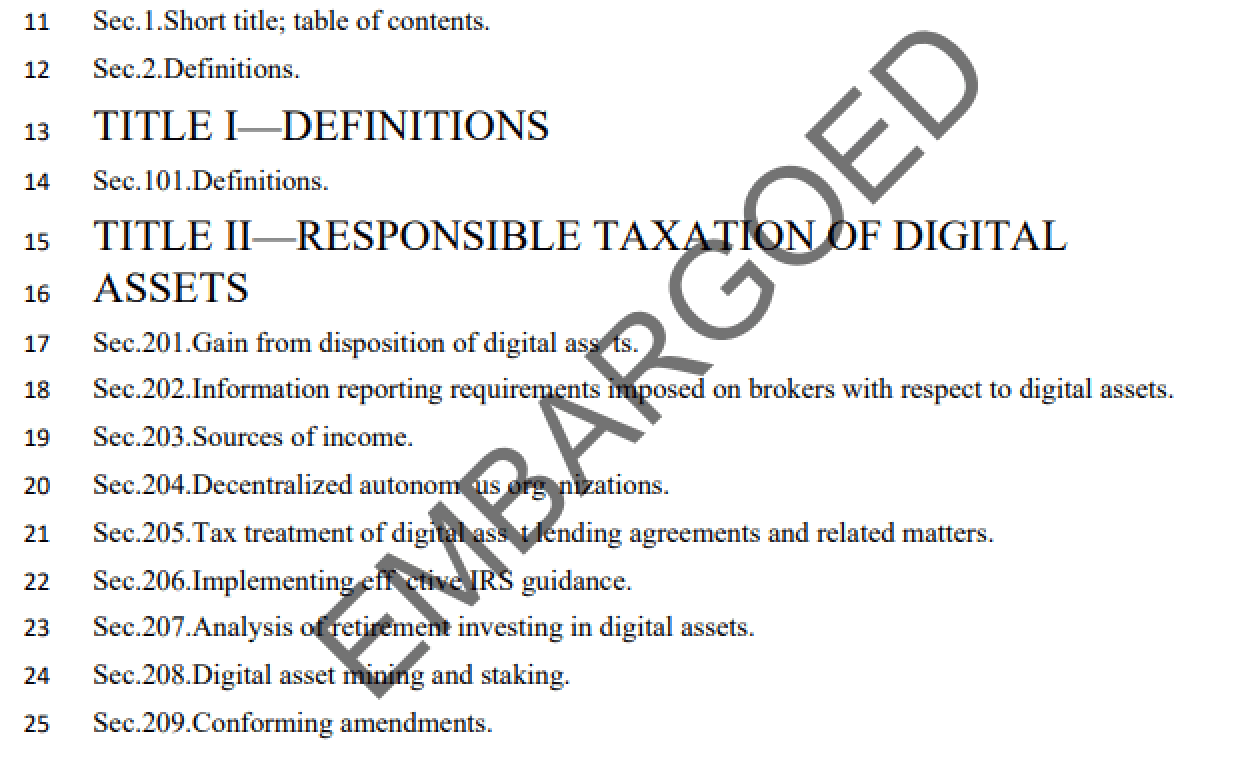

The US Senate leaked its draft crypto-regulation yesterday. It was a sneak peek into what’s coming down the line. Some of it good and some of it bad. This is not final legislation. Even so, the direction of travel is clear enough.

- Everything is a security, except Bitcoin (which is a commodity).

- Crypto-exchanges will need to register with the SEC. The cost will be high, only the largest can survive it.

- DeFi is going to struggle. A lot.

- Web 3.0 assets might be able to steer around this if they avoid financial incentives.

Where does it all land? With the bifurcation of the whole industry. Bitcoin and some of the exchanges become the white market. Everything else needs to become fully decentralised if it wishes to avoid the regulatory net.. Web 3.0 will be something else, probably with its own regulations.

From our perspective it is overwhelmingly good. We will see the continued legitimisation of the large exchanges (in which we hold some tokens). They will need to register and it will be expensive but they are going to survive.

The largest asset in our fund is going to benefit from receiving the same treatment as every other commodity out there.

There is one difference though: it is more scarce than all of them.

