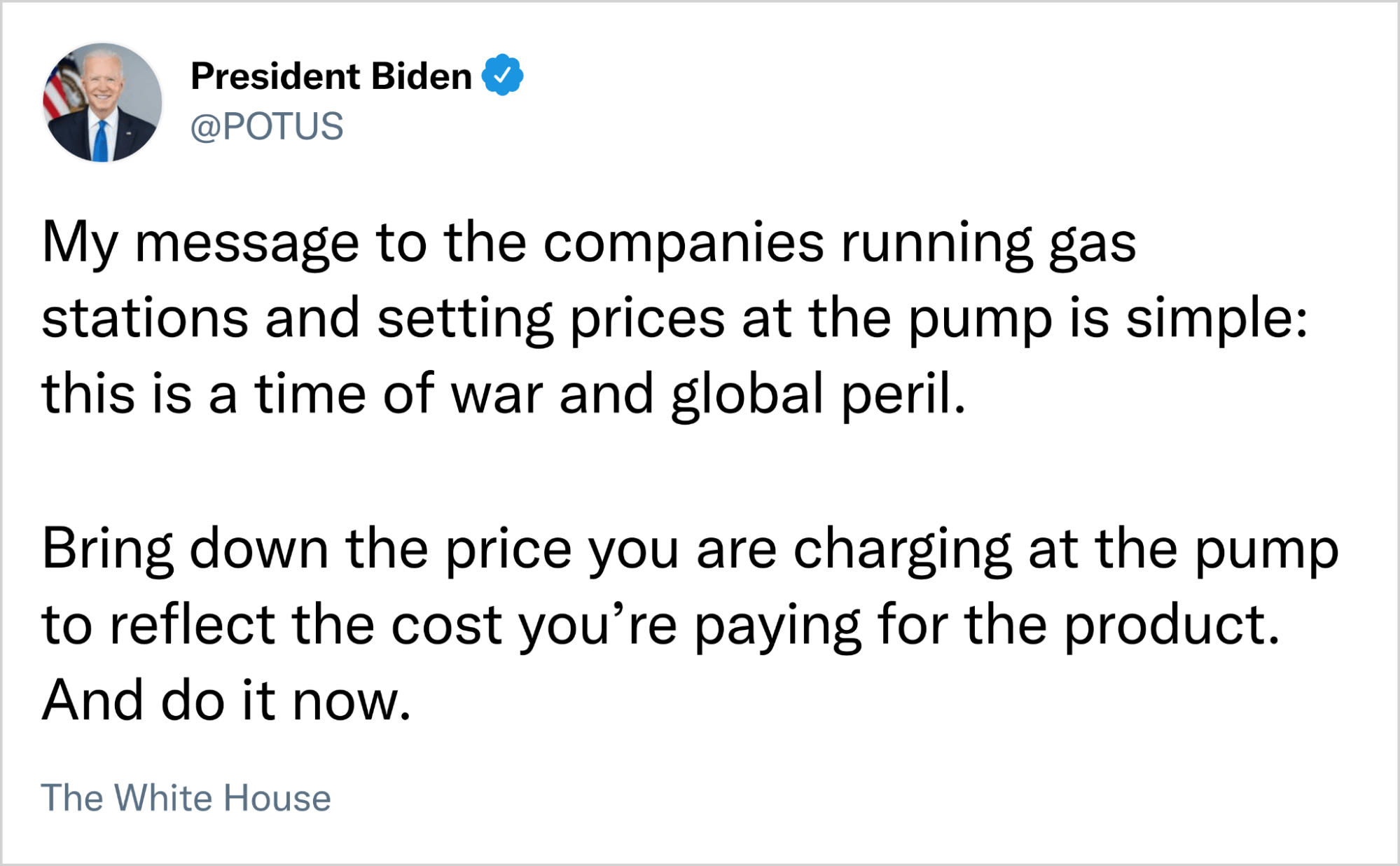

Price controls

This is how we control inflation now — by shouting. Evil oil companies are price gouging American consumers. Or, prices remain high because nobody can pick up a signal from the markets after the price mechanism was destroyed.

