Safe Haven

“and so, it’s become absolutely clear that bitcoin is not a safe haven asset”

I was watching Bloomberg on Monday as the Japanese market went into meltdown, completing its worst day since 1987. Some talking head (from an Australian investment firm) popped up and made the declaration about bitcoin. The only place you can really be now is bonds, he said.

We cannot pretend that intra-day drops of 20% are any good but it misses the point as far as I’m concerned. If you put the focus on Japan, where the drama started, you will see why. The carry trade that has sustained Japan for so long is starting to unwind as they are forced into raising interest rates from zero. It’s consequential because when you model a carry trade, the rough maths is:

Japan will pay me 0.5% to borrow from them. I can buy USD and they will also pay me 4% to lend to them. The Yen will likely depreciate under these circumstances so I also need to hedge that. There will be some margin. I will model extreme currency scenarios that have been seen before.

What you likely will not model is a 10% move in the Yen over a short period. Yet, that is what happened and it is quite likely that all the micro gains of the carry trade are wiped out in one fell swoop.

Safe haven trades cannot behave like this. The premise should be that my safe haven trade will deliver me the same features at the end of any drama as it did at the start. In the case of Japan, the relatively safe carry trade has now failed because all the features that made it ‘safe’ changed. Interest rates moved against you in both the US and Japan; FX moved against you; the economy moved against you. All the features of the trade changed. The very best people at managing these scenarios made money and everyone else did not.

On Monday Bitcoin fell 20%. Today it is still delivering blocks every 10 minutes. The issuance curve has not changed, it still has no staff and no marketing budget and its key features remain the same. In five years that will still be true. None of the key features have changed or are changing.

We could put this another way. Imagine you could buy a property. Initially the property would be small and would have a modest view of the ocean. Each year, the properties foundations would get stronger (at no cost to you), its view would improve and it would get larger each year. The quid pro quo would be that its price will be volatile.

Would you buy that asset, knowing that it would continually improve without any maintenance cost? Not only is it not subject to external conditions, all its conditions are known in advance.

A completely made up story

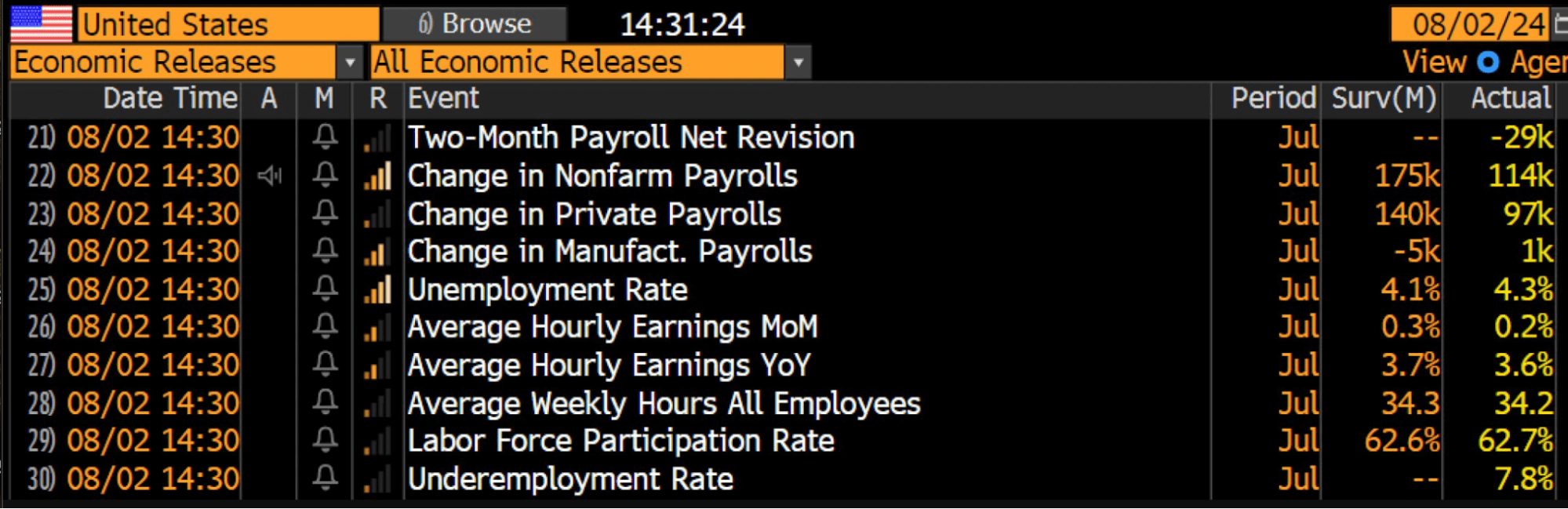

“Weakening US Jobs data”. As we pointed out last week with the ‘Quit Rate’, weakinging probably doesn’t quite cover it. In the US five of the last six jobs reports were revised lower subsequently. That is a very unlikely outcome unless the statistics are knowingly false or, more likely, the trend is simply in that direction. They missed on every score but participation rate last week.