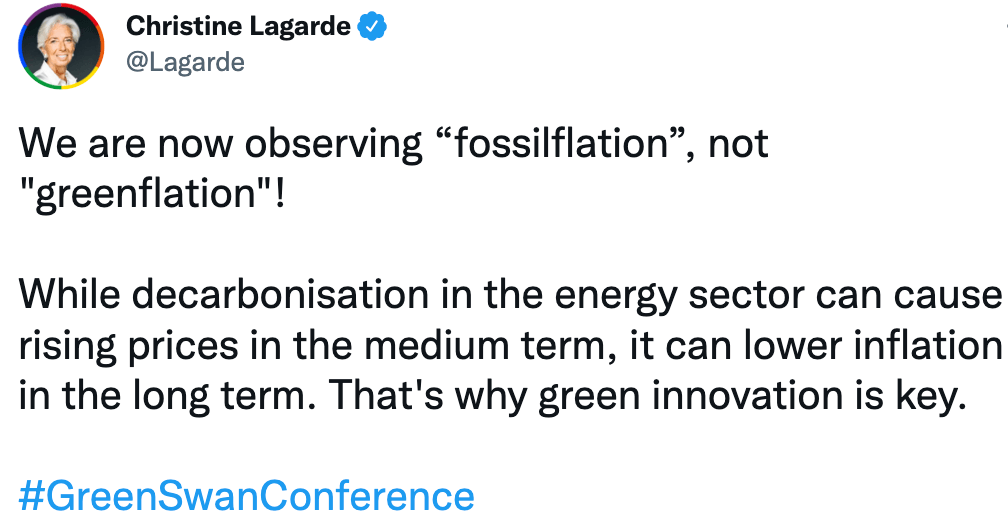

Euro-Trash

I suppose, if you are to blame for something, finding another scapegoat is a wise idea. In Christine’s case the scapegoat is fossil fuels. Inflation is the fault of fossil fuels. Indeed, the lack of them is the primary cause.

The occasion of these comments was the unusually named ‘Green Swan’ conference where several powerful central banks met to discuss their green agendas.

I would at this point mention that these policy areas are very much outside of the remit of central banks. The ECB has one remit: stable prices; the Fed has two: stable prices and full employment. Neither institution has climate in their remit yet they are unrelenting in talking about it.

This is not to diminish the real efforts of people who wish to look after the climate. Simply to point out that policy decisions on such matters are for elected officials only. Nobody even knows who these people are and yet they are setting the energy agenda by proxy while blaming their own failings on something they would like to control, but don’t.

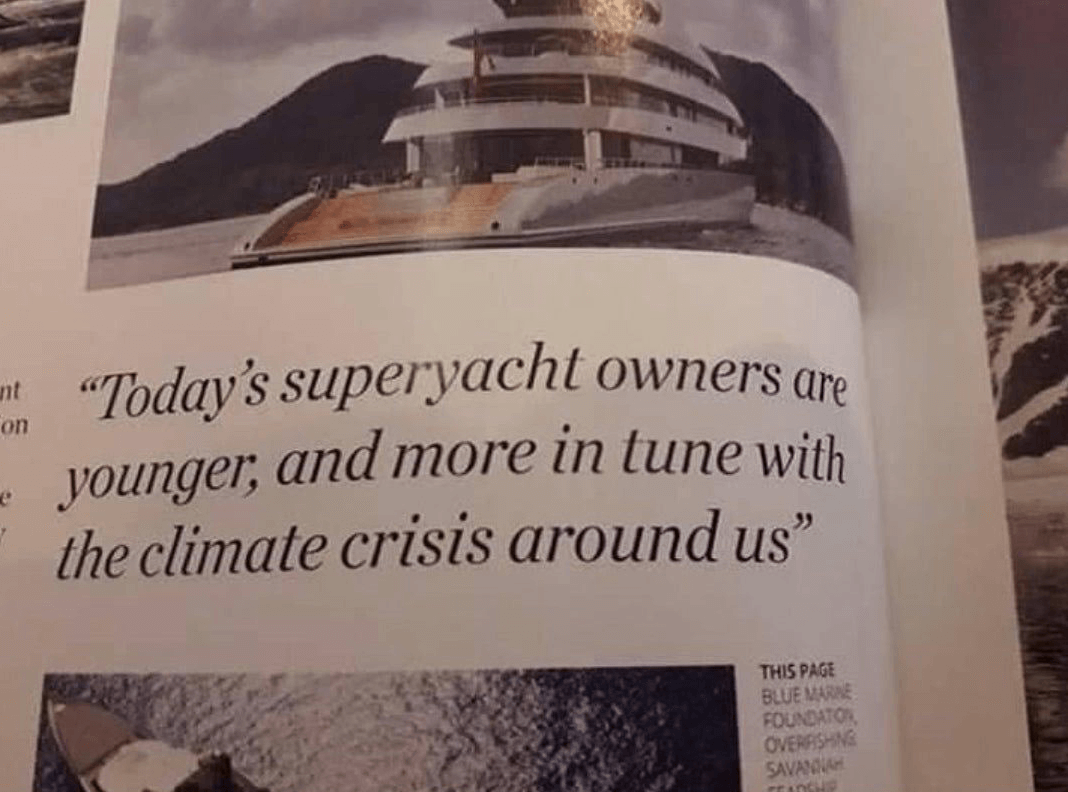

Joining Christine at the conference was climate bajillionaire, Al Gore. Al couldn’t make it in person so joined the conference from his 100 bedroom home in the California foothills. Photos of Al’s home kindly provided by Google Maps:

Al was emphatic and strong in his condemnation of all things energy consuming.

‘The entities responsible for emitting an endless stream of greenhouse gas pollution, and their investors, will be held accountable,’

Al did not join the conference for long though, something about the pool guy coming to fix the heating. Anyway, it’s been a while and it was good to see him.

The whole thing was delightful and it seems an appropriate time remind everyone of this article from SuperYacht Monthly in 2019:

I would argue not just superyacht owners, but central bankers too.