A bus

Hostage to fortune

The power of energy independence is being writ large across the sky by the Ukraine conflict. The US Secretary of State is looking to ban Russian oil imports for reasons we can well understand, but with oil at $100 translating to $4/gallon at the US pumps it is not politically compelling to do it. Talk of a Russian oil ban has now pushed the price to $130, that could mean over $5/gallon in America, a record. Not a pleasant calculus for the Biden administration to contend with.

There is perhaps no better illustration of how regressive energy prices are than when they force up the price of petrol. Most people cannot avoid that cost, simply driving to work becomes an enormous burden, it’s a burden sufficient to lose elections. In Australia, a Federal election is a few months away, prices are now rising so quickly they will almost certainly have an impact at the polling booth and it’s unlikely to be kind to the incumbents.

Unfortunately, politicians will reach for convenient enemies. I anticipate hearing a great deal more about bitcoin’s power consumption shortly as politicians look to deflect from their poor long term choices.

This might be an absolute boon for places like El Salvador though which has unlimited natural energy from its volcanoes. What’s more, they are not vulnerable to global energy prices. Their access to boundless energy as well as their willingness to go it alone might transform the country. Bitcoin is now a player on the global energy stage. It can help solve problems where there is surplus energy from renewable resources (which there almost always is at times) but it is likely to be more famous for putting new countries on the map that never were before.

The forever gap

A lot of people think that the Federal Reserve and the US Government are operating some sort of monetary conspiracy in which they, and those closest to them, are personally enriched at the expense of everyone.

It’s a neat theory but nothing could really be further from the truth. They are incredibly open with their data and with their objectives. For example, they have never deviated from telling people that they plan to devalue your net worth at 2% per annum, at a minimum, ad infinitum. No explanation is ever put forward for why that is appropriate. It is simply accepted to their great financial benefit and our loss.

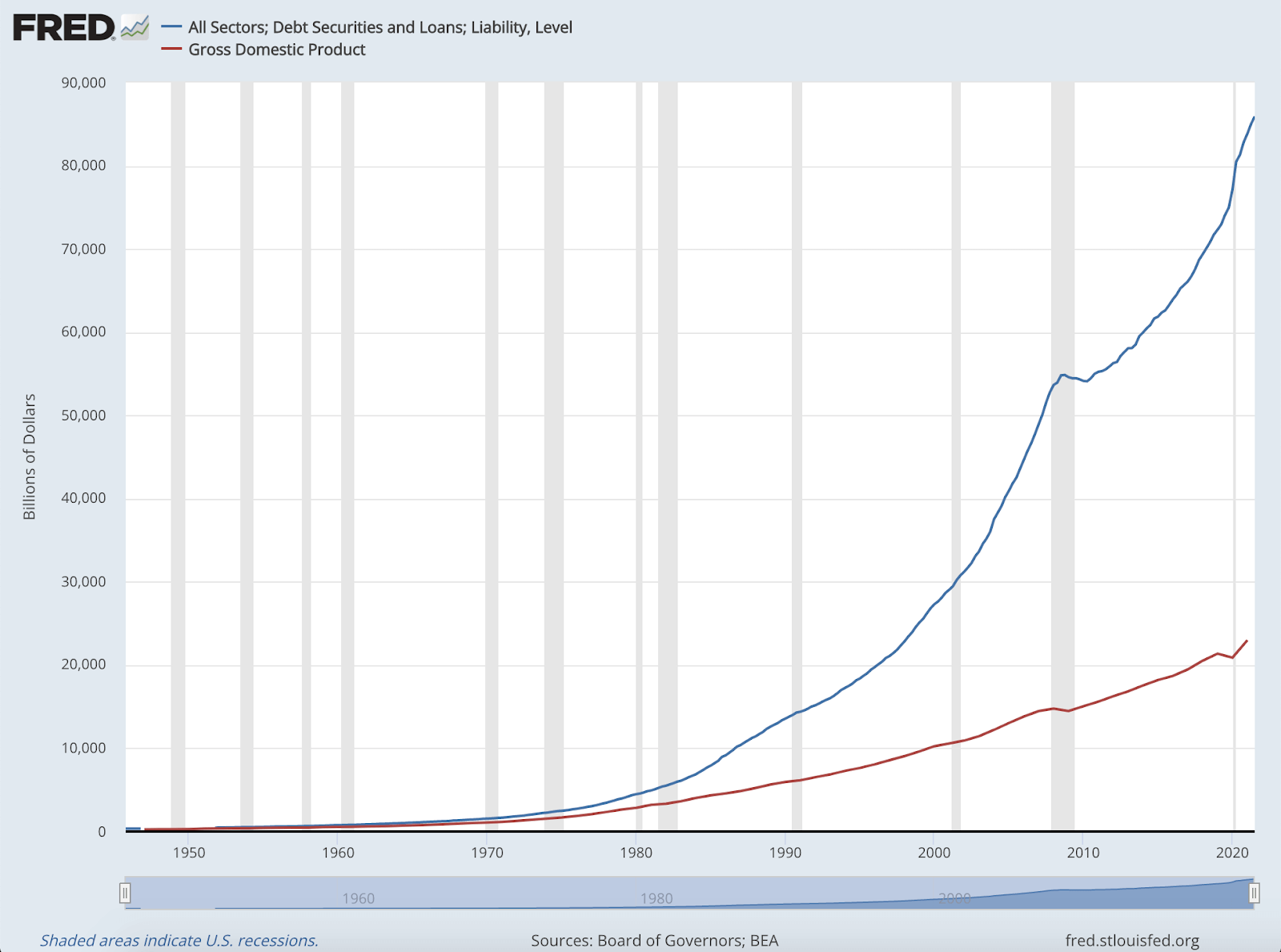

More telling are the detailed charts provided by the Federal Reserve on the path to national bankruptcy.

