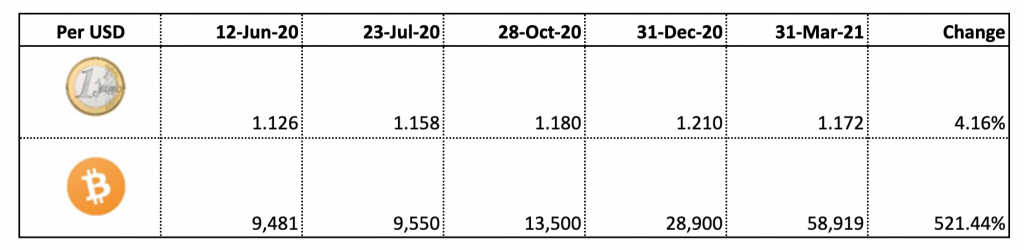

Quarterly performance

Fund Managers love quarterly performance, especially when it’s good. “Here are all the amazing things we did with our brilliant and insightful analysis that’s three miles deep and two inches wide” or whatever that Scottish sounding bloke says.

Fo us, quarterly performance is really irrelevant. Time and again, I urge people to just look beyond the four-year horizon that bitcoin operates on. That’s all you have to do. Think about 2025, the supply of bitcoin per day will have halved again, the whole ecosystem will be vastly more developed and the work going on right now will be paying dividends.

We will have good quarters and we will have bad ones. I think the sector we are in is the right one for at least the next decade. It is exciting because most people still laugh at us. They haven’t taken the time to understand the sector at all, but they will. We are not doing anything complicated; we are not using leverage or derivatives. We aren’t double thinking ourselves with complex trading algorithms, that triple pike with twist before executing a trade.

Simply, we are alive in the digital universe buying things we believe have an economic imperative, that are both useful and scarce. Then we hold them.

Even so, I enjoyed the bamboozlement of my inbox this week:

“an outstanding quarter of +5.7429% against a adjusted NASDAQ benchmark of +3.4643%. Accounting for exchange we did even better, with our insanely complex foreign exchange anti-matter long-but-short-but long derivatives, that not even our bank understands, enhancing performance by width of an atom (before costs)”

We discussed the Build Back Better conspiracy in November last year. Governments around the world simultaneously announcing new railway lines and underground tunnels that would help us defeat an invisible virus. It didn’t sound that credible actually.

Unfortunately, nobody told Joe Biden

“I’m convinced that, if we act now, in 50 years, people are going to look back and say this was the moment that America won the future”

- Some shiny new cars: $230 billion in funding to create a national network of 500,000 electric-vehicle chargers by 2030.

- Fewer potholes: $815 billion over eight years to modernise America’s roads, highways, bridges and airports.

- Faster internet: $500 billion for high-speed broadband.

- The removal of lead pipes: $45 billion to replace every lead water pipe.

I read an excellent book on this topic last year, which I may have shared before, called Stronger Towns. It lays out the issue with the way America was built, the sprawling towns and highways. It’s a disaster that leads to inevitable decline (see Detroit). Essentially it happens because of a lack of urban density, large out-of-town retailers benefit from the new roads but they don’t pay for them or even come close with their municipal taxes. When these things are costed, the ongoing maintenance cost is almost never included. The same fate ultimately awaits China but for now, everything they have is shiny and new.

So, while America spends its future resources on tarmac and lead removal, the Chinese will almost certainly be exerting theirs on artificial intelligence, robotics and something that they referred to in their Five Year Plan as “digital industrialisation”. They are also deeply involved in blockchain development and bitcoin mining, amongst other things. The Americans are miles behind, and on the back of this plan, they will stay miles behind.

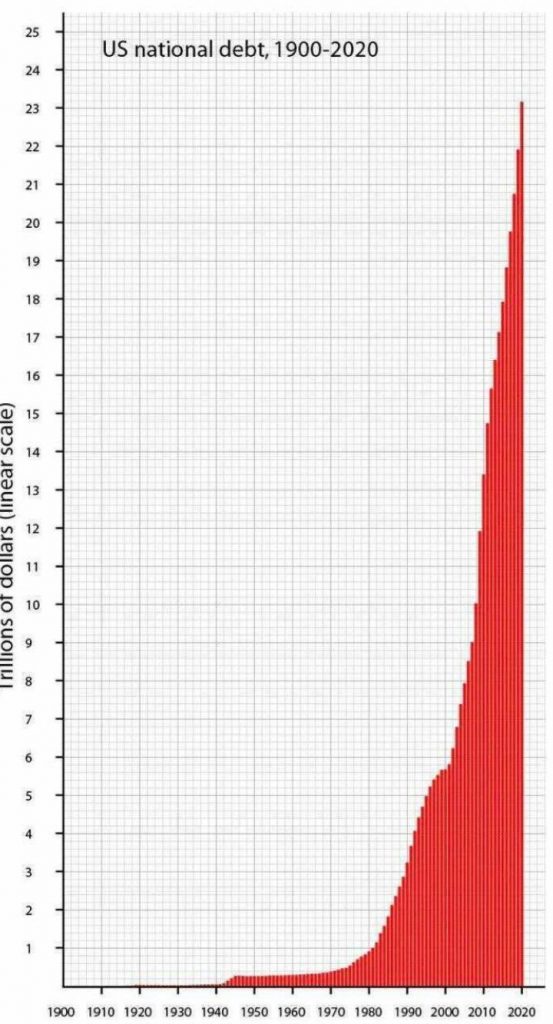

America’s biggest infrastructure project is set out below. It is their version of the Burj Khalifa and clearly shows they are living beyond their means. Until a President arrives who tells them that, the time bomb will continue to tick.