The true cost of inflation is that it makes economic decisions much harder. Do we drop prices at the pump when we might seriously regret it next week? If the consumer expects higher prices then why would we?

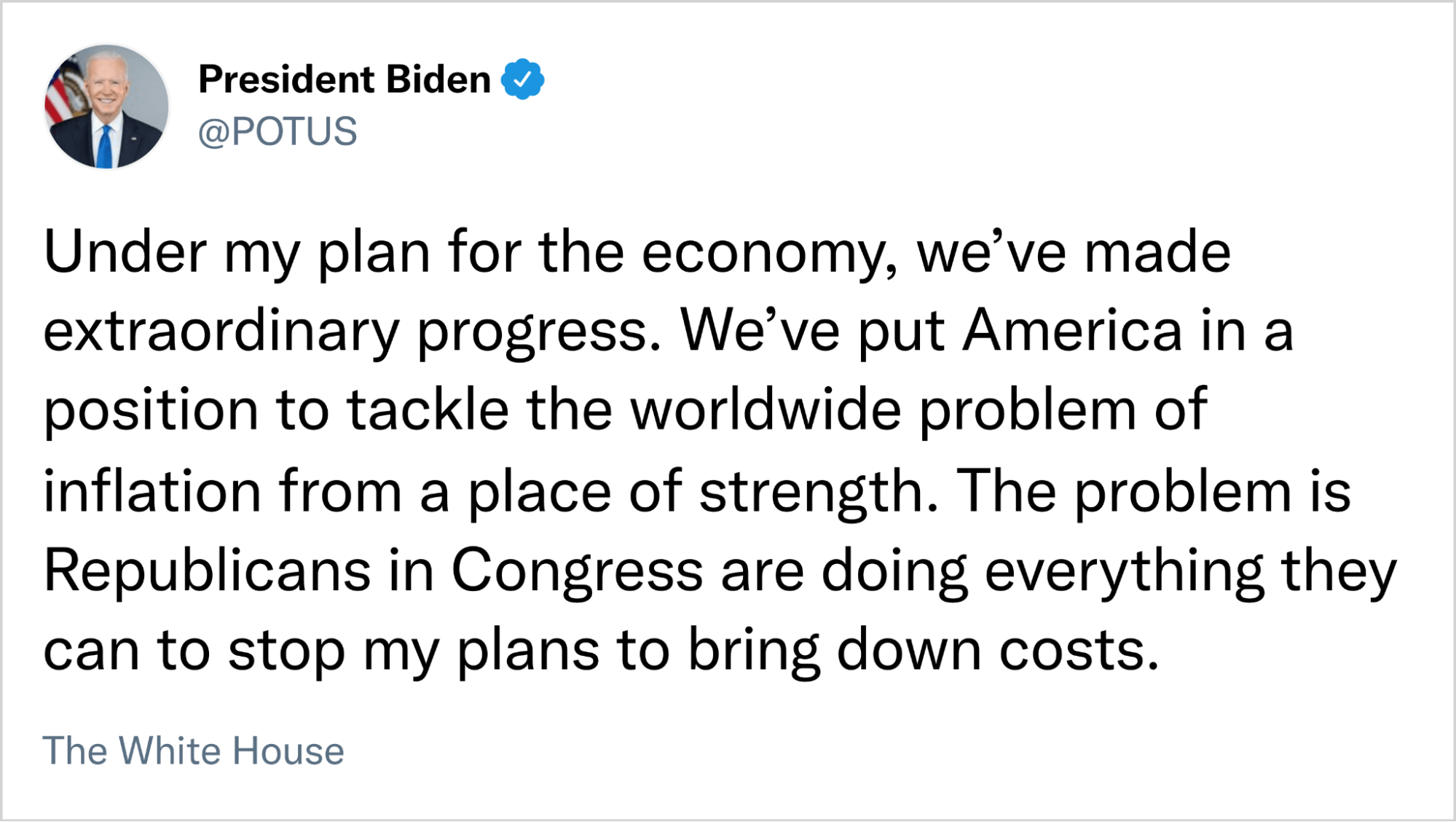

Biden then followed up with something even more strange:

Why is there a ‘plan’ for the economy? It sounds Soviet. For 100 years America let people run wild with their ideas and to invest in whatever they wished, charging pretty much whatever price they wished. This generally resulted in massive innovation and low prices.