The blue line details American liabilities, both public and private. The red line GDP. National leverage is absolutely soaring off the back of free money. The American economy is now about 4x leveraged on these figures.

What does the chart tell us? America cannot sustain higher interest rates. Talk of eight hikes this year simply isn’t going to happen. It would accelerate bankruptcy.

Let’s make a prediction, that by the time of the US midterms in November there has been a total re-rating of exactly where interest rates might go. Most people think raise after raise after raise, in fact the system is now hyper sensitive to minor changes in rates. Two to three raises, then outright panic.

There is no conspiracy. It’s right there in black and white in any chart you care to look at. If there is any nuance at all it is that the situation is much worse than the charts suggest, because it does not include unfunded liabilities like medicare and public pensions which will be among the biggest burdens for the federal government quite soon.

This is by no means a pessimistic appraisal, it’s all part of the economic cycle of renewal that’s as old as time. There will be massive opportunities available for people that take them and we plan to.

Euro-Trash

The purpose of Euro-Trash is simply to point out the utter madness that pervades the European Central Bank. It would be great to focus on their monetary policy, but their marketing machine just keeps handing us gifts like these. It’s hard to let them pass.

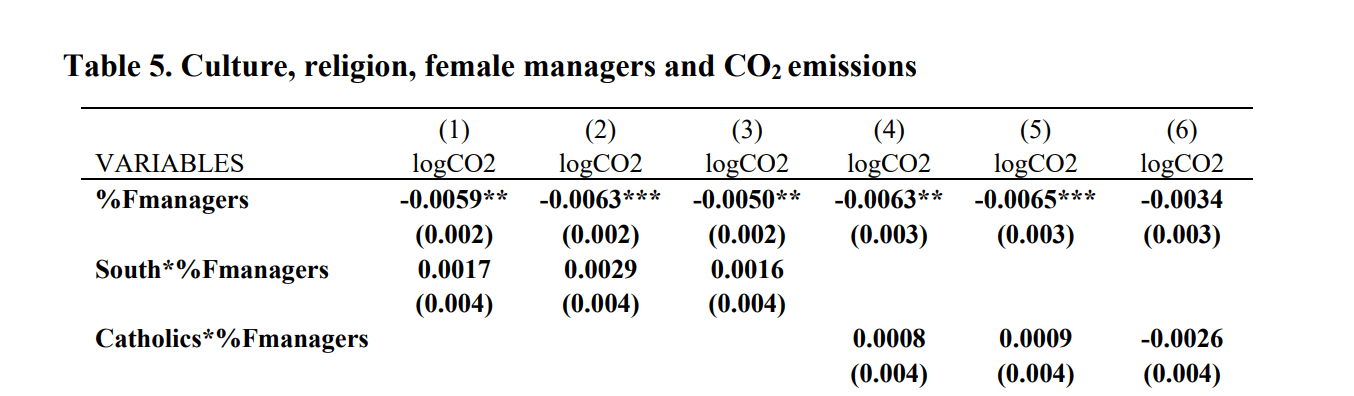

This research paper is dedicated to a supposed causality between gender diversity and climate change. The report is mind-blowingly bizarre. Among other oddities, it uses a control group for its measurements “are you catholic?”, referring to businesses with a certain percentage of “catholic to non-catholic female managers”. The inference is that being catholic does not change your opinion on the climate, so it’s a good control group. Seems more like a sweeping assumption that totally invalidates the ‘research’, but they went with it anyway.

Among many other delights was this formula. You couldn’t make this up. It’s on page 17 if you don’t believe me.

![]()

The report concludes that a 1% increase in female managers results in a 0.5% reduction in carbon emissions, hardly compelling. I imagine it would be just as easy and just as wrong to conclude that a 0.5% reduction in carbon emissions results in a 1% increase in female managers who are either catholic or not.

Most of all though, what on earth does gender diversity or climate change have to do with the ECB? They have a mandate to keep prices stable. It’s their sole function which they have been manifestly unable to deliver on for over a decade.

Where is the paper “Is there a correlation between ECB incompetence and inflation?”.

This week at ListedReserve

This morning we are presenting our fund at the Emergence Conference in Sydney. We are taking a rather direct approach to explaining our fund this year. For those that don’t know the pitch, it’s here.

Thesis

- Our core asset, bitcoin, uniquely solves for digital scarcity.

- Scarcity is seriously undervalued in a world of exploding money supplies and debt levels.

- Truly decentralised systems are extremely rare, but vastly superior.

- Decentralised ownership incentivises network effects, which will consume the value of centralised systems.

Performance

The necessary conditions for outperformance are

- Believing something strongly

- Being right

- Everyone else believing you are wrong consistently

Our fund sits in that category. We get told “too risky” and “too volatile” but the bulk of our fund is invested in the only asset in the world that is pure, valuable, instantly transferable, unencumbered collateral.

It is the ultimate asset. The other components of our fund benefit from similar features or indirectly as the picks and shovels that support the core assets.

It is only risky and volatile because the market does not understand it well (yet). Again, that is a necessary condition for outperformance.

Our fund has had an eventful six months, being down 35% from its peak. Even so, we have still outperformed nearly every other fund in Australia since we began in 2018.