It seems very clear now that the trend is downward for employment. Talk is no longer about whether we cut or not, it seems the discussion is around whether the cut is a full half percentage point rather than a quarter.

It’s a similar tale in Australia; the trend is now downward.

The alternative view is that there is persistent inflation and the RBA should raise rates. Chris Joye of Coolabah Capital being the main proponent of this particular narrative.

The main issue with all of this nonsense is that we all seem to actually believe that the interest rate is the only thing that sets the inflation rate. In fact surely it is the demand and supply of goods. If we simply got better at supplying things and dropping input prices, that would have more impact than anything.

A simple example here would be energy. Australia is awash with energy, the Saudi Arabia of gas. The Australia of uranium. Energy should basically be free here, we could pay for it for our 25 million people with export levies. This would have a massive impact on input prices for everything, inflation would collapse.

We never hear that though. We hear only about the blunt instrument of interest rates, where every policy error is corrected some years later by making borrowers pay more.

If you wanted an advert for an alternative monetary system the whole joke of interest rates and inflation would be it. It’s a complete circus of people pretending they can predict the future and therefore the opportunity cost of consumption foregone (the interest rate).

Lot’s of insiders make money from arbitraging rates and talking about what the next move is going to be and second guessing the Fed etc. Bank profits will go through the roof this year because their margins are effectively doubled on higher rates. Remember when the Reserve Bank told us there would be no rate rises from 0.5% until likely 2025! They were being honest and simply revealed that they have about as much clue as you and me. None.

Yet nearly everyone believes the story.

Seems unlikely

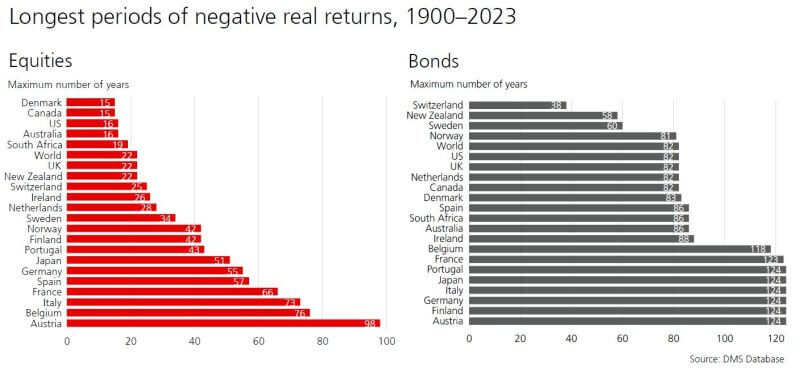

A reader sent this chart in. Always grateful for inbound content by the way, so don’t hesitate to send it in. In this case though, I do have some questions.

It lays out the longest runs (by country) of negative real returns. The suggestion is that the Austrian stock market went 98 years without making a positive real return. I suppose it’s possible, it just feels unlikely. Did France really do a 66 year negative stretch?

Anyway, let’s just assume it is directionally correct. We have six very large countries that have never delivered a positive return on their bonds. Again, it seems rather unlikely to me except that the negative stretches on the right are overwhelmingly, and consistently, longer than those on the left.

Bonds just seem a systemically awful investment over any period other than two to three years which appears to match where the overwhelming demand is on the bond curve.

If there was something new in this chart that we perhaps do not consider enough it’s this: where you live really, really matters. Countries can get it wrong and when they do the effects are lasting, so much so that an entire lifetime can pass before recovery. Something to ponder as dust gathers on your passport.

Meme of the week

Euro-Trash

It’s holiday month in Euro-land. Christine normally takes the first two weeks of August off (per her published calendar of appointments). So we have time to check in on where Europe stands economically.