The extent of the interventions isn’t limited to the Federal government either. In California, a new law requires landlords to pay tenants one month’s rent when they are evicted for non-payment. This is to facilitate the transition to new accommodations. What’s more, there are price controls on how much landlords can increase rent each year.

5% + inflation is a lot but you either own the property and charge rent in an open market or you don’t. Price controls are a dreadful weapon that distort market signals. All these changes will put people off being landlords and building new houses which is the last thing California needs.

Even in America, ownership of assets is at the whim of the government. There aren’t many things you can outright own and control. If you find any good examples, buy some.

Pay no tax

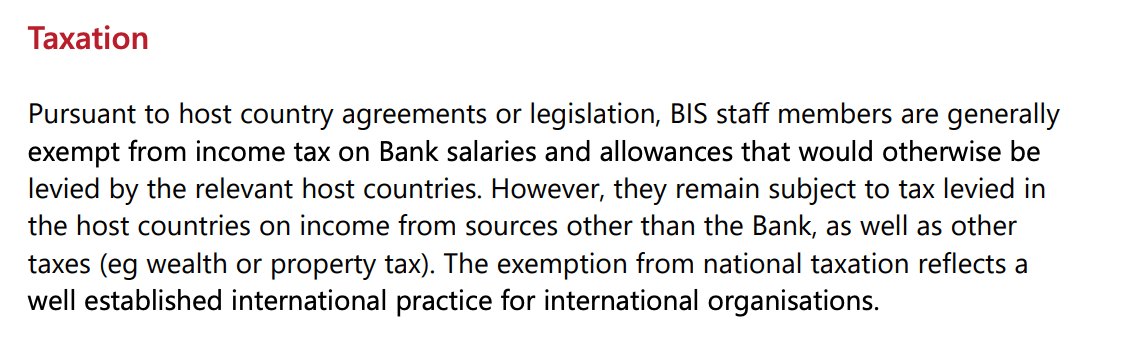

Annual Report time at the Bank for International Settlements. This strange institution is the central banker’s central bank and generally sets the tone for banking across the world. As we have come to expect for such an influential body, they are unelected.

What I did not expect was to turn to page 143 of their report and discover that their staff don’t pay any tax.

How can this be? These are the people who are designing the new central bank digital currencies that will track where you go and what you spend and most importantly that you do pay tax. Yet they do not.

The total salary cost of the 641 staff at the BIS was CHF143m for an average salary of CHF223,000 or A$330,000, completely tax free. No issue with the staff being well-paid, but not paying tax while designing financial infrastructure that makes sure everyone else has to is, let’s say, odd.

The Board members, who meet six times a year, are paid CHF120,000 plus another CHF120,000 for attending the meetings. I wouldn’t mind so much but amongst their members is convicted criminal Christine Lagarde and the imbecile who runs the Bank of England, Andrew Bailey.

To finish, let’s have a quote from the Annual Report from one of the many happy members of staff. Here is Jasmin, who works in the headquarters in Basel Switzerland.

“I am part of the Physical Security Team and work mainly at the main entrance of the Tower and the security desk of the Botta building. I am also responsible for preparing the access badges for meeting participants.”

Not bad for $330k, tax free.