Incidentally, the building of this tower continues. It stands $28 trillion tall now, and when Professor Plum has finished with his lead pipes, it will be even taller.

Great graphic here from Bloomberg describing the possible alternatives for Central Bank Digital Currencies. Two of the three options cut commercial banks out of the loop altogether, it’s no wonder they aren’t terribly keen on the idea.

It has to be said that the possession of a banking licence is a fabulous privilege and if I had one, I would be rather keen on protecting it too. You might consider from the inefficiency of these organisations that the privilege is abused by the incumbents. In Australia, the big four banks are gigantic bureaucracies which have become arms of the Australian government. Westpac employs 36,800 people, ANZ 37,500, CBA, 43,500 and the NAB 35,000. Between them, it’s the same number of employees as Apple.

Perhaps they aren’t comparable, but Apple actually make and design things, it’s labour intensive. Banks open accounts and write loans, just like they were doing 100 years ago. Arguably, you should get better at it after a combined half millennium of practice.

The madness of these businesses is compelling to watch. They are closing branches at a rapid rate so that they can reduce their cost base and “compete” in the digital space. That physical presence is perhaps their only advantage, their IT platforms are like something from the 1980’s, changing them is nearly impossible because of their deep integration and requirement that the regulator sign everything off.

This is from the Westpac:

The recommended minimum length for a password these days is 12-15 characters, plus some two-factor authentication. I know the example is silly, and I’m sure Westpac know that this isn’t how it should be done. It is simply to demonstrate how hard it is to change simple things in large organisations with old systems. A big bank wouldn’t take this risk unless it had some nightmare technical consequences for them.

As we stand, the big banks drive cars in a race where everyone else has to run. It seems to me their strategy is to get rid of the car because “it’s too expensive” and they will run like everyone else. At best, they only have one leg though. We are witnessing that as their digital “strategies” unfold.

I came across this during the week. Richard Field is a director of the Institute for Financial Transparency, so I assume he has a reasonable grasp of matters economic. Probing a little further into the narrative, he contends that wages are not rising and have not really risen anywhere for 10 years. Accordingly, he concludes deflation is the name of the game. I agree on wages, but I’m not convinced otherwise.

Back in the 19th century, with a mainly agricultural economy and locally based labour, the transmission mechanism for price was the cost of labour. The number one input into all production was labour. So, if the price of a strawberry picker in Cornwall went up, then the price of strawberries went up. In the 20th century, labour was still a massive factor in production, think Model T Fords with their huge production lines and workforces, this was still true for the large part of the last century.

Today’s production lines are a little bit different, capital is the name of the game and if the price of labour rises there are multiple alternatives. One is machines, another is finding someone else on the end of Zoom that has the skill and lives somewhere low cost.

For example, the level of automation in an Amazon warehouse is just incredible. I follow a company called Boston Dynamics (who build robots) to check out what the latest hardware can do. This one is simple stuff and weirdly compelling to watch. I much prefer their videos like this one about practical robots to the ones of robots doing gymnastics. This one can unload 800 boxes an hour for 8 hours on one charge. If they are plugged in they can keep going 24/7. Simple, boring and useful.

The more central banks try and lift wages through depressing interest rates, the more incentive there is to invest in capital like this. I imagine Amazon can borrow at just about zero percent, which makes robots almost free. Ultimately the economic returns of any economy are split between capital and labour, that split does not need to favour either side it will simply favour the most cost-effective side, and for almost everything now, that isn’t labour.

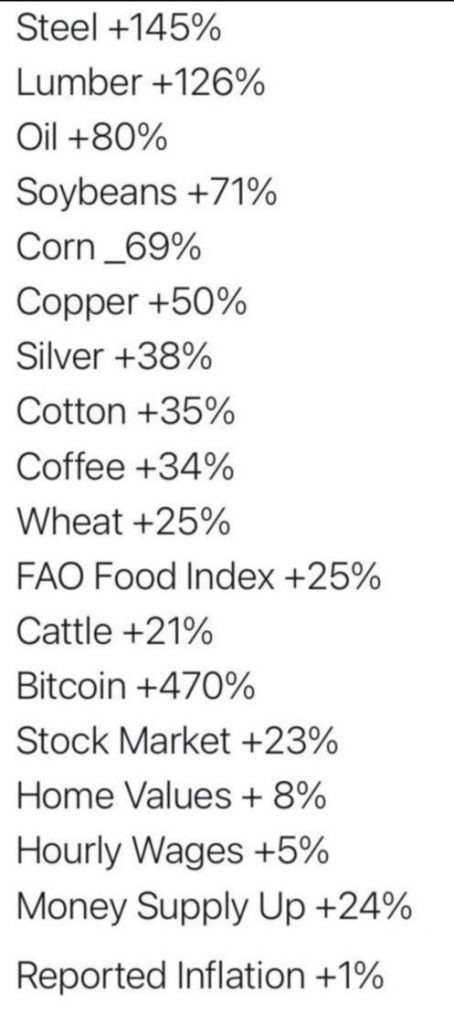

Looking at prices since June 2020, you’d be hard pressed to say they aren’t going up. The comparator is clearly depressed because June 2020 was mid-lockdown almost everywhere, but still.

Yet, reported inflation is 1% and wages are not rising.

How? Well, it’s simple. The returns are going to capital and not to labour. If you own machines, land, computer code, IP, knowledge, etc. then you are doing well. Everyone else is getting materially and meaningfully poorer. Fortunately, the efficiency of the machines actually holds down the rate of increase of finished goods prices and offsets the input prices. That won’t help you much though if you are low skilled and looking for a pay rise, it isn’t coming I’m afraid.

The solution is not an easy one but the default for governments will begin and end with tax, a lot of tax.