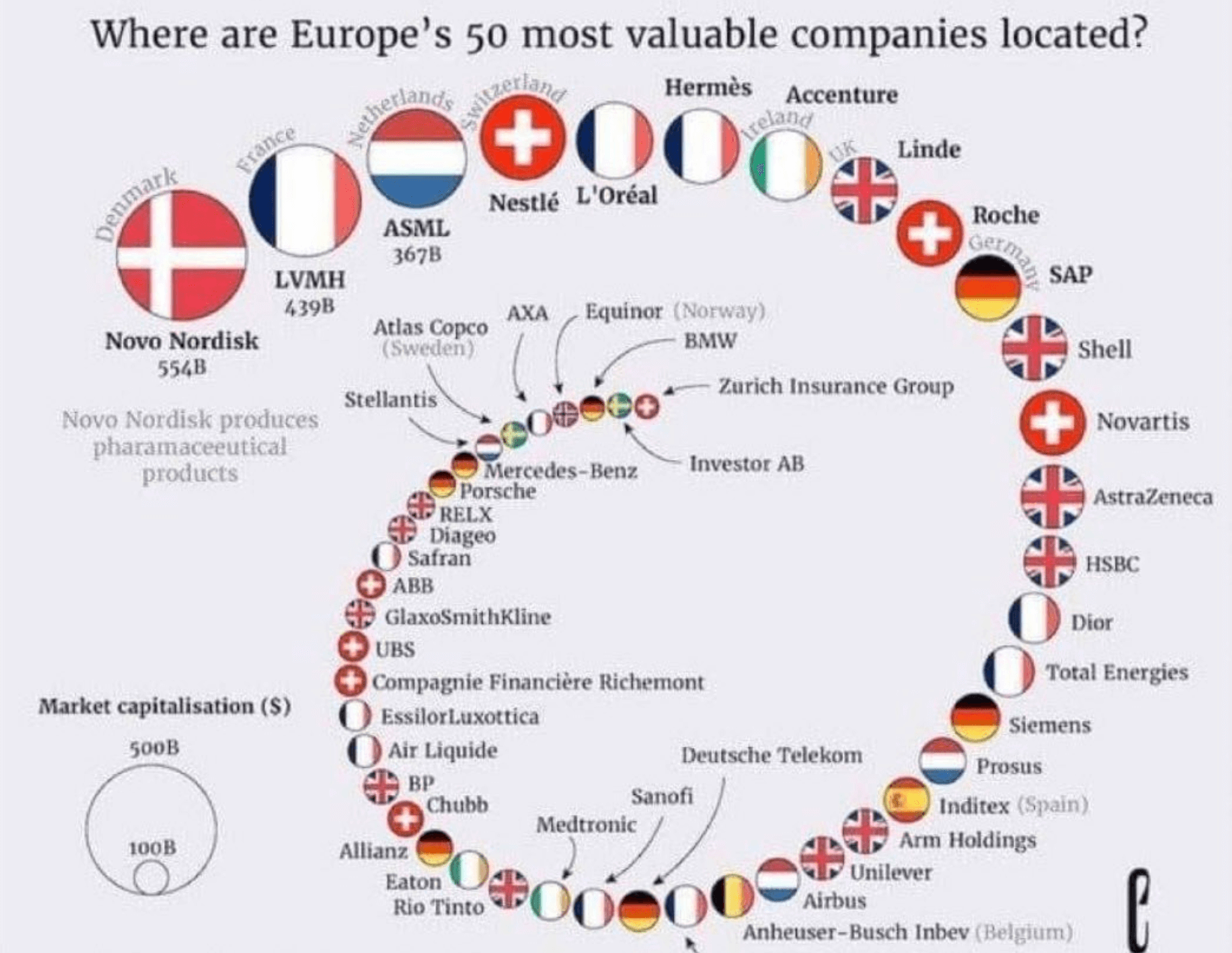

None of Europe’s top 50 companies are currently in the top 10 globally. There is only one (Novo) in the top 25. Their results this week were a disappointment too, well below forecasts. Perhaps more significant though is how old the European companies are. Many of them have been around for many decades, that is not bad per se, but simply points to the total lack of innovation across an entire continent.

Increasingly too it is obvious that other countries are aware of this. India for example makes its deals with Russia and China. The BRICS generally interact amongst themselves. Europe is an afterthought.

Sadly, not everyone was on leave though. Thierry Breton was busy celebrating his latest scalp via the Digital Services Act. It seems TikTok had launched a service in Europe that “could have had” addictive consequences. Thierry has now banned it. Personally not a fan of TikTok but do we really want Thierry thought policing us.