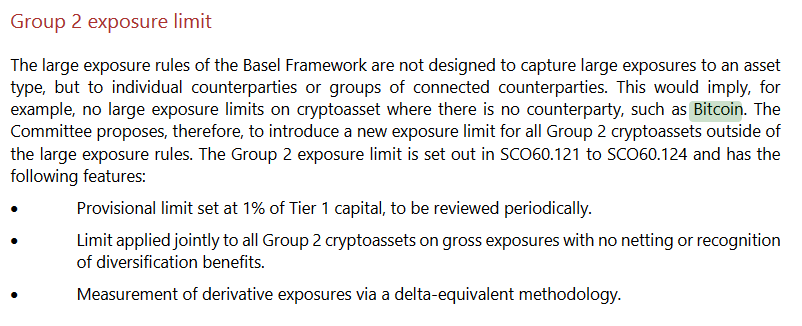

BIS

Apart from their non-tax paying nonsense. The BIS did present something interesting. Their discussion paper on bank reserves proposed that crypto-assets might be included.

The material acknowledgement here is that bitcoin ‘has no counterparty’. We have discussed many times now that bitcoin is pure collateral. We have paid the price for that in the last few months because the collapse of DeFi has meant the mass liquidation of the mainstay asset of our industry. It proved something though — that bitcoin works.

If you think about gold, many banks hold their gold in London or New York. If war breaks out the counterparty risk will rear its head and you will get your gold ‘later’. Another good example would be Russia’s international USD reserves which were seized earlier this year. Irrespective of their behaviour, counterparty risk exists at the nation state level.

This is a serious ‘coming of age’ time. Once bitcoin makes it onto the balance sheets of retail banks there won’t be a bank in the world that won’t have at least some. The next step will be central bank balance sheets.

Hot chips

The strangest feature of this market has been the continued march of bitcoin mining. There are signs of stress now among the least efficient operators but the hash rate, the measure of total computing power dedicated to bitcoin mining, has been resilient throughout.

Intel’s head of ‘Accelerated Computing Systems and Graphics’ group announced the launch, specifically designed for low energy consumption. The whole game in proof of work mining is to have the lowest energy consumption for the maximum processing power.

The intel chip consumes 26 joules of energy for every trillion calculations. It’s impressive stuff. The chip is doing one trillion calculations using the same amount of energy as having a lightbulb on for half a second.

The nearest competitor is Bitmain whose latest chip uses 29.5 joules. The 13% difference is huge in mining and can determine the winners and losers.

Not to be outdone, Samsung has also moved into mining chip manufacture. Nothing formal has been released yet but competition is getting hot. We now have Intel, TSMC and the Koreans all making chips for proof of work mining.

Critically, it is not computing power at any cost, but computing power per unit of energy input that matters. The chips have to get more efficient, not just faster. When you consider the amount of power that computing uses around the globe there is one industry that is pushing the frontier of low energy use and that, contrary to public opinion, is proof of work mining.

Euro-Trash

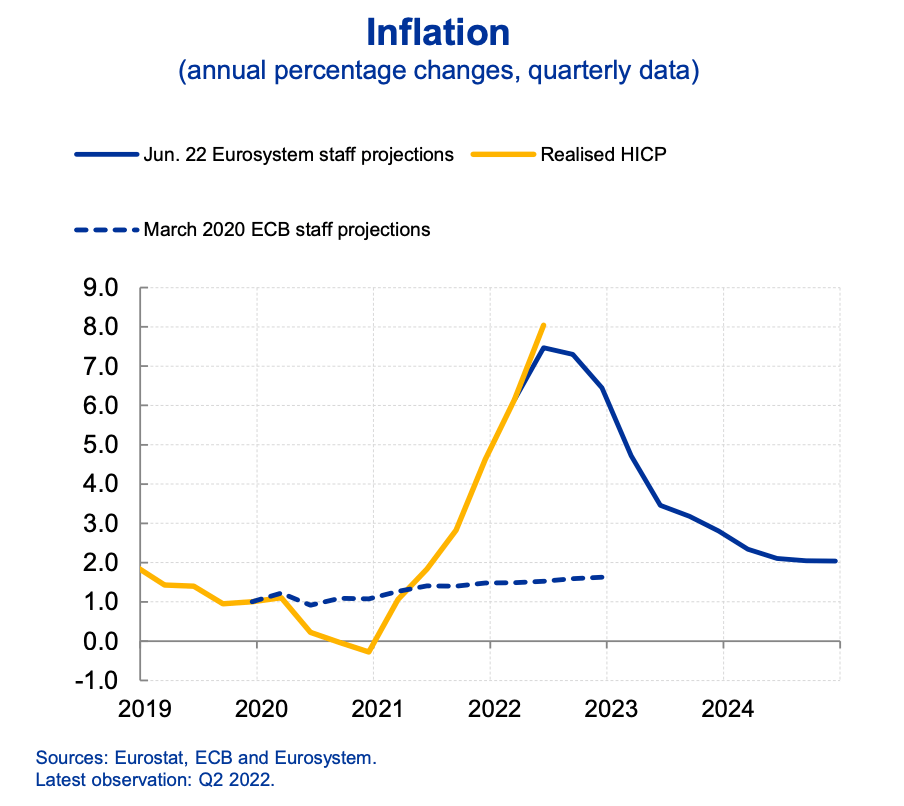

The ECB were back on the road this week with a presentation on inflation. This slide stuck out and was presented without irony. The ECB staff projection for inflation was for 1.5%. Inflation then jumped to 8% before they casually adjusted their expectation by a factor of five.

The presenter said “following the adjustment of our expectations we expect inflation to fall back towards our target by 2024”.

I’d call this not just being wrong, but being so monstrously wrong as to be incompetent. To then present it as “oh well not to worry” is unforgivable.

There is a very real cost to making a complete arse of it and here it is:

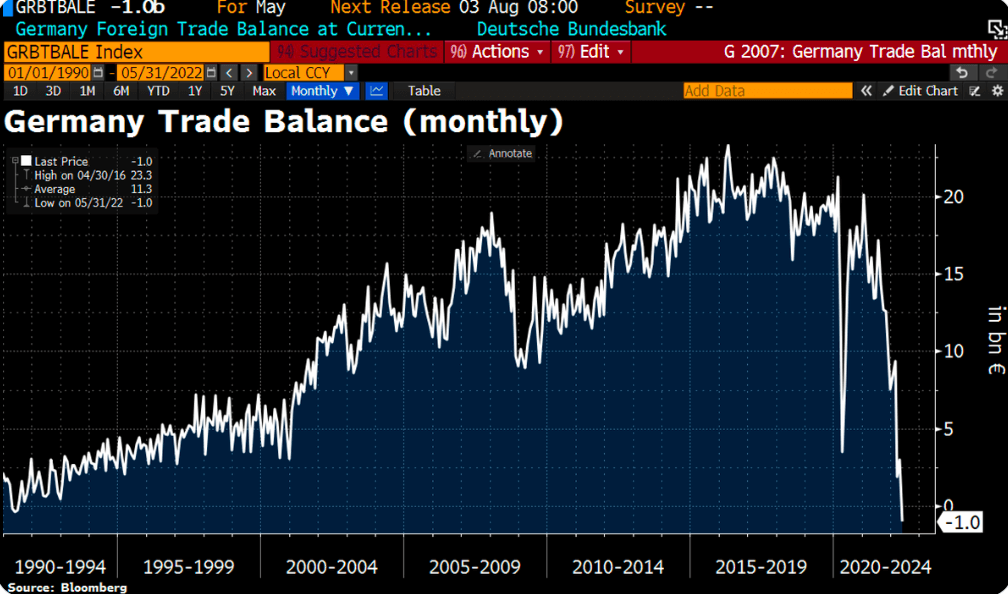

The German trade balance is now negative for the first time since 1999. Nearly a quarter of a century of industrial dominance is at risk because of some terrible decisions. Most things in Europe don’t matter too much provided the German economy is ticking along. Italian and Greek bond yields don’t matter, provided the Germans can pay for the difference. Unemployment in Southern Europe doesn’t matter provided the Germans can keep making transfer payments to keep the Union together.

This chart is not good. Hopefully it turns around. An upset Germany is not what we need right now.